Bank of Queensland Ltd

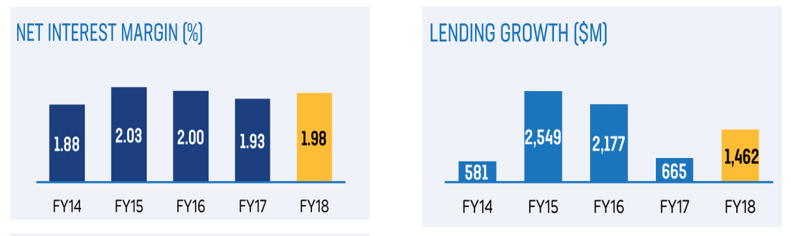

Inclination towards digitization and Higher NIM Underpinned FY 2018 Results:Bank of Queensland Ltd (ASX: BOQ) delivered a decent performance in FY 2018 on the back of lending growth as well as a rise in the net interest margin or NIMs. The bank’s lending in FY 2018 stood at $1.4 billion while in FY 2017 it was $665 million. The company’s management stated that its asset quality with respect to the loan portfolio has witnessed the favourable impact and this has been regarded as the “key strength” for BOQ.

BOQ’s NIMs and lending growth (Source: Company Presentation)

The bank is well-positioned to witness the long-term growth thanks to the improvements with respect to business mix, geography as well as channels. Of the total loan portfolio, the loans which have been garnered via BOQ specialist as well as Virgin Money Australia make up for 20% in FY 2018. Up till now, these businesses have been witnessing the decent organic growth and the management expects this momentum to continue moving forward. The bank has been working rigorously in the digital space and has witnessed some sort of progress. It has been working to reduce its dependency on the manual work procedures. The bank’s lending activities in FY 2018 were aided by the deposits.

What challenges banking sector has encountered in FY2018: It would not be wrong to infer that FY2018 has been a tough one for the banking sector. Broadly the sector witnessed higher regulatory pressures as well as public scrutiny. Apart from this issue, weaker credit growth as well as a change in the customer expectations have continued to impact the banking sector’s performance. Amidst all these factors, Bank of Queensland witnessed the revenue growth of 2% YoY to $1.1 billion which was underpinned by a rise in the NIMs of 5 bps (basis points).

Amidst Challenging Economic Environment, BOQ Plans to Work on Digitization: Moving forward, the banking sector is expected to face the challenging environment because of the Royal Commission’s interim report which highlighted certain concerns prevailing in the Australian banking sector. However, the management is optimistic about the outlook and expects that it would face opportunities as well.

Some of the challenges which might be encountered by the banking industry are weakening of the credit growth, subdued growth with respect to the wages as well as falling house prices. These could impact the top line numbers of the companies operational in the financial sector. In FY 2019, the bank is expected to remain committed towards the digital space as well as it plans to streamline the banking platform.

Technical Overview: On the daily chart of Bank of Queensland, a momentum indicator, Relative Strength Index or RSI, has been applied by considering the default values. As per the observation, the 14-day RSI is noted at the border level. A breach would lead to the entry in the oversold region. Hence, a rebound is expected to occur i.e. a bullish momentum is expected to be built. Hence, we maintain our “Buy” rating on the stock at the current market price of A$9.960 per share. The stock was down 5.5% on October 24, 2018, as it traded ex-dividend.

MyState Limited

FY 2018 Mainly Helped by Lower Expenses, Deposits Growth: MyState Limited (ASX: MYS) ended FY 2018 with total customer deposits amounting to $3.2 billion reflecting YoY growth of 9% thanks to the launch of eSaver as well as Everyday transaction accounts. The bank has managed to work on the policy of disciplined cost management as it is evidenced from the fall of 1.5% as compared to the prior corresponding period in the operating costs in FY 2018. The management reflected positive views with regard to the cost management initiatives.

