.png)

Stocks’ Details

The A2 Milk Company Limited

Insights into Macquarie Australia Conference:The A2 Milk Company Limited (ASX: A2M) is into the business of producing, marketing and selling branded dairy and infant formula products in the targeted global markets. On 1st May 2019, the company released its presentation of Macquarie Australia conference.With respect to trading performance for 9 months to 31st March 2019, ithad witnessed a rise of 42% to NZ$938 Mn on pcp basis, which is supported by continued sales growth in nutritional products and liquid milk. With regards to 2HFY19, it was mentioned that the company is accelerating its strategic investment in the brand, consumer insights, and organizational capability. A2M is building depth and breadth of organizational capability and infrastructure. In the context of Australia & New Zealand, there was continued strong performance throughout all key product segments such as liquid milk, infant formula, and other nutritional products along with strong underlying brand health.

.png)

Group Revenue and EBITDA Trend (Source: Company Reports)

Future Aspects:The company had invested strongly in the 1HFY19 in internal and external capability, and this has been continued in the second half, and continue to invest in FY20 by this rate. The company is reinvesting its benefits of scale towards increased marketing activities in the second half after the very strong first-half performance and encouraged by growing market share in China.

Stock Recommendation: A2M stated that the second half EBITDA margins would consequently be lower than the first half. Adding to that, the company expects FY19 EBITDA as a percentage of sales in the range of ~31-32%. With respect to stock’s past performance, it had witnessed a rise of 7.73% and 45.99% in the time span of three months and six months, respectively. As per ASX, the company’s stock price is trading slightly towards the 52-week higher levels of $16.08 with high PE multiple of 46.38x. Hence, considering above stated parameters and looking at the current trading level, we give an “Expensive” recommendation on the stock at the current market price of A$14.580 per share (down 2.279% on 30 May 2019).

Bellamy's Australia Limited

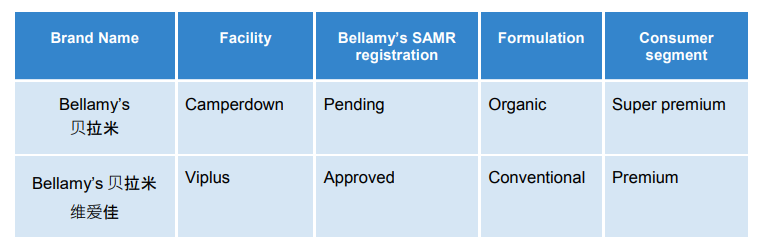

New Bellamy’s Branded Series:Bellamy's Australia Limited (ASX: BAL) is involved in the manufacturing and distributing of branded food products with a market capitalisation of ~A$1.02Bn as on 30th May 2019. The company, through a release, updated the market about the series of approvals, which was announced by SAMR. Adding to that, those approvals include Bellamy’s branded formulation-series which is to be produced at the ViPlus Dairy facility in Toora, Victoria. The company pointed out that the initial interest and feedback is very strong, which had come from sub-distributors.

The existing Bellamy’s organic series is to be produced at Camperdown Powder and it is also intended to target the super-premium segment of the offline channel in Tier 1, 2, and 3 cities.

Production Location of Bellamy’s organic Series (Source: Company Reports)

Future expectations:The company continues to maintain its zero debts levels, with access to $40Mn debt facility. It is planning to double its marketing spend in 2HFY19, and planning to double its China sales and Marketing team in the same period for activating brands. The company is very confident in the medium-term rebrand and portfolio opportunity. With respect to FY19, The Group EBITDA margin is revised by the company and is now in the range of 18-22% on a normalised basis, which is reflecting the increased investment in marketing and China team.

Stock Recommendation:The company remains confident in the application and expects Australian Audits in CY2019. In the context of the cash balance, the company pointed out that it has been increased by $7Mn to $95Mn. The current ratio of the company stood at 4.84x in 1HFY19 in comparison to the industry median of 1.42x, depicting its decent position to address the short-term obligations. With respect to stock’s past performance, it had offered returns of 1.93% and 23.12% in the time span of three months and six months, respectively. However, in the time span of one-month, the stock had witnessed return of -19.28%. Based on the foregoing, we reiterate our “Speculative Buy” recommendation on the stock at the current market price of A$8.690 per share (down 3.444% on 30th May 2019).

Bubs Australia Limited

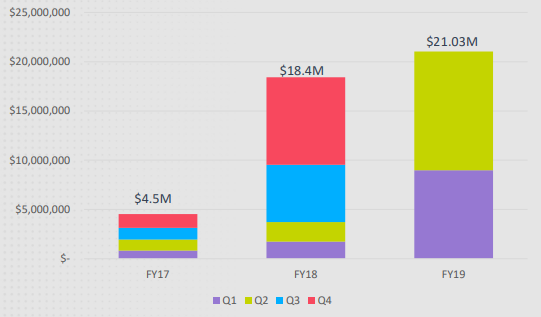

Synergistic Agreements- Support Growth Momentum: Bubs Australia Limited (ASX: BUB) is an Australian registered company, which is involved in manufacturing of infant milk formula with a market capitalisation of ~A$649.73Mn. Recently, the company disclosed that one of its directors, Kristy-Lee Newland Carr offloaded its 4,000,000 shares for personal reason in relation to acquiring a new family home. Post-development, she holds 16,761,600 ordinary shares with 4,770,810 unlisted options. In another release on ASX, the company announced that it has inked a joint venture agreement with Beingmate Baby & Child Food Co., Ltd, and a Strategic Partnership Agreement with Alibaba’s Tmall. Additionally, it had also formalised an equity linked alliance with CW Retail Pty Ltd, CW Management Pty Ltd, and CW Retail Services Pty Ltd, which was announced on 18th April 2019. These strategic agreements will support its growth momentum in years to come. In 1H FY19, the gross revenue stood at $21.03 million, which is 14.29% higher than the full year of 2018.

Group Quarterly Gross Sales Revenue (Source: Company Reports)

What to Expect From BUB: As per the Annual Report, the company is investing in building its organizational capacity. For FY19, the company has mentioned some strategic priorities like innovation & product development, increased domestic market penetration, vertical integration & supply chain and china channel development & partners.

Stock Recommendation:From the analysis standpoint, current ratio stood at 3.17x in 1HFY19, which is higher than the industry median of 1.42x, showing its decent liquidity position to address the short-term obligations in comparison to the broader industry. Asset-to-equity ratio stood at 1.34x in 1HFY19, when compared to the industry median of 1.97x and, thus, it looks like that the company is mainly relied on the equities to finance its assets.Moreover, the company focuses on building a robust platform for long-term growth. With respect to stock’s past performance, it had delivered a return of 10.39% and 127.68% in the time span of one-month and three-months, respectively. However, in the time span of the previous five days, it had given a return of -2.67%. Hence, considering aforesaid facts and current trading level, we give a “Speculative Buy” recommendation on the stock at the current market price of A$1.245 per share (down 2.353% on 30th May 2019).

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...