.png)

Stocks’ Details

Primero Group Limited

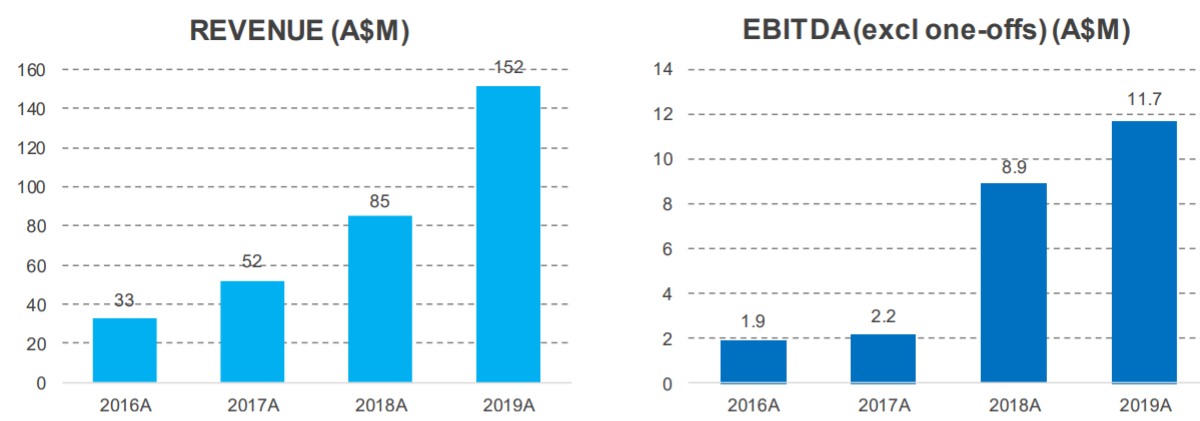

Substantial Growth in Revenue: Primero Group Limited (ASX: PGX) is an engineering contracting company, specialised in the provision of engineering design and construction services to the minerals, energy and infrastructure sectors. As on 23rd December 2019, the market capitalisation of the company stood at $58.52 million. During FY 2019, revenue of the company stood at $151.7 million, representing a growth of 78% on FY18. The company also reported a strong balance sheet with a cash balance of $21.9 million and a debt of $3.0 million.

The company executed several complex and highly technical EPC projects and recorded a 3-year CAGR of ~80% in underlying EBITDA.This reflects sustainable growth with strong operational contract performance.

Financial Performance (Source: Company Reports)

Growth Opportunities: The growth outlook of the company remains robust with significant recent contract wins in NPI and Minerals. PGX expects approximately $800 million of qualified tender opportunities and is well-positioned to capture a meaningful share in opportunities. The company is focusing on multi-year O&M / BOO project opportunities. It also expects building potential for larger revenue as well as longer duration contracts presenting throughout multiple commodities and business areas.

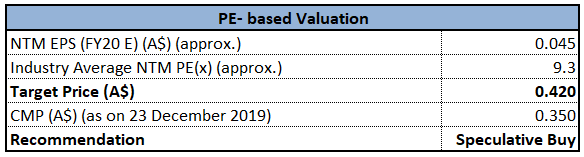

Valuation Methodology:P/E Multiple Based Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week low of $0.335, proffering a decent opportunity for accumulation. In the time span of 4 years from FY15 to FY19, the company witnessed a CAGR of 43.6% in revenue and a CAGR of 34.06% in gross profit. During the year, net margin and return on equity stood at 4.1% and 28.7%, higher than the industry median of 2.7% and 9.9%, respectively. This indicates that the company is well deploying the capital of its shareholders and is capable of converting its revenue into profits. Considering the trading levels, Revenue and gross profit CAGR, decent financial performance and growth opportunities, we valued the stock using a relative valuation method, i.e., P/E multiple approach and arrived at a target price of lower double-digit upside (in percentage terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.350, up by 2.941% on December 23, 2019.

