.png)

Stocks’ Details

Fortescue Metals Group Limited

Investment in New Projects: Fortescue Metals Group Limited (ASX: FMG) is engaged in the mining, processing and transportation of iron ore from its deposits within the Pilbara area of Western Australia. The market capitalisation of the company stood at A$35.13 Bn as on 20th January 2020. The company recently announced that Hunan Valin Iron and Steel Group Co., Ltd, and its related bodies corporate has made a change to their substantial holding in the company on 13th January 2020, and the current voting power stands at 11.7941% as compared to the previous voting power of 13.0600%. Also, in the recent presentation, the company mentioned that it is driving growth with the help of investment in new projects, which is supporting the purposefully designed breadth of the product offering of FMG. The following picture provides an idea of the financial performance of FY19:

.png)

Financial Performance FY19 (Source: Company Reports)

Guidance for Year Ahead: For FY20, the company is expecting shipments in the range of 170mt -175mt and C1 cost/wmt in the vicinity of US$13.25 - US$13.75. The company has also forecasted a capital investment for the financial year 2020 amounting to US$2.4 billion. The company is aiming for a dividend payout in the ambit of 50-80% of NPAT.

Valuation Methodology: P/E Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The key strategic focus of the company is to strengthen the balance sheet, maintain long-term sustainability, and continued growth and development while delivering returns to shareholders. Net margin of the company stood at 32.0% in FY19 as compared to the industry median of 10.9%. This reflects that the company has better capabilities to convert its top-line into the bottom-line as compared to the broader industry. We have valued the stock using a P/E based relative valuation approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Therefore, considering, the investment of the company in new projects, strong demand for its products, and return to shareholders being a strategic focus, we give a “Hold” recommendation on the stock at the current market price of A$11.830 per share, up by 3.681% on 20th January 2020.

BHP Group Limited

BHP Eyeing Strong Free Cash Flow: BHP Group Limited (ASX: BHP) is engaged in the exploration of minerals as well as production, refining and exploration of hydrocarbons. The market capitalisation of the company stood atA$119.6 Bn as on 20th January 2020. The company recently announced that Terry Bowen, who is the director of BHP Group Plc and BHP Group Limited, has been appointed on the Board of Transurban Group, effective 1st February 2020. In another update, the company stated that the retirement date of Andrew Mackenzie would be 31st March 2020. The below picture depicts an overview of interim dividend dates for 2020:

.png)

2020 Interim Dividend (Source: Company Reports)

Confident to Fight against any Future Volatility: The company is optimistic that it is placed well to ride out any future volatility on the back of its strong balance sheet, low-cost operations, and successful capital allocation framework.

Valuation Methodology: P/E Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The portfolio of quality assets as well as a pipeline of competitive growth options are anticipated to report strong free cash flow and returns through the 2020s and beyond. The company can deliver on its plans for the future with its capabilities in safety, exploration and deepwater operations, in combination with a high-performance culture. We have valued the stock using a P/E based relative valuation approach. For the purpose, we have taken the peer group - Rio Tinto Ltd (ASX: RIO), South32 Ltd (ASX: S32), and Alumina Ltd (ASX: AWC) and arrived at a target price upside of lower double-digit (in percentage terms). In light of a decent outlook, portfolio of quality assets, and anticipated cash flows, we maintain a “Hold” rating on the stock at the current market price of A$41.240 per share, up by 1.576% on 20th January 2020.

Rio Tinto Limited

Ended the Financial Year with Decent Set of Numbers: Rio Tinto Limited (ASX: RIO) is involved in the production of copper, gold, iron ore, coal, aluminium, etc. The market capitalisation of the company stood at A$39.07 Bn as on 20th January 2020. The company recently announced that one of the non-executive directors, Simon McKeon has been appointed as a non-executive director of National Australia Bank Limited with effective from 3rd February 2020. The company ended the financial year 2019 with good momentum, mainly in its Pilbara iron ore operations and in bauxite, irrespective of the operational challenges in 2019. The company is increasing its investment, with $2.25 billion of high-return projects in iron ore and copper approved in the fourth quarter. The company increased its exploration and evaluation expenditure to $624 million in 2019, further strengthening its pipeline of opportunities.

.png)

Production Results for Q4 FY19 (Source: Company Reports)

Focus on Strengthening the Balance Sheet: The company increased its exploration and evaluation expenditure to further strengthen its pipeline of opportunities. The company’s strategy revolves around strengthening the balance sheet, generating superior shareholder returns and creating growth options.

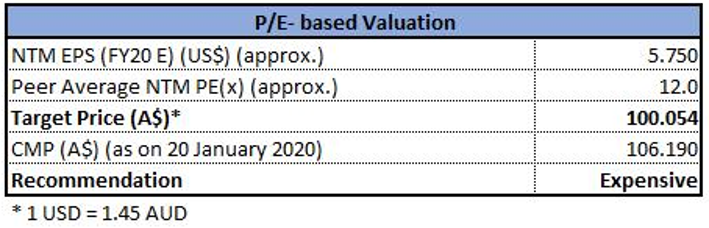

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company possesses the potential for maintaining the delivery of superior returns to shareholders over the short, medium as well as long-term, which is driven by its strong value over volume approach and ongoing disciplined allocation of capital. As per ASX, the stock is trading close to its 52-week high of A$107.130. We have valued the stock using P/E based relative valuation approach, and for the purpose, we have taken peers such as BHP Group Ltd (ASX: BHP), Fortescue Metals Group Ltd (ASX: FMG), and Iluka Resources Ltd (ASX: ILU) and arrived at a target price, which is offering a correction of lower single-digit (in percentage terms). Thus, considering the stretched valuations and current trading levels, we give an “Expensive” recommendation on the stock at the current market price of A$106.190 per share, up 0.903% on 20th January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...