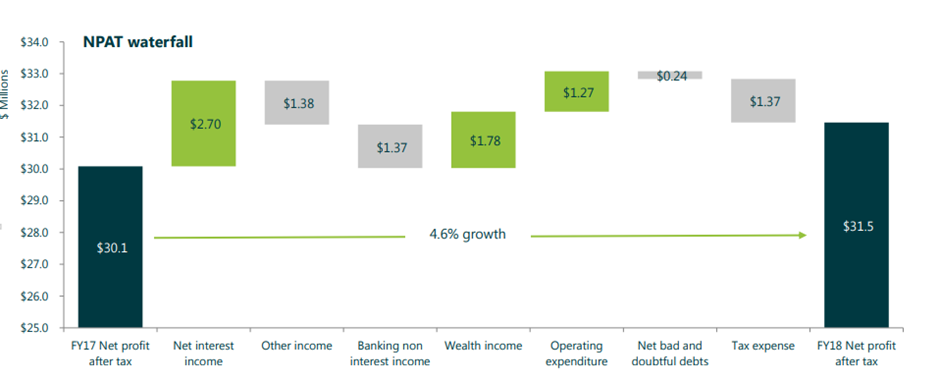

MyState’s NPAT (Source: Bank’s Presentation)

The decline in the costs would help MyState to focus on the investments towards digital tools, marketing activities as well as customer acquisition. However, depreciation and amortization expenses rose in FY 2018 as compared to the prior corresponding period because the increased investments in the digital assets had started to amortise. As compared to FY 2017, the bank witnessed a rise of 4.6% in NPAT to $31.5 million which was mainly underpinned by the robust momentum witnessed in the net interest income or NII and wealth income.

Increased Funding Costs, Regulatory Pressures to Impact Broader Sector: The management of MyState views that the competition in the lending markets is likely to prevail moving forward. Apart from that, higher funding costs might be a headwind for the overall sector. The bank has plans to work towards improving the digital tools which could help it in easy as well as faster onboarding of the customer.

It has plans to work for the customer satisfaction and thus, would be working to enhance and improve its digital platform. MyState Limited is also working to make deployments in the Wealth. Apart from that, bank would also be working towards the cost reduction initiatives.

Technical Overview: Two technical indicators have been used on the daily chart of MyState Limited i.e. Moving Average Convergence Divergence or MACD and Relative Strength Index or RSI and default values have been considered. As per the observation, the MACD line has crossed the signal line and is moving downwards. However, when we see 14-day RSI, the stock might soon reach in the oversold zone and then a rebound might happen. Thus, at the current price of A$4.600 per share, we maintain our “Hold” rating on the stock.

CYBG PLC

NII rose 4% Aided by Volumes and NIMs: CYBG PLC (ASX: CYB) generated net interest income or NII amounting to £426 million in the six months ended March 2018 which implies the YoY growth of 4% on the heels of robust volume growth as well as rise in the NIM of 218 bps (basis points). During the same period, the bank saw YoY decline of 10% mainly because of non-recurring marketing incentive expenses.

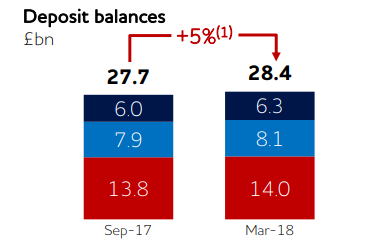

CYBG’s deposit balances (Source: Bank’s Presentation)

For six months ended March 2018, the bank’s deposit balances rose to £28.4 billion implying the rise of 5%. This growth reflects the strength of the bank’s funding platform. The positive momentum witnessed in CYBG’s asset quality represents that the bank has been following prudent underwriting standards.

Digital Tools to Help CYBG Moving Forward: With the help of iB platform, CYBG plans to improve the digital experience which could help it in the long-term. Therefore, it might increase its focus towards the digital tools which might result in increased investments. The company has been making efforts to improve the experience of its SME or Small and Medium Enterprises customers.

The customer lending platform, robust technology platform as well as strengthened capital position are the primary factors which underpins CYBG’s capability to carry out operations in the challenging environment. The management also has optimistic outlook for the bank.

Technical Overview: On the daily chart of CYBG PLC, Relative Strength Index or RSI has been applied by using the default values. The 14-day RSI was earlier in the oversold region and witnessed a small rebound. However, it did not last long, and the 14-day RSI was again seen in the oversold region. Therefore, we suggest to wait and watch the stock at the current price of A$4.740.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...