Westpac Banking Corporation

.png)

WBC Details

WBC Announced Its H1FY19 Report: Westpac Banking Corporation (ASX: WBC) operates in Consumer Bank, Business Bank, BT Financial Group (Australia), Westpac Institutional Bank, and Westpac New Zealand.

The bank recently announced interim financial results where it reported net profit decreased by 24% pcp to $3,173 million in first half 2019. Its liquidity ratios are well above the regulatory requirements of 100% as its Liquidity coverage ratio was reported at 138% and Net stable funding ratio was reported at 113%. Its net interest margin (excluding Treasury & Markets) were down by 12 bps from prior corresponding period due to provisions for customer refunds and higher short-term funding costs.

Its operating expenses increased by 1% in the half, as major remediation and restructuring items increased by $162 million. Its asset quality was reported sound as stressed exposures to total committed exposures (TCE) increased modestly by 1 bp compared to March 2018. The Board of Directors declared fully franked interim dividend of AUD0.94 with record date on May 17, 2019, and payment date on June 24, 2019.

.png)

H1FY19 Financial Metrics (Source: Company Reports)

What To Expect:As per the management, it is expected that the Australian economy will remain subdued with GDP growth this year expected to hold at around 2.2%. However, the economy will continue to be supported by strong government investment and exports, in both resources and services. Employment growth is likely to slow while inflation is likely to remain low.

The uncertain international backdrop is weighing on business investment decisions as markets are cautious of the recent trade war concerns along with softness in the European economy. House prices are likely to remain soft and home building is set to reduce through 2019 and into 2020. The bank expects that the system housing credit growth to slow to 3% in the current bank year and fall further next year to 2.5%, which would imply total credit growth slowing to 3% this year and 2.8% next year.

Despite challenges from regulatory compliance and Royal Commission recommendations, the company remains positive on the outlook and committed towards investments in technology, digital platforms to create value for its customers and shareholders.

Stock Recommendation:Its Tier 1 Risk-Adjusted capital ratio in H1FY19 stands at 12.84% better than 12.81% in H1FY18. On the valuation front, its EV/EBITDA for TTM stands at 5.3x lower than the industry median of 11.5x, indicating an undervalued position at the current juncture.

Hence, considering the aforesaid facts and current trading level, we recommend a “Buy” rating on the stock at the current market price of $27.060 (down 0.184% on May 7, 2019).

Commonwealth Bank of Australia

.png)

CBA Details

Potential for further upside: Commonwealth Bank of Australia (ASX: CBA) is the leading banking and financial service provider in Australia. Recently, the group disclosed that Commonwealth Bank of Australia and its related bodies became a substantial holder of Charter Hall Limited since May 03, 2019 with voting power of 5.01%. Moreover, it ceased to be a substantial holder in the Domino's Pizza Enterprises Limited effective from May 3, 2019.

In another update, CBA announced that significant fee reductionsby Colonial First State (owned by CBA) across its superannuation and investment platforms, reducing the cost of investing for over 500,000 members.It will lower costs for members across its FirstChoice Wholesale platform, FirstChoice Employer Super and its FirstWrap Plus platform and will come into effect from early June 2019 in line with updates to the relevant product disclosure statements. The changes announced are projected to result in a total benefit to members of around $68 Mn per year. The FY20 impact on net profit after tax is expected to be around $45 Mn.

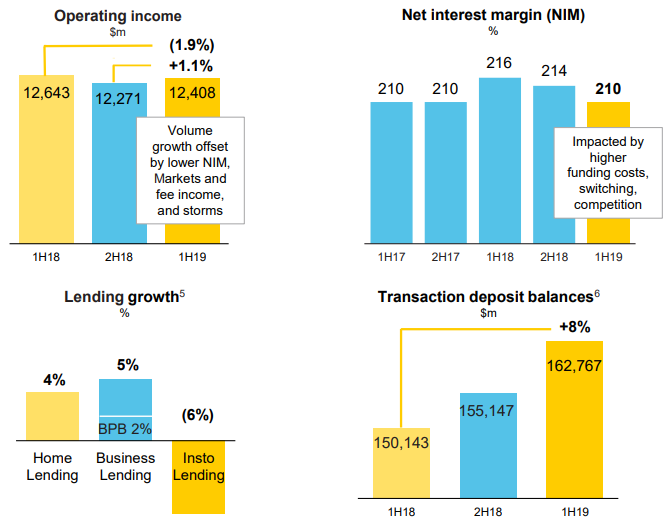

In H1FY19 results, CBA reported its statutory net profit after tax (NPAT) including discontinued operations at $4,599 Mn. Its cash NPAT from continuing operations increased by 1.7% to $4,676 Mn. Its operating income decreased by 1.9% to $12,408 Mn, with volume growth offset by lower net interest margin, lower Markets and fee income, and the impact of weather events. Its net interest margin was reported at 2.10% which is 4 bps lower than H2FY18, due to higher funding costs and home loan switching and competition. Its operating expenses reduced by 3.1% to $5,289 Mn, with elevated risk, compliance and remediation costs offset by prior period one-offs.

