Stocks’ Details

Galaxy Resources Limited

Strong balance sheet coupled with expectations of recovery in mining volumes: Galaxy Resources Ltd (ASX: GXY) has via a recent release provided the necessary details about the progress of the development activities which were undertaken by the company for the Sal-de-Vida project. The company has said that the transfer deed in respect to the sale of the northern tenement which is located at the Salar del Hombre Muerto have been inked with POSCO. However, this pact will take its official shape only after the same has been presented before the Salta courts for registration and the courts are slated to reopen in February 2019. Hence the consideration of US$280 million (less withholding tax of approximately US$8 million) will be released only after the registration is done.

For the quarter ended September 30, 2018, the firm had US$54.7 Mn in cash thanks to a healthy cash margin of US$ 411 per dmt and constant receipts from customers. The company enjoys debt free status as on September 30, 2018. This strong cash balance is constantly supporting the funding requirements for ongoing project development initiatives.

The company has registered lower production of spodumene at circa 31.2kt and cash margin per tonnes sold at US$411/dmt for the 3Q 2018 on account of the reduced recoveries. This was witnessed on account of permitting the delays in planned mining access on the east of floater road and the extraction of lower feed grade. However, the volumes are anticipated to show the signs of recovery in 4Q 2018 with the improvements in the grade and the recoveries related with the associated mining located at the east of floater roads.

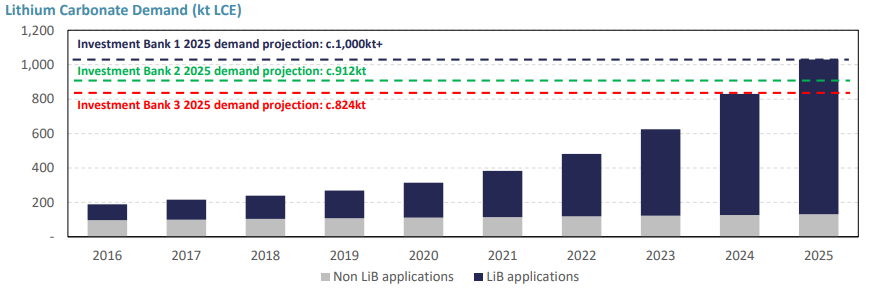

Going forth, therapid growth in lithium demand shall be driven by the penetration forecast which is expected to reach to a level of more than 15% of the automotive segment by the year 2025. Also, the Energy storage systems (ESS) has emerged as a critical component in managing the grid stability. Moreover, the high consumption of Electronic goods and its accelerated obsolescence will support the demand for lithium.

Forecasts of Global lithium demands (Source: Company Reports)

On the financial metrics front, the EBITDA margins for the 1H 2018 came in at 45.80%, while the same was negative in the pcp signifying a turnaround in the operations. Moreover, the company has no long-term debt on its balance sheet & hence has less financial leverage.

Meanwhile, the stock price has fallen by 26.32% in the past 6 months as on 09 January 2019. Thus, considering the strong balance sheet and expectations of recovery in mining volumes in the upcoming period, we maintain our “Hold” recommendation on the stock at the current market price of $2.30 (down 3.361% on 10 January 2019).

Orocobre Limited

Robust production outlook backed with underlying demand:Orocobre Ltd (ASX: ORE) stated via a recent release that the company has completed the third-Phase drilling program at Cauchari. It has started engineering for the feasibility study as well. The third-phase drilling enhanced the expansion of the resource area to the south with greater depths. The recent drilling has resulted in the intersection which is very encouraging and significant in the way that this is having similar physical structure and substance like the deeper holes drilled at Olaroz in recent past.

The production for the quarter ended September 2018 was 2,293 tonnes of lithium carbonate; this implies a rise of 7% on pcp. However, the same was down 36% on a Q-O-Q basis due to the shutdown of the plant for the two weeks and lower seasonal evaporation rates.

The company has posted strong sales of US$32 Mn for the quarter; this was a rise of 36% from the previous corresponding period. This growth was on the back of a surge in the average price realization per tonne which came in at US$14,699/tonne on an FOB basis. Also, the gross cash margins came in at US$10,059/ tonne, up by 62% on pcp, thanks to the higher average pricing realized driven by a better product mix and profitability of Olaroz operations. The company has available cash balance of US$308.7 as on 30 September 2018, thanks to the increase in the average price received per tonne.

