Ramsay Health Care Limited

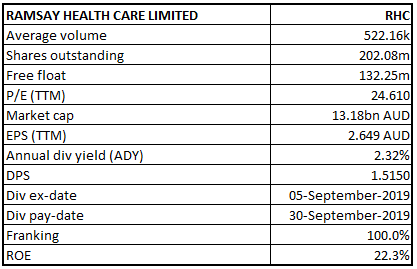

RHC Details

Brown Field Expansion Led to Improved Fundamentals: Ramsay Health Care Limited (ASX: RHC) is a major global healthcare service provider company which operates across 11 countries, treating more than 8.5 million patients in circa 500 locations. Recently, Ramsay Health Care Limited informed that Paul Ramsay Holdings Pty Limited has completed the underwritten block trade sale of 22 million shares (representing 10.9% stake) of RHC to institutional investors at $61.80 per share. Following the settlement, Paul Ramsay Holdings Pty will hold ~21% of the issued share capital.

Why Are We Watching RHC?

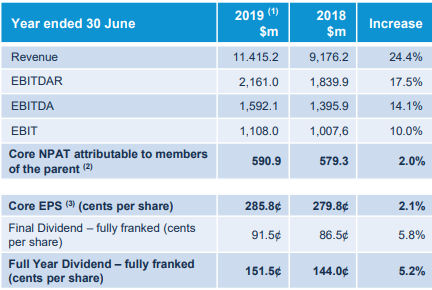

Reason 1- Decent Financials in FY19: RHC announced FY19 annual results wherein, the company posted a revenue of $11.415.2 million, up 24.4%. The company posted a Core Net Profit After Tax of $590.9 million during FY19, a yoy increase of 2%. The company reported EBITDA of $1,592.1 billion, up 14.1% from FY18. UK segment delivered a decent EBIT & revenue growth in the second half, aided by recovery in NHS volumes and tariff increase during April 2019. During the period, the Ramsay acquired 16 brownfield projects, costing $242 million across Australia which included a total of 333 new beds and a net of 216 beds along with 15 operating theatres and 30 consulting suites. The company during FY19 completed the acquisition of the pan-European healthcare company, Capio. Revenue from Australia came in at $5.18 billion, up 4.1% on y-o-y, followed by 6% higher EBITDA of $950.5 million on y-o-y basis. Continental Europe reported revenue and EBITDAR growth of 51.7% and 32.6%, on y-o-y basis at €3.4 billion and €590.9 million, respectively. Revenue form United Kingdom stood at £444.3 million, grew by 4.7% on FY18 while EBITDAR was down by 2.8% to £99.8 million during same period.

FY19 Financial Highlights (Source: Company Reports)

Reason 2- The Board of Directors announced a fully franked dividend of AUD 0.91500000 for each ordinary share held, payable on 30 September 2019.

Reason 3-Decent Outlook: As per FY20 guidance, RHC is targeting Core EPS growth on a y-o-y basis in the range of 2% to 4%. This corresponds to negative Core EPS growth of -6% to -4% under the new lease accounting standard AASB16. The management expects Core EBITDAR to grow in the range of 8% to 10%, aided by positive changes to operating model. The company is predicting robust growth in terms of volumes in FY20 on account of brownfield acquisition in Australia and major turnaround in NHS volumes in the UK. The Board also highlighted FY20 EBITDAR to be unaffected by the new lease norms.

Stock Recommendation: The stock of RHC is trading at $62.200 with a market capitalization of $13.18 billion. The stock is quoting close to the average price of its 52-week high and low of $74.120 - $51.890. The stock has delivered returns of -8.35% and 4.03% in last three-months and six-months, respectively. Stock has corrected 7.86% in last 1 month. The stock is available at an Enterprise Value to Sales of 1.6x on Trailing Twelve Months (TTM) basis as compared to the industry median of 1.9x. Australian brownfield programme remained robust with a total of 16 projects completed during FY19 which will strengthen Ramsay’s position as a leading international healthcare service provider. Higher scale and size provide a platform to drive greater efficiencies and establish stronger global partnerships for the company. Considering the aforesaid facts, price movement and business prospects, we recommend a ‘Hold’ rating on the stock at the current market price of $62.200, down 4.601% as on 17 September 2019.

Daily Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...