H1FY19 Financial Metrics (Source: Company Reports)

What To Expect: Growing population, infrastructure boom, and continued demand for Australia’s exports supported by growing incomes in Asia are expected to support earnings of the banks.Despite regulatory compliances and Royal Commission recommendations, CBA believes that their strong franchise, dedicated people, and their strong commitment in making necessary changes will deliver good results in the forthcoming year.

Stock Recommendation: Its Tier 1 Risk-Adjusted Capital Ratio in H1FY19 stands at 12.90% better than 12.30% in H1FY18. On the Valuation front, its EV/EBITDA for TTM (trailing 12 months) stands at ~7x, which is lower than the industry median of ~11.5x, indicating potential for further movement. Hence, considering the aforesaid facts and current trading level, we recommend a “Hold” rating on the stock at the current market price of $74.610 per share (down 0.44% on May 7, 2019).

Macquarie Group Limited

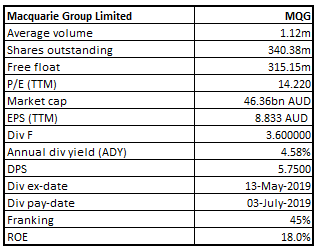

MQG Details

Overvalued Position at Current Juncture:Macquarie Group Limited (ASX: MQG) recently announced that it been granted relief from section 259C of the Corporations Act 2001 (Cth) relating to certain acquisitions of Macquarie shares by Macquarie Group companies. In another announcement, MQG reduced its interest in Atlas Arteria Limited from voting strength of 6.34% to 5.34%.

Financials:In its FY19 Net profit, the contribution from annuity-style businesses was 53% and markets-facing businesses were 47%.

Under annuity-style businesses:

-

Macquarie Asset Management (MAM) contributed 24%

-

-

Corporate and Asset Finance (CAF) contributed 17%

-

-

Banking and Financial Services (BFS) contributed 12%

-

Under markets-facing businesses:

-

Commodities and Global Markets (CGM) contributed 25%

-

-

Macquarie Capital (MacCap) contributed 22%

-

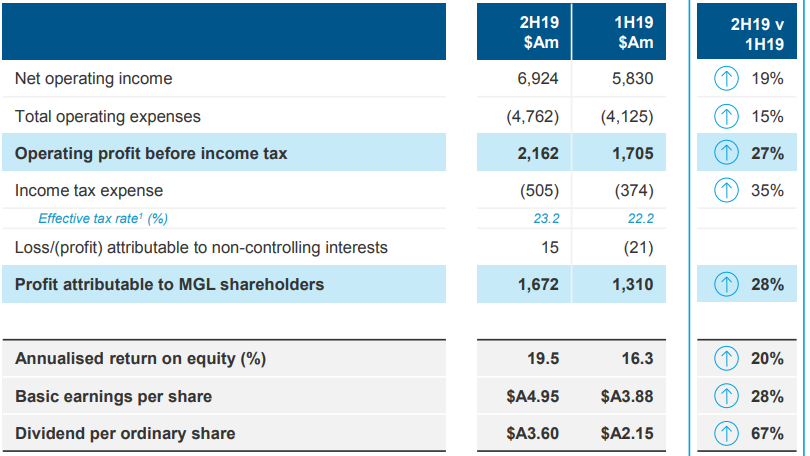

H2FY19 Financial Result (Source: Company Reports)

What To Expect: In the short term, the financial result for FY20 is expected to be slightly down than in FY19. The group’s short-term outlook is subject to the completion rate of transactions, market conditions, the impact of foreign exchange, potential regulatory changes and tax uncertainties, and geographic composition of income.

In the medium term, the company believes to deliver superior performance.Its ongoing program is expected to identify cost-saving initiatives and efficiencies.

Stock Recommendation: On the valuation front, the P/E of 14.22x and P/BV of 2.8x is currently above the industry median multiples of 11.3x and 1.2x respectively, indicating the stock to be overvalued. Also, the group’s stock price is trading slightly towards the 52-week higher level. Hence, considering the aforesaid facts and current trading level, we recommend a “Sell” rating on the stock at the current market price of $124.890 per share (down 0.581% on May 7, 2019), and we advice to investors that they can book the profit at the current level.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...