Stocks’ Details

Mesoblast Limited

Robust Top-line Numbers aided by 73%pcp Growth from TEMCELL HS Inj.®1: Mesoblast Limited (ASX: MSB) is a biotechnology company which specialises in adult stem cell technology. The Company has leveraged its proprietary mesenchymal lineage cell therapy technology platform to establish a broad portfolio of commercial products and late-stage product candidates.

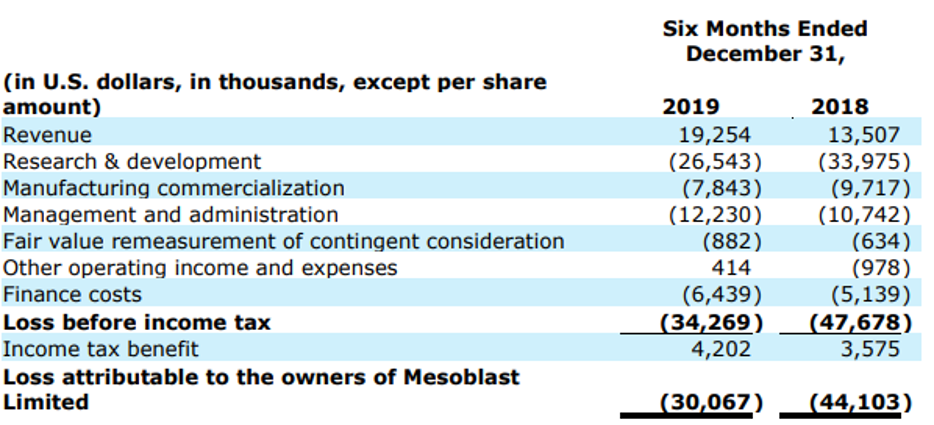

H1FY20 Business Highlights for the Period ended 31st December 2019: MSB declared its half-year results, wherein the company reported revenue of US$19.2 million, up 43% on y-o-y basis. Growth was attributable to 73% pcp growth from sales of TEMCELL HS Inj.®1. The business reported its milestone revenue of US$15.0 million, up 36%, aided by growth from strategic partnerships. MSB posted a lower loss after tax of US$30.1 million, as compare to US$44.1 million. Decline in R&D was attributable to a reduction in third party costs of its Phase 3 clinical trials. The business entered into an agreement with Lonza for the commercial manufacture of RYONCIL. The above collaboration is likely to facilitate inventory build ahead of the planned US market launch and for commercial supply as per the company’s long-term strategy.

Key H1FY20 Income Statement Highlights (Source: Company Reports)

Outlook: For the next twelve months, the business will seek for updates on Priority Review and Prescription Drug User Fee Act (PDUFA) date for RYONCIL for SR-aGVHD in children. In addition, the company will be initiating confirmatory trial of REVASCOR for Advanced and End Stage heart failure.

Stock Recommendation: The stock of MSB is trading at $2.44 with a market capitalisation of ~$1.3 billion. The stock is trading at the upper band of its 52-week trading range of $1.18 to $3.21. The stock has generated robust returns of 72.24% and 92.06% in the last six-months and one year, respectively. The business applied for Priority Review of the BLA for RYONCIL, under the product candidate’s existing Fast Track designation and is expected to launch the product in the US in 2020. Considering the current trading levels and business prospects, we recommend a “Buy” rating on the stock at the current market price of $2.44 per share, up 0.826% on 27th February 2020.

Ramsay Health Care Limited

Robust Growth from Europe Led Improved Business Performance: Ramsay Health Care Limited (ASX: RHC) is a global hospital group, that owns and operates a comprehensive range of healthcare facilities.