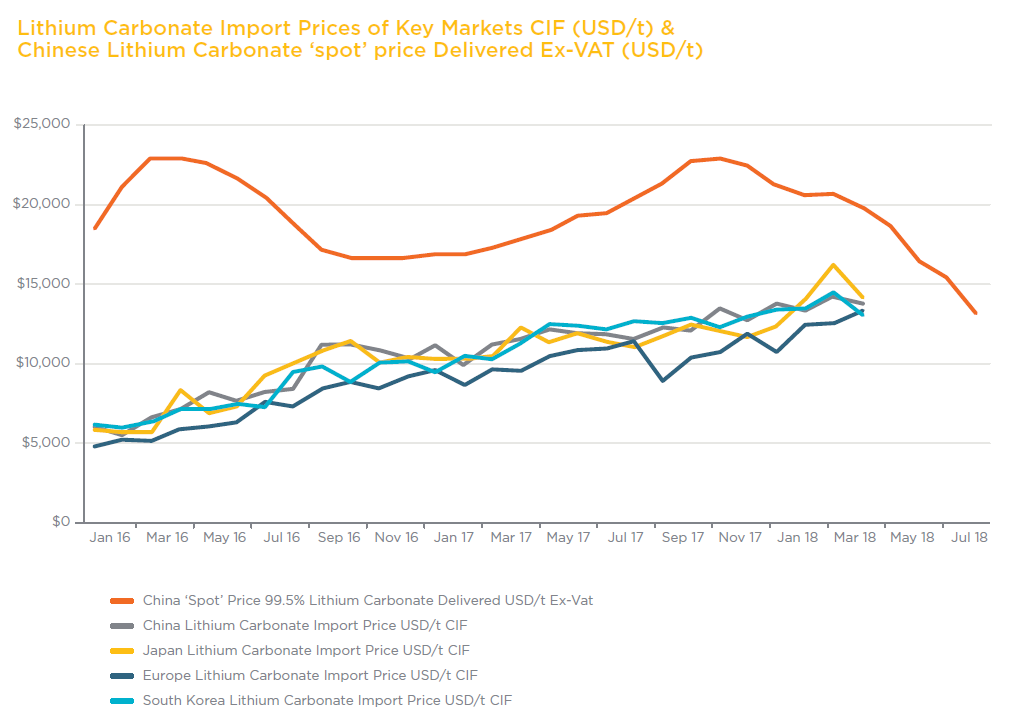

Orocobre expects full-year production for the FY 2019 to be higher than that achieved in FY18 on account of production contributed by Cauchari site.The December quarter production is expected to be significantly higher than the September quarter. However, the company feels that the average price realization per unit may decline going further due to the global price decline in lithium carbonate.

Global Lithium Carbonate Import Prices (Source: Company Reports)

As the firm is into an asset intensive business, the valuation on the net asset basis can be considered appropriate. The firm is trading at a Price to book of 1.30x while the Industry median is at 2.1x, thus the company seems undervalued at the current market price.

Meanwhile, the stock price has fallen over the past six months by 38.03% as on 09 January 2019 and is now looking attractive for accumulation in this price range. Moreover, fundamentally the company is sound enough which is evident from its balance sheet. Thus, considering the above rationale we maintain our “Buy” recommendation on the stock at the current market price of $3.33 (1.77% on 10 January 2019).

Kidman Resources Limited

Favourable market dynamics- a growth catalyst:Kidman Resources Limited (ASX: KDR) has through a recent ASX release made an announcement stating that it has entered an MOU with the LG Chem in relation to the supply of 12kt of lithium hydroxide p.a. to LG Chem over a term of 10 years. LG Chem has both agreed to work towards the execution of a binding Strategic Supply Agreement by 31 July 2019. This Memorandum of Understanding (MOU) with LG Chem is representing around 50 percent of Kidman’s share of lithium hydroxide production of 22.6kt per annum.

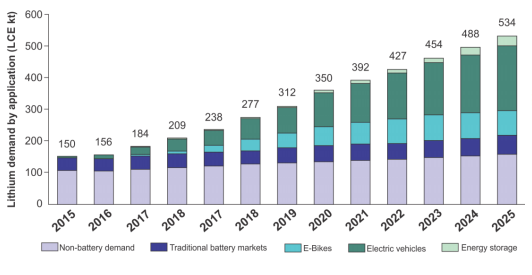

Going forth, it is believed that the Australian region has enormous potential to become a leader in the lithium space. The region is one of the major suppliers of lithium and spodumene production. Moreover, the growing investment will consolidate the region’s position in the global lithium market. Hence its estimated that the lithium demand is expected to expand at a robust rate till the year 2025 on the back of increased production of electric vehicles. The firm is expected to capitalize on the favourable market dynamics and to exhibit promising growth in the coming periods.

Forecasts of lithium demand correlated with application (Source: Company Reports)

Meanwhile, the stock price has fallen by 34.88% over the past six months as on 9 January 2019 and is trading at lower level.Hence considering the robust market outlook & growing demand for lithium due to electrification of vehicles, we maintain our “Buy” recommendation on the stock at the current market price of $1.110.

.PNG)

Stock Price Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...