Altura Mining Limited

Trading close to a 52-week low level: Altura Mining Limited (ASX: AJM) is a significant player in the global lithium market. The company recently declared commercial production of lithium from its fully owned Altura Lithium Mine. The company also conveyed that it has been inundated with strong demand from existing shareholders for the Company’s Security Purchase Plan (SPP) Offer announced on 7 February 2019. The Board has decided to increase the amount to be raised to $10.0 million from the original $5.0 million driven by the positive response. The increased maximum amount will minimize the prospect of any required scale-back of the SPP Offer applications. The SPP Offer Period closes on 15 March 2019 which is after the date of these accounts. The funds raised will be used by the Company primarily to finance the continued growth of its business activity, debt reduction, fulfill working capital requirement and development cost, etc.

.png)

1HFY19 Consolidated P&L Statement (Source: Company Reports)

From the analysis standpoint, the revenue from continuing operations improved by ~10.29% on the prior period to $450,000 for the half year period December 2018, primarily on the back of improved sales from mining services. Among the liquidity ratios, the company’s current ratio stood at 1.59x in FY 2018 which is higher than the industry median of 1.57x reflecting that the company possesses decent liquidity position. We expect that the decent liquidity position and current Security Purchase Plan (SPP) offer will support to meet its short-term obligation and provide sufficient headroom for future growth.

What to Expect From AJM: Going forward, the company wants to create shareholder value through the development of profitable mining operations and other supplementary mining activities that deliver strong cash flows for the group and results in dividends for shareholders on a regular basis.

Meanwhile, the share price of the company has fallen 22.86% in the past three months as at 12 March 2019 and is trading close to a 52-week low level of $0.120 showing an opportunity to enter the stock at lower levels. By looking at the current trading scenario and decent outlook backed by higher demand of lithium product around the globe, we maintain our “Speculative Buy” recommendation on the stock at the current market price of A$0.145 per share.

Kidman Resources Limited

Strong demand outlook for lithium driven by penetration in electric vehicles: Kidman Resources Limited (ASX: KDR) is into the business of lithium development, coupled with the development of the Tier-one Mt Holland Lithium Deposit in Western Australia. Recently, the company has given a notice of change in the director’s interest relating to an indirect interest of Mr. Southam in the company’s securities. As per the release, the change has arisen since Mr. Southam stopped to be an employee of Western Areas Limited (Western Areas) from 31 January 2019. Mr. Southam had an indirect interest in the securities held by Western Areas through his position as an Executive Director and employee of that company.

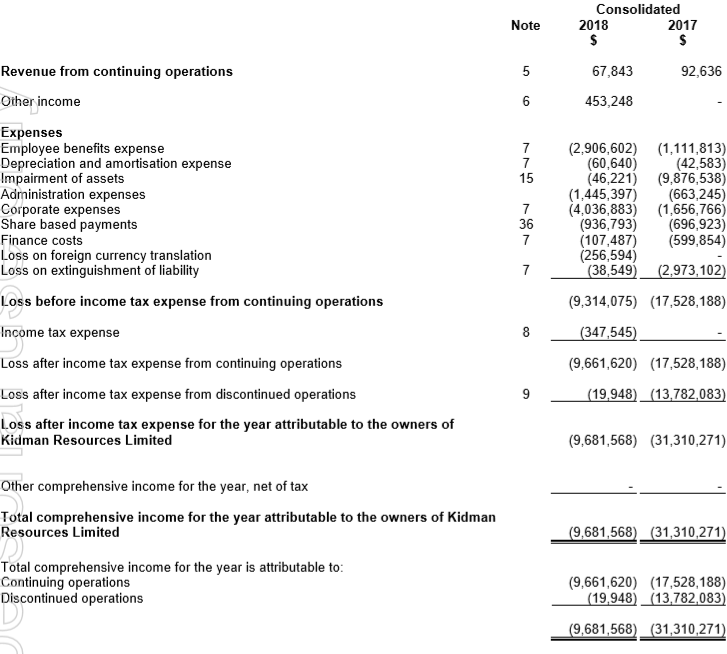

Income Statement (Company Reports)

On the financial front, the operating cash outflow of the company was $5.26 million for the quarter ended 31-December 2018. The cash & cash equivalents stood at $30.86 million as at 31 December 2018 as compared to the prior quarter where the same was $7.98 million. Among the key ratios, the current ratios improved by 35.0% Y-o-Y to 0.56x in FY18 as compared to 0.42x in FY17.

