Stocks’ Details

IOOF Holdings Limited

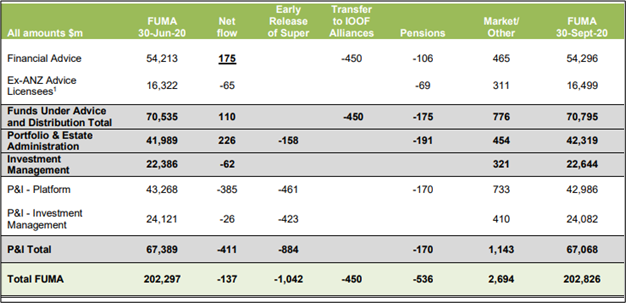

ACCC Approves Proposed Acquisition of MLC: IOOF Holdings Limited (ASX: IFL) provides financial advice and distribution, along with portfolio and estate administration, and investment management solutions. The market capitalisation of the company stood at ~$2.32 billion as on 31st December 2020. Recently, the company has received a final decision from the Australian Competition and Consumer Commission (ACCC) with respect to the proposed acquisition of MLC, which stated that ACCC would not oppose IOOF’s proposed acquisition of MLC. For the quarter ended 30th September 2020 (Q1 FY21), the company reported a total FUMA (Funds Under Management, Advice and Administration) of $202.8 billion, reflecting a rise of $529 million as compared to the previous quarter. The financial advice business reported net inflows of $175 million while investment management recorded a net outflow of $62 million. Also, the portfolio & estate administration business experienced continued net inflows of $226 million during the quarter.

Key Financials (Source: Company Reports)

Outlook: The company is expecting a run-rate synergy of $43 million in FY21 with respect to Pensions & Investments business. In addition, the company is building scale in its business for long-term benefits.

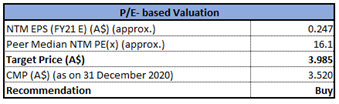

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

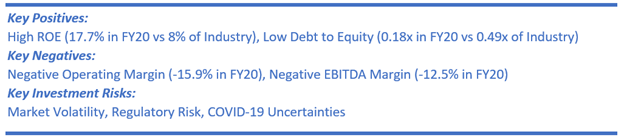

Stock Recommendation: The company ended FY20 with cash and cash equivalents of $374.7 million. The stock of IFL has corrected 9.27% and 22.06% in the last one and six months, respectively. As a result, the stock is trading towards its 52-weeks low level of $2.505. We have valued the stock using the price to earnings multiple based illustrative relative valuation and arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Challenger Ltd (ASX: CGF), Pendal Group Ltd (ASX: PDL), Perpetual Ltd (ASX: PPT), and others. On a technical analysis front, the stock has a support level of ~$2.824 and a resistance level of ~$5.188. Therefore, in light of the favorable final decision by ACCC regarding MLCAcquisition, growth in FUMA during Q1 FY21, current trading levels, and valuation, we give a “Buy” recommendation on the stock at the current market price of $3.520 per share, down by 1.676% on 31st December 2020.

Pinnacle Investment Management Group Limited

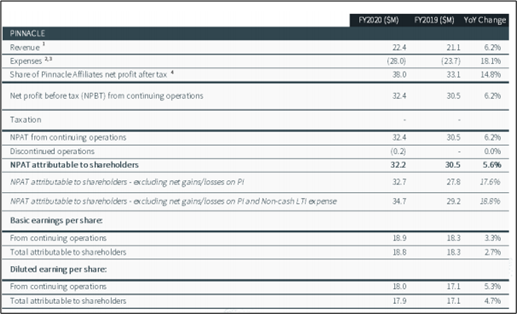

Decent Growth in FUM: Pinnacle Investment Management Group Limited (ASX: PNI) is engaged in the development and operation of investment management businesses. The market capitalisation of the company stood at $1.35 billion as on 31st December 2020. Despite the fall of 10.8% in the ASX300 index over the 12-month period ended 30th June 2020, the company witnessed a rise of 8.1% in funds under management (FUM) to $58.7 billion. For the year ended 30th June 2020, the company recorded a net profit after tax (NPAT) attributable to shareholders of $32.2 million, reflecting a rise of 5.6% over the prior year. The company declared a fully franked final dividend of 8.5 cps, which took the total dividend to 15.4 cps.

Key Metrics (Source: Company Reports)

Outlook: The company’s decision to keep its core capabilities well-resourced in FY20 is likely to place the business in a decent position for further growth. In addition, the company would also continue to invest in and seed new Affiliates where management teams have a strong track record and growth potential.

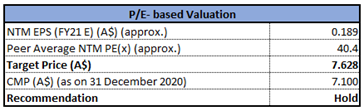

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company recorded net inflows of $3.0 billion in FY20. Basic earnings per share (EPS) for the year stood at 18.8 cents, up 2.7% over FY19. In the last one and three months, the stock of PNI has provided positive returns of 16.39% and 40.03%, respectively. We have valued the stock using the price to earnings multiple based illustrative relative valuation and arrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers like Challenger Ltd (ASX: CGF), HUB24 Ltd (ASX: HUB) and NIB Holdings Ltd (ASX: NHF). On a technical analysis front, the stock has a support level of ~$4.725 and a resistance level of ~$7.831. Hence, considering the decent returns in the past months, growth in FUM, outlook, and valuation, we give a “Hold” rating on the stock at the current market price of $7.100 per share, down by 1.934% on 31st December 2020.

humm Group Limited

Signing of MOU with Douugh: humm Group Limited (ASX: HUM) provides the point of sale lease and rental finance for the IT equipment, electrical appliance and other retail markets. The market capitalisation of the company stood at ~$567.08 million as on 31st December 2020. Recently, the company reached a Memorandum of Understanding with neobank Douugh in order to roll-out a Douugh-branded buy now pay anywhere feature into the U.S market in 1H FY22 via a proposed joint venture. The company is also making a strategic investment of $2.5 million in Douugh for supporting support research and development, marketing and growth. For FY20, the company reported Statutory Net Profit After Tax amounting to $21.4 million and cash NPAT of $29.2 million, which indicates COVID-19 macro-overlay provision. In addition, the company witnessed a YoY growth of 30% in active customers to 2.3 million.

Financial Summary (Source: Company Reports)

Outlook: The strategic priority of the company revolves around delivery on its key strategic pillars with the significant rationalisation of products while achieving double-digit volume growth and strong customer engagement.

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: At the end of FY20, the company had wholesale funding facility headroom of $648 million and $145 million of undrawn corporate debt facilities and unrestricted cash representing net gearing of 29%. We have valued the stock using the price to cash flow multiple based illustrative relative valuation and arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Smartgroup Corporation Ltd (ASX: SIQ), Credit Corp Group Ltd (ASX: CCP), IOOF Holdings Ltd (ASX: IFL), to name few. On a technical analysis front, the stock a support level of ~$0.907 and a resistance level of ~$1.366. Thus, considering the recent signing of MOU, growth in active customers, outlook and key risks associated with the business, we give a Speculative Buy” recommendation on the stock at the current market price of $1.125 per share, down by 1.747% on 31st December 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...