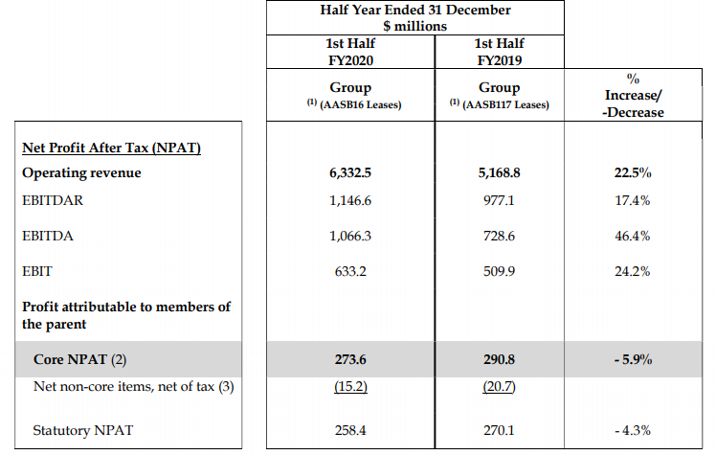

H1FY20 Operational Highlights for the Period ended 31 December 2019: RHC announced its six-months results, wherein the company reported revenue of $6.3 billion, up 22.5% on pcp terms. During the period, the company witnessed growth across its UK, Continental Europe and Asia segments, which was partially offset by challenging conditions in Australia. EBITDAR came in at $1.1 billion, up 17.4% from H1FY19. The company’s UK business recorded its best half yearly performance in recent years, driven by growth in overall business activities. Revenue from its UK business stood at £267.6 million, up 8.7% on pcp. Australia reported a revenue of $2.7 billion, depicting an increase of 3.9% on y-o-y basis.

Key H1FY20 Financial Highlights (Source: Company Reports)

The Board of Directors announced a fully franked dividend of $2.042700 per security with a payment date of 20th April 2020.

Outlook: The business expects growth in terms of volume and tariff in the UK and Europe segment and expects a softer growth environment in Australia. The business expects its FY20 Core EPS growth on a like-for-like basis in the range of 2% to 4%, which corresponds to a negative Core EPS of -6% to -4% under the new lease accounting standard AASB16. The business expects EBITDAR growth of 8% to 10%, that will remain unaffected by the new lease standard.

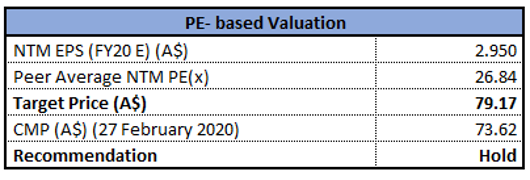

Valuation Methodology: Price to Earnings Based Valuation

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of RHC is trading at $73.62 with a market capitalisation of ~$15.11 billion. The stock is trading at the upper band of its 52-week trading range of $60 - $80.93. The stock has generated decent returns of 10.80% and 23.77% in the last six-months and one year, respectively. The company has a strong balance sheet, which will help in funding the pipeline of brownfield capacity expansion and future acquisitions. Considering the current trading levels and business prospects, we have valued the stock using Price to Earnings based relative valuation method. For the purpose, we have taken peers like CSL Ltd (ASX: CSL), Cochlear Ltd (ASX: COH), Sonic Healthcare Ltd (ASX: SHL), and arrived at a target price of higher single-digit upside (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $73.62 per share, down 1.538% on 27th February 2020.

Australian Pharmaceutical Industries Limited

Reported Robust Bottom-line Growth along with Improved Market-share: Australian Pharmaceutical Industries Limited (ASX: API) operates as awholesale distributor of pharmaceutical and allied products. The company also provides retail support services to pharmacists. Recently, the company informed that one of its directors, named Richard Craig Vincent, has acquired 495,711 performance rights under the Long Term Incentive Plan 2019 - 2022.

FY19 Financial Highlights for the Period ended 31st August 2019:API declared its full year results, wherein the company reported revenue amounting to $4 billion, up 4.1% on y-o-y basis. The company delivered robust bottom-line growth with NPAT amounting to $56.6 million, up 17.4% on y-o-y basis. During the period, the company’s growth assets continued to perform well while Priceline like-for-like sales grew 0.7%. The year was marked by growth in market share and contribution from Priceline pharmacy, consumer brands and Clear Skincare businesses, followed by a solid result from the pharmaceutical wholesaling business.

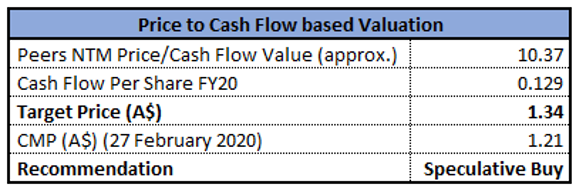

Valuation Methodology: Price to Cash Flow Based Valuation

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of API is quoting at $1.205 with a market capitalisation of ~$591.19m. The stock is trading at the lower band of its 52-week trading range of $1.2 to $1.57. The stock has generated negative returns of 8.05% and 11.76% in the last three months and six-months, respectively. The company intends to deliver high quality, affordable and innovative products to its broad customer base and focuses on new product development which will further lead to high volume generic products introduced into the market. Considering the current trading levels and business prospects, we have valued the stock using Price to Cash Flow based relative valuation method. For the purpose, we have taken peers like Ansell Ltd (ASX: ANN), Healius Ltd (ASX: HLS) and Sonic Healthcare Ltd (ASX: SHL) and arrived at a target price of lower-double digit upside (in % terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $1.205 per share, up 0.417% on 27th February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...