.png)

Stocks’ Details

Kogan.com Limited

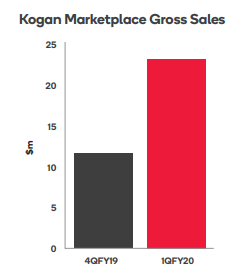

Q1 FY20 Business Update:Kogan.com Limited (ASX: KGN) isa portfolio mix of retail and services businesses, which include Kogan Retail, Kogan Marketplace, Kogan Mobile, Kogan Internet, Kogan Insurance, Kogan Health, Kogan Pet, Kogan Life, Kogan Money, Kogan Cars and Kogan Travel. The market capitalisation of the company stood at ~A$661.47 Mn as on 5th November 2019. Recently, the company updated the market with its performance for the first quarter ended 30th September 2019. It stated that the period has witnessed the rollout of key New Verticals such as Kogan Money Super, Kogan Mobile NZ, Kogan Energy and Kogan Money Credit Cards. KGN added that each of these verticals is supported by a strong commercial partnership with a top tier incumbent provider that focuses on providing customers with a market-leading offer. Moreover, September 2019 quarter also witnessed a robust growth in Exclusive Brands and continued momentum in Kogan Marketplace.

Kogan Marketplace Gross Sales (Source: Company Reports)

What to Expect:As per the Annual Report for FY20, the company expects a continued brand growth and deeper market penetration of maturing portfolio businesses alongside continuing expansion of new portfolio businesses. The company also anticipates growth in active customer base, exclusive brands, Kogan Marketplace, Kogan Insurance and Kogan Internet in FY20.

Stock Recommendation: KGN entered into an agreement with Corporate Travel Management Limited, which would help the company to offer Kogan Travel branded travel services, including flights, cars and holiday packages, during FY20. Return on equity of the company stood at 34.8% in FY19, reflecting a YoY growth of 3.6%. This implies that the company has provided decent returns to its shareholders. The company has witnessed a CAGR growth of 21.65% in total revenue within a time span of 5 years (FY15 - FY19). On the stock’s performance front, it generated returns of 11.75% and 45.45% in the time period of one month and three months, respectively. Hence, considering the decent performance in Q1 FY20, agreement with Corporate Travel Management Limited, decent outlook, returns to shareholders and decent capabilities to generate revenue, we maintain our “Hold” rating on the stock at the current market price of A$7.080 per share, up 0.568% on 5th November 2019.

Accent Group Limited

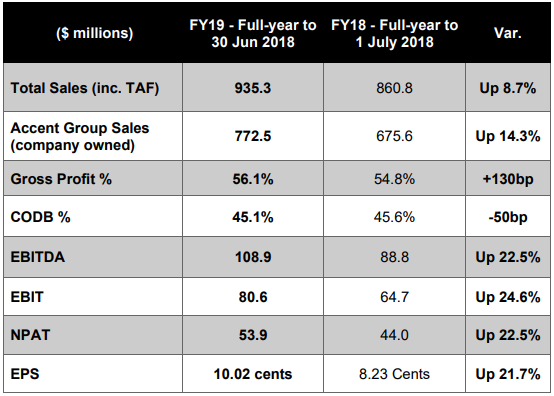

Annual General Meeting is to be held on 28 November 2019:Accent Group Limited (ASX: AX1) owns and operates numerous footwear and apparel businesses in the performance and active lifestyle sectors. The company recently announced that it would be conducting its 2019 Annual General Meeting on 28th November 2019. When it comes to financial performance, the company reported a statutory net profit after tax amounting to $53.9 Mn, reflecting an increase of 22.5% on the prior year. The key personnel of the company stated that FY19 has proved to be another record year of profit for the group. It continues to deliver against its growth plan objectives in gross margin improvement, new store rollouts, The Athlete’s Foot franchise acquisitions and innovation both in the digital and instore customer experience.

Financial Overview: (Source: Company Reports)

Future Guidance:For FY20, the company is aiming at bottom-line growth, which is anticipated to be achieved via low single-digit LFL growth, continued strong digital growth, 40 new stores, 54 stores annualising from FY19 and 65 current and new TAF corporate stores. The company anticipates the profit impact of The Trybe and PIVOT to be broadly neutral in FY20.

Stock Recommendation:The Board of Directors declared a fully franked final ordinary dividend of 3.75 cps. Consistent with approach communicated in 1HFY19, final dividend is more closely aligned to EPS and cashflow generated in H2. The ordinary dividends declared during the year stood at 8.25 cps, reflecting a rise of 22.2% on last year and representing an 82% payout ratio for the year. On the valuation front, the stock has EV to sales multiple of 1.1x in comparison to the industry median of 1.3x on TTM basis. The stock has EV to EBITDA multiple of 7.8x against the industry median of 8.4x on TTM basis. The net margin of the company stood at 6.8% in FY19 as compared to the industry median of 3.4%. This represents that the company has better capabilities to convert its top-line into the bottom-line against the broader industry. Thus, in light of the decent numbers in FY19, expectations for strong digital growth, capability of converting top-line into the bottom-line, and current trading levels we recommend a “Hold” rating on the stock at the current market price of A$1.565 per share, up 1.954% on 5th November 2019.

Super Retail Group Limited

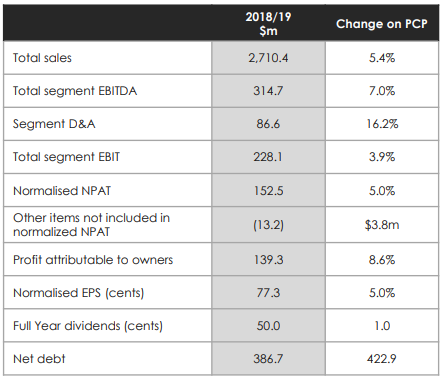

Decent Growth in Sales:Super Retail Group Limited (ASX: SUL) is in the operation of specialty retail stores in the automotive, tools, leisure and sports categories. It has a market capitalisation of ~A$1.88 Bn as on 5th November 2019. The company has recently appointed Rebecca Farrell as Group General Counsel and Company Secretary, effective from 3rd February 2020. Ms Farrellwould be a member of the Executive Leadership Team and would lead the SUL’s legal, company secretarial and compliance functions, including responsibility for sustainability, risk and health and safety. The company in a release stated that in the first 16 weeks of 2019/2020, the Group has delivered total sales growth of 4.2% and like for like (LFL) sales growth of 3.2%. The following picture provides an idea of results for FY19:

Group Results (Source: Company Reports)

Future Prospects:The Group would be looking towards building on the strategic pillars, and primarily would be focused on (1) Delivering a seamless omni retail experience for its customers, (2) Integrating its supply chain to deliver lower costs, reduced working capital and increased utilization, and (3) Leveraging its powerful retail brands to create new profit pools and improve gross margin.

Stock Recommendation:The stock of SUL is trading at a price to earnings multiple of 13.46x in comparison to the industry average of 16.7x on TTM basis. It has an EV to EBITDA multiple of 7.1x as compared to the industry average of 15.2x on TTM basis. The gross margin and EBITDA margin of the company stood at 45.1% and 11.5% in FY19 as compared to the industry median of 24.2% and 6.9%, respectively. On the stock’s performance front, it produced returns of 25.66% in the time span of six months. However, on a YTD basis, the stock delivered a return of 39.09%. Thus, considering the sales growth in the first 16 weeks of FY20, decent outlook, and respectable returns in the past few months, we reiterate our “Hold” recommendation on the stock at the current market price of A$9.460 per share, down 0.421% on 5th November 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...