Stocks’ Details

QBE Insurance Group Limited

1H19 Statutory NPAT up by 29%: QBE Insurance Group Limited (ASX: QBE) is an Australia-based company with over 12,000 people employed in more than 31 nations. QBE is an insurance and reinsurance company, which offers commercial, personal and speciality products and risk management solutions to its consumers.

On 18 December 2019, the company stated that bad weather conditions in North America have adversely impacted the 2019 crop results. The company anticipates North American Crop insurance business’s current accident year operating ratio to be ~107% – 109% on net earned premium of roughly $1.2 billion. The results were impacted by prevented planting claims along with the yield shortages.

Other Recent Updates: On 16 December 2019, the company announced the cancellation of 1,499,698 QBE shares as part of the on-market share buy-back. On 11 December 2019, the company announced that Frederick Eppinger has ceased to be a Director in the company, effective from 6 December 2019.

Key Highlights for 1H19 Results: During the period, the company reported a statutory net profit after tax of $463 million, an increase of 29% from the prior year. Cash profit after tax stood at $520 million, an increase of 35% from the year-ago period. The company’s debt to equity ratio reduced from 38% in FY18 to 36.8% in the current period.

Operating Results (Source: company Reports)

Guidance: For FY19, the company expects its operating ratio to be between 94.5% – 96.5%. Net investment return is anticipated to be in the range of 3.0% – 3.5%.

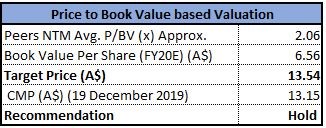

Valuation Methodology:Price to Book Value Multiple Approach

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per the ASX, the stock gained 10.06% in the past six months. Currently, the stock is trading close to the 52-week high of $13.42. Considering the operational performance in 1HY19 in terms of improvement in attritional claims experience along with material investment returns and decent guidance for FY19, we have valued the stock using Price to Book Value based relative valuation method and arrived at a target price with lower single-digit upside (in % terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $13.15, down 0.152% on 19 December 2019.

Nearmap Ltd

Nearmap Acquires Intellectual Property and Technology from Primitive LLC: Nearmap Ltd (ASX: NEA) offers technology for integrated geospatial map for enterprises, businesses and governments.On 12 December 2019, the company acquired intellectual property and technology from Primitive LLC. This move is a part of the company’s strategy to obtain and generate roof geometry from its capabilities and enhance the customer experience. The price consideration of the acquisition stood at US$3.5 million, which was funded via $70 million equity raised in September 2018.

Director’s Interest Update: On 16 December 2019, the company announced that Robert Melville Newman, one of the Directors in the company, has acquired 666,667 fully paid ordinary shares for a consideration of $1.06 per share.

Issue of Shares to Directors and KMP: On 16th December 2019, the company announced the issue of 1,500,001 fully paid ordinary shares to a Director and KMP of the company on conversion of options. On 13th December 2019, the company also issued 6,250 fully paid ordinary to an overseas employee of the company.

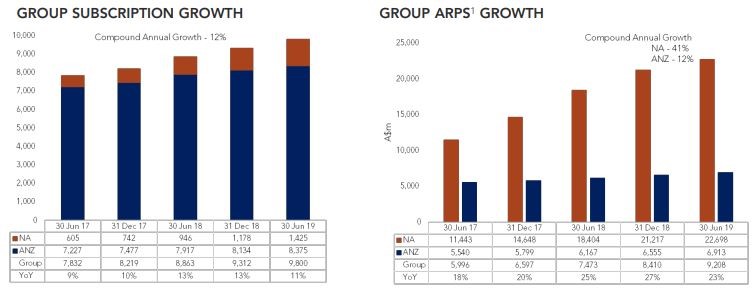

FY2019 Highlights for the Period Ended on 30 June 2019: The company reported revenue of $77.64 million, up 45% year over year. Subscriptions increased by 11% during the period and stood at 9,800. The company noted an increase of 23% in group average revenue per subscription (ARPS).Group annualised contract value came in at $90.2 million, up 36% year over year.Group customer churn came in at 5.3% as compared to 7.5% reported in the year-ago period.

Subscription Highlights (Source: Company Reports)

Subscription Highlights (Source: Company Reports)

Stock Recommendation: As per the ASX, the stock has gained 78.4% on a year-to-date basis. Currently, the stock is trading below the average of its 52-week low and high of $1.480 and $4.290, respectively. The company expects strong momentum in FY20 with continued growth in ACV portfolio, accelerating expansion in North America, improving leadership in Australia and New Zealand, along with artificial intelligence features on MapBrowser. Considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $2.730 on 19 December 2019.

Propel Funeral Partners Limited

Expansion of Debt Facilities: Propel Funeral Partners Limited (ASX: PFP)provides services pertaining to funeral, homes cemeteries, crematoria and related assetsin Western Australia, New Zealand, Queensland and Victoria, Tasmania region. On 5 December 2019, the company announced that it increased its senior debt facilities with Westpac Banking Corporation to $150 million. The debt facility earlier amounted to $100 million. This expansion confirms that the company is well funded to continue with its acquisition strategy.

Financial Highlights for FY19 Period Ended 30 June 2019: The company reported revenue of $95.1 million, an increase of 17.6% year over year. Operating EBITDA came in at $23.8 million, up 10.6% year over year. Operating NPAT increased by 8.1% and came in at $13.3 million. Gross profit margin improved from 69.7% to 70.7% in FY19.

Financial Highlights (Source: Company Reports)

Outlook: The company expects momentum in FY20 from the increasing number of funeral ceremonies. Also, the company has strengthened its business from the recent acquisition of Waikanae Funeral Home, the Kaitawa Crematorium and the Morleys Group.

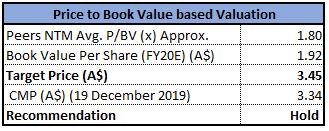

Valuation Methodology:Price to Book Value Multiple Approach

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per the ASX, the stock has gained 32.93% on a year-to-date basis.The stock made its new 52-week high of $3.350 on 19 December 2019. Propel Funeral Partners Limitedsees advantages from the increasing number of funeral volumes. The company also expects to increase financial flexibility in order to enhance shareholders’ value through dividends and growth initiatives. Considering the above factors, we have valued the stock using Price to Book Value based relative valuation method and arrived at a target price with lower single-digit upside (in % terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $3.340, up 0.3% on 19 December 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...