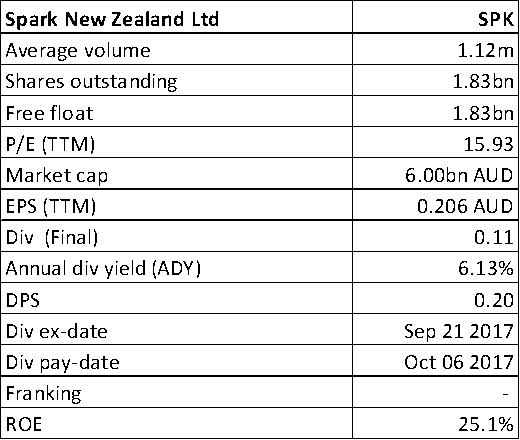

Spark New Zealand Ltd (ASX: SPK)

SPK Details

Positioning itself in a digital ecosystem: The telecommunication player, Spark New Zealand (ASX: SPK) has been gaining attention at the back of the healthy dividend yield scenario with positive outlook of about 6-7% over the next year and onwards while giants like Telstra have slashed the FY18 dividends. The recent snapping of all shares in Digital Island, a NZ-based business telecommunications provider, by Spark New Zealand is also considered to be a positive for the group going forward as Spark now aims to run Digital Island as a standalone business with it operationally reporting into the Spark Ventures & Wholesale unit. SPK has otherwise supplied a range of wholesale services to Digital Island for over 10 years.

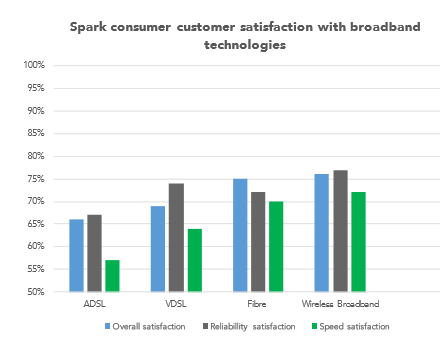

Customer Satisfaction with Broadband (Source: Company Reports)

Overall, the group finds support from the growth in mobile (6% revenue growth in FY17) and wireless broadband (increase in broadband customer base to 84,000) with management’s vision on making SPK the lowest-cost operator in the market. The group, however, sees more potential in wireless than the challenged fixed broadband. The group’s underlying fundamentals are also resilient when compared to peers. In the last three months (as at November 20, 2017), the stock has fallen 9.4% owing to challenges in the Telco sector. We give a “Hold” at the current price of $3.29

.png)

SPK Daily Chart (Source: Thomson Reuters)

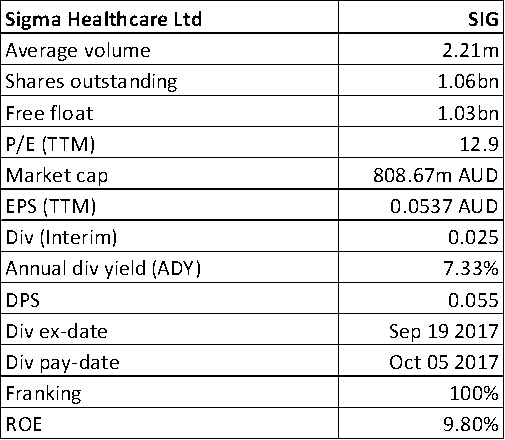

Sigma Healthcare Ltd (ASX: SIG)

