.png)

Stocks’ Details

Orica Limited

Improved Product Demand Drives Business Growth: Orica Limited (ASX: ORI) is a provider of commercial explosives and innovative blasting systems used for the mining, quarrying, oil and gas and construction markets.

FY19 Operating Highlights for the year ended 30 September 2019: Orica Limited reported its full-year financial numbers wherein the company posted sales revenue of $5,878 million as compared to $5,374 million in the previous financial year. ORI reported a statutory net profit of $245 million as compared to a loss of $48 million in FY18. EBIT on an underlying basis, stood at $665 million, up 8% on y-o-y basis. Growth in EBIT was aided by strong performance across all regions, particularly EMEA. During FY19, the company witnessed significant contributions from technology products, GroundProbe™ and Minova. The period also saw an improvement in manufacturing performance. The company reported a 4% growth in total AN product volume, led by strong growth in Latin America. ORI also reported that rectification work for Burrup is progressing in line with the announced plan.

.png)

FY19 Income Statement Highlights (Source: Company Reports)

The company announced an 85% unfranked dividend of AUD 0.3300 for each ordinary share, payable on 13 December 2019.

Guidance: Due to higher demand in Australia and new contracts in the Pilbara, volumes are expected to strengthen in FY20. The company expects further take-up of its market-leading technology solutions. ORI expects earnings contributions from the Burrup plant in the second half of FY20. Improvement in EBIT margins are also anticipated as the plant reached full production. As per the Management guidance, FY20 capital expenditure is anticipated between $370 million and $390 million.

Stock Recommendation: The stock of ORI is quoting at $23.730 with a market capitalization of $8.72 billion. 52-week trading range of the stock stands at $16.230 to $23.890, and the stock is trading close to the upper end of the range. The stock has generated decent returns of 9% and 23.66% during the last three-months and six-months, respectively. ORI’s has seen improvement in manufacturing and cost performance across the board. The business has seen higher traction with customers for its market-leading technology solutions. ORI’s efforts to improve every aspect of operations within the control has started to deliver positive results for the business. Considering the aforesaid facts, price movement and business prospects, we have a 'wait and watch' view on the stock at the current market price $23.730, up 3.624% on 01 November 2019.

Orora Limited

Improved Consumer Demand to Aid Profitability Growth:Orora Limited (ASX: ORA) provides an extensive range of tailored packaging and visual communications solutions to its clients. The services include designing and manufacturing of packaging products such as glass bottles, beverage cans, corrugated boxes, recycled paper, multi-walled paper bags and point of purchase displays. Recently, ORA informed that one of its directors, named Jeremy Leigh Sutcliffe has acquired 3,037 ordinary shares for a consideration of $2.8568 per share.

FY19 Operational Highlights for the year ending 30 June 2019: ORA reported its full-year financial results wherein the company posted sales of $4,761.5 million, up 12.1% on y-o-y basis and NPAT of $217 million as compared to $208.6 million in the previous financial year. During the year, the company reported EBIT of $335.2 million, up 3.7% on y-o-y basis. During FY19, the company reported higher net debt at $890 million as compared to $667 million on the previous financial year, primarily driven by recent growth investments and impact of FX. Australasia segment reported EBIT at $246.6 million, up 6.2% on y-o-y basis, as a result of organic growth in fibre segment supported by the asset refresh program. Beverage earnings in Australasia were higher than pcp due to stronger Can volumes and continuous improvement in operating efficiencies across both Cans and Glass. In the North American segment, EBIT went down 3.6% on y-o-y basis to $116.6 million.

.png)

FY19 Financial Highlights (Source: Company Reports)

Outlook: As per the management, Orora Limited will continue to invest in efficiency, growth and innovation while integrating recent acquisitions into business operations.

Stock Recommendation: The stock of ORA is quoting at $3.110 with a market capitalization of $3.73 billion. The stock has a 52-week trading range of $2.600 to $3.470. The stock has generated returns of -8.58% and 0.32% during the last three-months and six-months, respectively. In FY19, the company has delivered decent revenue growth despite a challenging sector outlook. ORA continued to strengthen its business by investing in growth and innovation initiatives, with approximately $300.0 million invested in acquisitions, organic capital projects and innovation. With a strong balance sheet in place, the company has laid down a foundation for further business growth. Considering the above factors, we recommend a ‘Hold’ rating on the stock at the current market price of $3.110, up 0.647% on 01 November 2019.

Downer EDI Limited

Robust Bottom-line Growth aided by Strong Urban Demand: Downer EDI Limited (ASX: DOW) is a leading provider of integrated services in Australia and New Zealand. The company recently updated that Vinva Investment Management ceased to be a substantial holder.

FY19 Operational Highlights for the period ended 30 June 2019: DOW declared its financial results, wherein the company reported total revenue at $12,812.7 million, up 6.5% on y-o-y basis, driven by growth in Utilities, EC&M and Mining segments. Profit after income tax during the year stood at $276.3 million as compared to $71.1 million in the previous financial year. Underlying EBITA margin for FY19 came in at 4.2%, up 0.4% from FY18. EBITA from transport services came in at $242.4 million, up 22.5% on y-o-y basis. EBITA from the mining segment came in at $76.7 million, representing a significant increase of 52.2% on y-o-y basis.

.png)

FY19 Financial Highlights (Source: Company Reports)

Outlook: Downer is targeting NPATA of around $365 million before minority interests for FY20, depicting a growth of 7.3% on y-o-y basis.

Stock Recommendation: Thestock of DOW is quoting at $8.090 with a market capitalization of $4.79 billion. The stock has generated returns of 11.5% and 2.16% during the last three-months and six-months, respectively. In FY19, the company reported a decent cash conversion of 89.0% of EBITDA. The company has seen continuous growth acrossurban services businesses, including transport, utilities and facilities, and has a strong pipeline of opportunities across all the markets. The stock is available at an enterprise value (EV) to sales multiple of 0.5x on trailing twelve months (TTM) basis, as compared to the industry median of 1.7x. Considering the aforesaid facts, price movements, valuation and business prospects, we recommend a ‘Hold’ rating on the stock at the current market price of $8.090, up 0.497% on 01 November 2019.

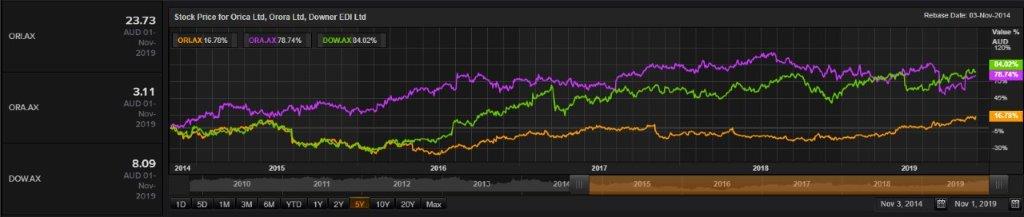

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...