Magellan Global Trust

Constant Growth in Assets & stable returns: Magellan Global Trust (ASX: MGG) has recently reported its weekly NAV per unit of Magellan Global Trust and recorded the same at $1.6738 as at 8 February 2019, an increase of 1.6% in NAV from $1.642 as on February 01, 2019. Through the latest Fund update for the quarter ended December, the company stated it has the highest exposure in the consumer defensive segment with an 18% allocation. In terms of geography, the trust is heavily invested in the U.S. markets with a 48% stake. MGG reported a negative return for December quarter wherein MGG Investment Portfolio delivered a return of -7.8% in three months (as of 31 December 2018) as compared to MSCI World Net Total Return Index (AUD) returns of -11.0%, exhibiting rise of 3.2%. The portfolio witnessed a negative performance for the December quarter because of tighter US monetary policy, tensions between China and the US, key resignations from the US administration, and political uncertainty in Europe fanned doubts about the global economic outlook, etc. The stocks which underperformed included the likes of Apple, Facebook and Kraft Heinz. Since inception, MGG Investment Portfolio generated 8.7% returns per annum against the MSCI World Net Total Return Index returns of 4.7% p.a. As at 31 December 2018, the trust has a total funds size of approximately A$1,651.5 Mn.

.png)

Fund Performance Since Inception (Source: Company Reports)

Although, the group has a cautious outlook going forward considering that the funds’ performance entirely depends upon the performance of the business it has invested in. However, considering the fact that the assets price is at their record all-time highs, major central banks across the world are tightening their stance towards interest rates which will result into less liquidity infusion into markets going forward. Meanwhile, the stock price has risen by 9.33% in the past one year as on 8 February 2019 and is trading at a reasonable PE level of 9.74x. By looking at its historical investment return performance and considering the expectations of a robust U.S. economy going forward, we, therefore, maintain our “Buy” recommendation on the stock at the current market price of $1.625 (down 0.915% on 11 February 2019).

MFF Capital Investments Limited

Rise in weekly NTA: MFF Capital Investments Limited (ASX: MFF) has reported an NTA per share as at Friday, February 8, 2019, of $2.909 pre-tax. The NTA per share as at Friday, February 1, 2019, was $2.849 pre-tax, hence a rise of 2.11%.Moreover, the company has posted its numbers for the half year ended 31 December 2018 wherein it reported a net loss after income tax of $12.96 Mn. This loss was predominantly on account of the mark to market reductions in the market value of the Company’s portfolio. The company’s Net assets decreased by $19.54 Mn & came in at $1,218.65 Mn. This fall in assets was primarily on account of the market price movements for the Company’s investment portfolio as well as the dividend payment in the period. As regards the outlook, the company investments are focussed towards the equities of non-Australian domiciled companies & will remain so. The management doesn’t consider it to be fruitful to give any broad outlook in view of fluctuations.

.png)

MFF’s Net Tangible Assets Per Share (Source: Company Reports)

Meanwhile, the stock price has risen by 6.20% in the past one month as on 8 February 2019 and is trading at a reasonable PE level of 13.95x. The company had reported an ROE of 21.90% and a net margin of 68.4% for the year ended June 2018, which is decent enough for the concerned industry. Hence, considering the robust ROE’s and a constant rise in the NTA’s, we maintain our “Buy” recommendation on the stock at the current market price of $2.78 (up 1.46% on 11 February 2019).

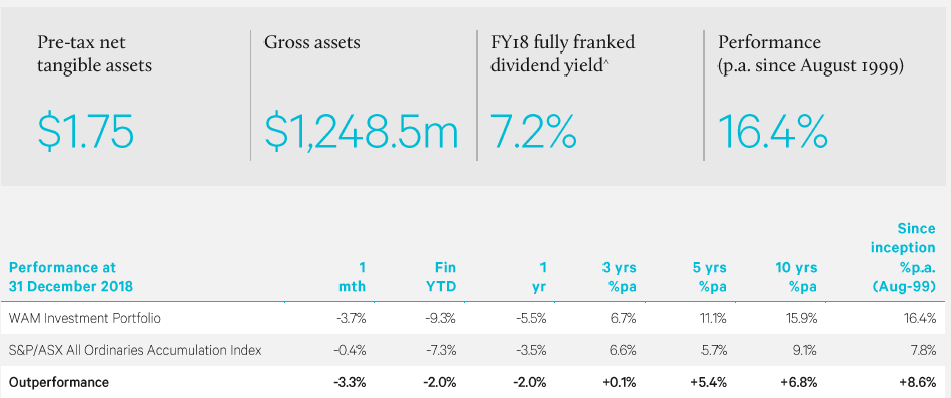

WAM Capital Limited

Constant Growth in Assets: WAM Capital Limited’s (ASX: WAM) Investment portfolio fell by 3.70% in the month of December 2018. This fall was on account of the subdued performance witnessed in the GTN and EMECO holdings.EMECO holdings fell on account of the earnings downgrade from the management due to the weakness in the Australian geographical segment. EHL was impacted by the concerns of a slowdown in economic activity. Further, the fund remains bearish on the Australian equities as a whole and anticipates the year 2019 to remain challenging. Thus, considering this the fund will continue holding high levels of cash to manage risk & ensure the needed liquidity. The management is of the view that the next bear market will provide some of the rarest opportunities to pick undervalued growth companies.Since inception, WAM Investment Portfolio generated 16.4% returns per annum against the S&P/ASX All Ordinaries Accumulation Index returns of 7.8% p.a.As at 31 December 2018, the group has Gross asset of approximately A$1,248.5 Mn with pre-tax net tangible assets of $1.75 per share.

WAM Capital’s December 2018 portfolio performance (Source: Company Reports)

Meanwhile, the share price has receded by 5.56% in the past three months as 8 February 2019 and is trading at reasonable PE multiple of 11.45x. The company had a pre-tax margin of 88.7% and an ROE of 9.90% for the year ended June 2018 which is decent enough as per the concerned industry standards & showing a better delivery of returns to the shareholders. Hence, considering an outperformance achieved in the long term compared to the benchmark as well as decent margins along with the respectable ROE, we maintain our “Buy” recommendation on the stock at the current market price of $2.18 (down 1.357% on 11 February 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...