SIG Details

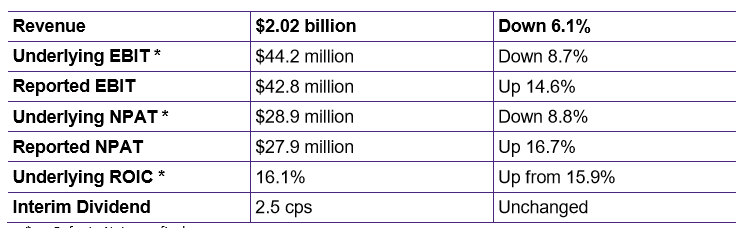

Prevailing headwinds: The pharmaceutical wholesaler, Sigma Healthcare’s (ASX: SIG) dividend outlook also looks to be strong for the next year. While the group has reflected upon initiatives on efficiency gains from project renew and opening of new distribution centre in Queensland, some concerns float with regards to the earnings in next couple of years at the back of challenges including those from the Government’s Pharmaceutical Benefits Scheme (PBS). It would be prudent to see whether the group’s initiatives (such as those in service-offerings) lead to outcomes that can counterbalance the challenges. On related terms, the group had updated the market about Astra Zeneca advising pharmacies and all CSO pharmaceutical wholesalers on their intention to exclusively distribute a proportion of their products direct to Pharmacy effective from 1 November 2017. These products as identified were said to be representing about 1% of SIG’s total sales.

First half 2018 Result (Source: Company Reports)

The group is thus making an effort to minimise the impact on earnings from such changes. On the other hand, SIG maintained the FY18 underlying EBIT guidance of $90 million. SIG is otherwise seen to be benefitting in terms of growth from acquisition including that of MPS business. Given some loopholes, we think that the stock is still “Expensive” at the current price of $0.75, and would review the same at a later date while gauging changes in regulatory environment.

.png)

SIG Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd (ASX: NAB)

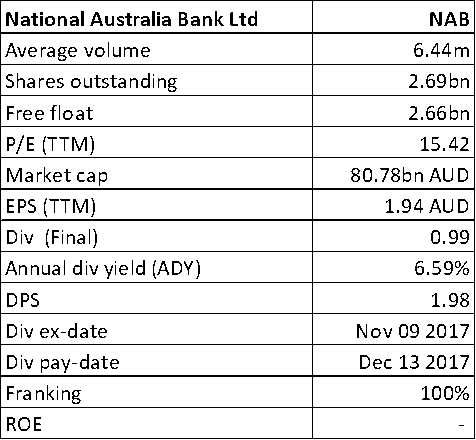

NAB Details

Improving asset quality: While there has been some decline in annual dividends of the majors, National Australia Bank (ASX: NAB), is still seen as a good income stock from a dividend yield expectation of about 7%. The bank has specifically indicated to maintain FY18 dividends at the FY17 level, subject to no material change in the external environment and satisfactory group financial performance. In its recent result for FY17, National Australia Bank’s revenue was up 2.7% with growth in housing and business lending, and stronger Markets & Treasury income. However, bad and doubtful debt (B&DD) charges surged 1.3% to $810 million, but as a percentage of gross loans and acceptances declined 1 bp to 14 bps. On the other hand, asset quality was better with the ratio of 90+ days past due and gross impaired assets to gross loans and acceptances down 15 bps to 0.70% at the back of improving conditions for NZ dairy customers and strategies across the Australian business lending portfolio.

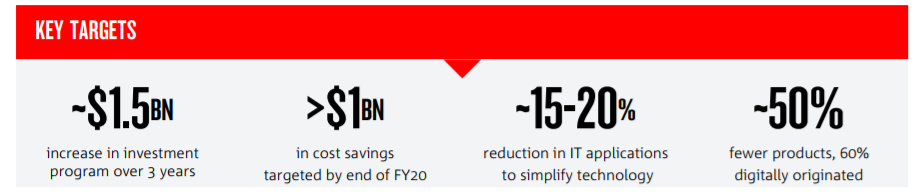

Key Targets (Source: Company Reports)

NAB’s recently introduced strategic initiatives on business simplification are also expected to keep the stream flowing while challenges in banking sector prevail at large. NAB has indicated for cost savings of over $1 billion by end of FY20 at the back of the initiatives and the plan to slash about 4,000 staff. Looking at the current price and some positives factored in the stock performance, we put a “Hold” on the stock at the current price of $30.03

.png)

NAB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...