Optimistic outlook: The company is progressing well, to become a low-cost, integrated producer of lithium hydroxide for the growing electric vehicle market. It has significant resources globally of high quality which is in the tier one mining jurisdiction of Western Australia. It has also significant funds which can support the initial stages of project CapEx, with offtake arrangements providing support as well for the ongoing bank financing discussions of the company. There is a strong demand outlook with the demand for lithium supported by increasing penetration in electric vehicles with lithium hydroxide being used as fastest growing battery types.

Meanwhile, the share price of the company has fallen 16.67% in the past one month as at 12 March 2019 and is trading below to the average of 52 weeks high and low level of ~$1.65. Since its listing on ASX, it has posted a return of 445.45%. Hence, considering the strong demand outlook for lithium and robust project economics, we give a “Buy” recommendation on the stock at current market price of $1.220 (up 1.667% on 13 March 2019)

Galaxy Resources Limited

Strong balance sheet coupled with no debt: Galaxy Resources Limited (ASX: GXY) is into the exploration of minerals and production of lithium concentrate in Australia, Canada, and Argentina. The primary focus of the company includes exploration for minerals and the production of Lithium Carbonate.

The company has received US$271.6 million from POSCO driven by the sale of the package of tenements located on the northern portion of the Salar del Hombre Muerto. This amount includes the transaction sale price of US$280 million, excluding US$8.4 million in withholding taxes, earlier paid in November 2018 and comprises US$257 million consideration previously held in escrow by the Escrow Agent, and US$14.6 million payable by POSCO directly to Galaxy within 5 business days of completing the registration of certain usufruct transfers.

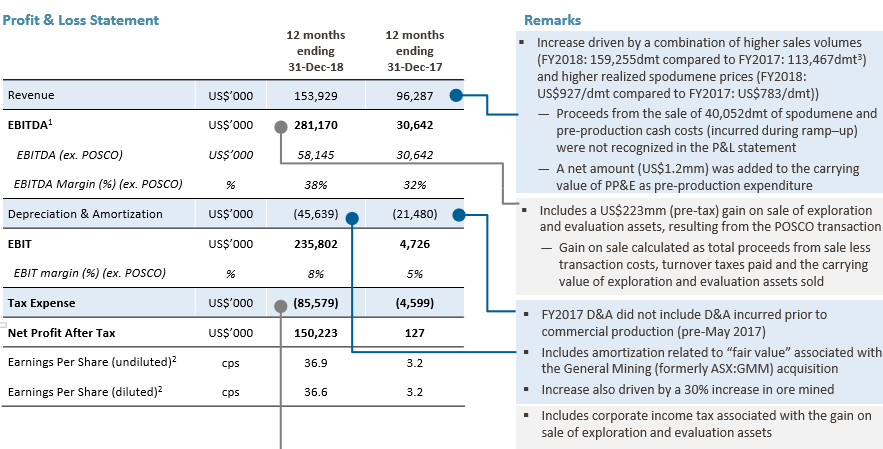

Profit & Loss Statement (Source: Company Reports)

The revenue of the company stood at US$153.92 million in FY18 as compared to US$96.28 million in FY17, an increase by 60.0% Y-o-Y driven by a combination of higher sales volumes and higher realized spodumene prices. The reported net profit after tax stood at US$150.2 million which included a gain on sale of US$146.8 million (after-tax) arising from the POSCO transaction. The Group net profit after-tax for the year, excluding the POSCO gain was US$3.5 million, representing a 26-fold increase compared to FY2017.

During FY18, the company reported higher than industry EBITDA margin of 35.3% as compared to the industry median of 30.9%. Further, the returns generated for the shareholders have improved over the years as the ROE was -42.0% in FY14 which has turnaround to positive RoE of 30.1% in FY18 with an average growth of 19.9% per annum.

Meanwhile, the stock price of the company has risen 3.09% in the past one month but down by 5.21% in the past one week as on March 12, 2019. Hence considering the volatility in the stock and robust lithium demand coupled with ramp-up spodumene production in Q1 2019 and exploring potential downstream opportunities with the existing customers, we maintain our “Hold” recommendation on the stock at the current market price of $1.980 (down 1% on 13 March 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...