.png)

Stocks’ Details

Orocobre Limited

Lithium Carbonate Pricing Estimates for Dec’19 Qtr Released:Orocobre Limited (ASX: ORE) is involved in the production and exploration of minerals and focuses on developing Lithium/Potash resources in Argentina. Recently, the company provided an update on expected lithium carbonate pricing for the December quarter, which was estimated to be around US$5,400/tonne Free on Board (FOB), subject to achieving the planned shipping schedule. With market conditions being soft, the company has made the decision to meet current pricing to ensure the retention of market share. Lithium chemical prices are expected to recover in the medium term from below incentive pricing for green-fields projects. Despite a reduction in the company’s price guidance for the quarter, operational and cost improvements are expected to limit the impact on its operating margin.

.png)

Quarterly Production and Sales Data (Source: Company Reports)

September’19 Quarter Key Highlights:Despite maintenance activity in August, production for the period was reported at 3,093 tonnes, as compared to 2,293 tonnes in pcp. Product sales were reported at 3,108 tonnes of lithium carbonate with an average price of US$7,111/tonne on an FOB basis. Total sales revenue for the quarter was reported at US$22.1 Mn. It is expected that full-year production for FY20 will be at least 5% higher than FY19. Average sales price in the December quarter is expected to be in the range of US$6,200 - US$6,500/tonne.

Stock Recommendation:ORE’s share generated a positive YTD return of 1.07%. The company’s balance sheet and business model position it as one of the low-cost lithium chemicals producers. Its gross margin and net margin for FY19 stood at 45.2% and 67.3%, better than the industry median of 41.1% and 11.7%, respectively, implying decent fundamentals of the company. Its ROE for FY19 improved from 0.5% in FY18 to 9.6% in FY19. Its current ratio for FY19 stood at 3.27x, better than the industry median of 1.75x, implying a decent liquidity position of the company. Considering the recent updates, September’19 Quarter performance, profitability margins and positive lithium global outlook, we recommend a “Buy” rating on the stock at the current market price of $3.040, up 7.042% on January 7, 2020.

Pilbara Minerals Limited

Cash Balance of ~$61 Mn at the end of Sep. Qtr:Pilbara Minerals Limited (ASX: PLS) is an Australian lithium-tantalum producer focussed on the development of its 100%-owned Pilgangoora Lithium-Tantalum Project.

September’19 Quarter Key Highlights:Production of spodumene concentrate at 6.06% Li2O was reported at 21,322 dry metric tonnes (dmt), as compared to 63,782 dmt in June Quarter. The period also witnessed the first sales contract for secondary tantalite concentrate signed subsequent to the quarter-end for 36,500 lbs (nominally 30% Ta2O5). In August, the company completed the first shipment to China’s Great Wall Motor Company, and the agreement involves the supply of 20,000 dmt per annum over a period of around six years.

Net cash outflow from operating activities for the period was reported at $28,761,000. Net cash outflow from investing activities for the period was reported at $11,493,000. Net cash inflow from financing activities for the period was reported at $37,820,000. Cash and cash equivalents at the end of the period were reported at $60,896,000.

.png)

September’19 Quarter Operating Cash Flow Statement (Source: Company Reports)

Financial Health of the company:Company’s current ratio for FY19 stood at 2.13x, better than the industry median of 1.75x, implying a decent liquidity position of the company.

Lithium Outlook:Weak customer demand in lithium raw materials especially in China, impacted spodumene exports from Western Australia. PLS responded to such conditions by actively moderating production, reducing costs and using available final product stocks to customer needs. Developments by battery and car manufacturers across the globe are expected to boost the demand for lithium-ion batteries, which is expected to help lithium miners and producers to boost earnings.

Valuation Methodology:Price to Book Multiple Approach

.png)

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock posted a negative YTD return of 3.28% and is currently trading close to its 52-week low level of $0.250, proffering an opportunity for stock accumulation. Considering the company’s recent developments, positive lithium long term outlook and current trading levels, we have valued the company using Price to Book Value based relative valuation method and arrived at a lower double-digit upside in percentage terms. Hence, we give a “Speculative buy” rating on the stock at the current market price of $0.315, up 6.78% as on 7 January 2020.

Galaxy Resources Limited

GXY Releases its Corporate Strategy for 2020:Galaxy Resources Limited (ASX: GXY) is an international lithium company with lithium production facilities in Australia, Canada as well as in Argentina. Recently, the company reduced its substantial stake in Lepidico Ltd from 9.35% to 8.095%, effective from December 23, 2019. In another update, S&P Dow Jones Indices announced separation of GXY from S&P/ASX 200 Index and S&P/ASX All Australian 200 Index, effective from December 23, 2019.

In another update, the company informed the market about its corporate strategy for 2020 and beyond. It is determined to advance its projects to create a sustainable, large scale, global lithium chemicals business via organic growth. It has concluded process test work for the Sal De Vida project and the optimised work has resulted in the improvement of lithium recovery. GXY aims to implement a lower activity mine plan at Mt Cattlin to reduce volumes and costs to maintain positive cash margins and preserving resource life.

.png)

GXY’s Global Operations Data (Source: Company Reports)

September’19 Quarter Key Highlights:During the period, the company inked an agreement with lenders to acquire the senior secured loan facility provided to Alita Resources Limited (ASX: A40). Its cash position at the end of the period was reported at US$169 million, with US$32 million of debt.

Financial Health of the company:The company’s EBITDA margin for H1FY19 stood at 30.9%, better than the previous half-year period. Its current ratio for H1FY19 stood at 4.97x, better than the industry median of 1.82x, implying a decent liquidity position of the company. Debt to equity ratio for H1FY19 stood at 0.07x, lower than the industry median of 0.09x.

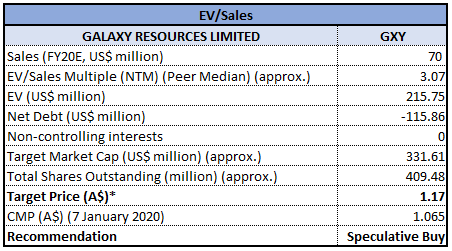

Valuation Methodology:EV/Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters), *1 USD = 1.45 AUD

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock posted a negative YTD return of 2.49% and is currently trading below the average of 52-week high and low levels of $2.415 and $0.815, respectively. Considering the company’s decent cash balance as on September 30, 2019, corporate strategy for 2020 and current trading levels, we have valued the company using EV/Sales based relative valuation method and for the purpose, we have taken the peer group Orocobre Ltd (ASX: ORE), Pilbara Minerals Ltd (ASX: PLS)and Altura Mining Ltd (ASX: AJM).Therefore, we have arrived at a target price of lower double-digit upside in percentage terms. Hence, we give a “Speculative buy” rating on the stock at the current market price of $1.065, up 8.673% as on 7 January 2020.

%20ORE.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...