LiveTiles Limited

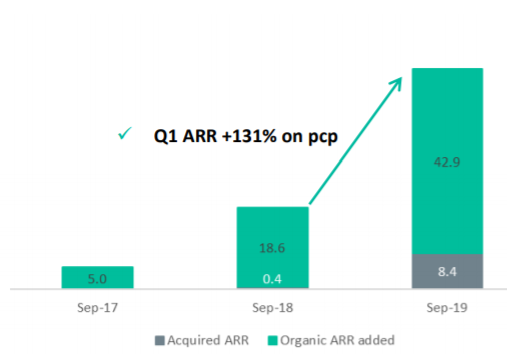

Strong Growth in Customer Cash Receipts: LiveTiles Limited (ASX: LVT) is engaged in the development and sale of business software in Australia and overseas. As on 23rd December 2019, the market capitalisation of the company stood at $215.1 million. The company has recently completed the acquisition of CYCL and has issued 42,605,922 shares as part of the upfront consideration. LVT has witnessed decent growth in customer cash receipts, resulting in another record quarter (i.e., Q1 FY 2020). In the first quarter, it also saw a growth of 131% in ARR (Annual Recurring Revenue) on prior corresponding period.

ARR growth (Source: Company Reports)

What to Expect From LVT: LiveTiles Limited expects to deliver another year of strong customer and revenue growth in FY20 with a target of achieving at least $100 million of ARR by June 30, 2021. The company has a clear path to drive operational execution in support of its growth strategy and is prioritising to increase the capacity and capability of internal and partner services to support customer onboarding and adoption. LVT also has clear plans to realise efficiency benefits and more effective customer, people and partner outcomes with completion expected by June 30, 2020.

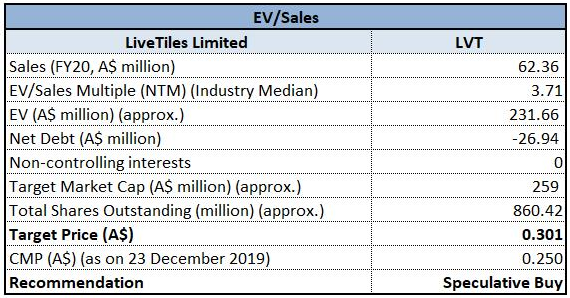

Valuation Methodology: EV/Sales Multiple Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week low of $0.240. In the time span of 4 years from FY15 to FY19, the company has witnessed a CAGR of 197.80% in revenue and has seen a significant improvement in EBITDA and net margin in the same time period. On account of current trading levels, CAGR in revenue, improving margins and decent outlook, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple, and arrived at a target price of lower double-digit upside (in percentage terms). Hence, we give a “Speculative Buy” rating on the stock at the current market price of $0.250 on December 23, 2019.

Aeon Metals Limited

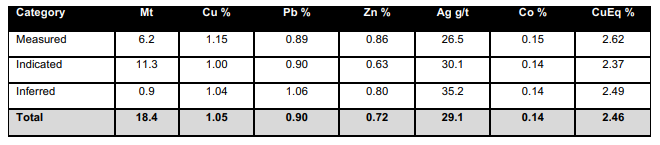

Grant of $1.65 Million: Aeon Metals Limited (ASX: AML) is primarily engaged in the exploration and development of the advanced Walford Creek Copper-Cobalt project. As on 23rd December 2019, the market capitalisation of the company stood at $105.02 million. Aeon advised that it is has taken receipt of R&D grant funds amounting to A$1.65 million for the research work. The grant is associated with the selection, design and operation of the metallurgical processes, which seek to produce high grade concentrates consistently and at the maximum recovery.Recently, the company stated that The Vardy & Marley Copper Mineral Resource has increased to 18.4mt @ 1.05% Cu, 0.14% Co, 29g/t Ag, 0.90% Pb and 0.72% Zn while the Vardy & Marley Cobalt Peripheral Mineral Resource has decreased to 17.4mt @ 0.26% Cu, 0.09% Co, 20g/t Ag, 0.80% Pb and 1.01% Zn.

Vardy/Marley Copper Mineral Resource (0.5% Cu cut-off) (Source: Company Reports)

Future Opportunities: The company has received various indicative, non-binding and confidential non-dilutionary funding proposals from several strategic and project financing counterparties. The company plans to progress these proposals, including with a view to delivering enough interim funds through to target completion of the Walford Creek PFS in 2Q 2020. The company is also prioritising Walford Creek towards the development of a world-class base metals mine as well as continue to explore on priority exploration tenements.

Stock Recommendation: As per ASX, the stock gave a return of 40.91% in the past one month. During the year, current ratio stood at 3.08x, higher than the industry median of 1.81x. Debt/Equity ratio decreased to 0.19x in FY19 from 0.24x in FY18. Considering the returns in the past few months, decent current ratio, Debt/Equity level, and the recent funding proposals, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.165 per share, up by 6.452% on December 23, 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...