Stocks’ Details

CSL Limited

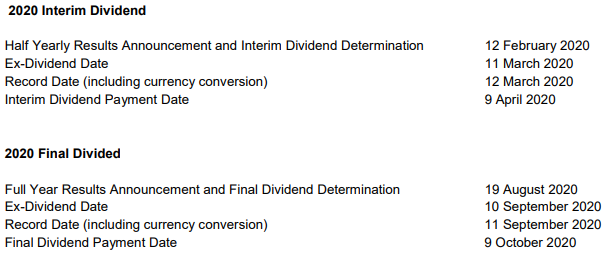

FY20 Interim and Final dividend Dates Proposed:CSL Limited (ASX: CSL) is involved in developing and delivering innovative medicines. Recently, the company issued new 4,818 fully paid ordinary shares, comprising 3,661 shares issued under performance rights plan (PRP) 2015; 1,137 shares under PRP at nil price; and 20 shares under global employee share plan (GESP) at an issue price of $162.76 each. In another update, the company notified about the proposed dates for dividend payments and AGM for FY20. The 2020 Annual General Meeting of CSL Limited is to be held in Melbourne on October 14, 2020.

Proposed FY20 Dividend Dates (Source: Company Reports)

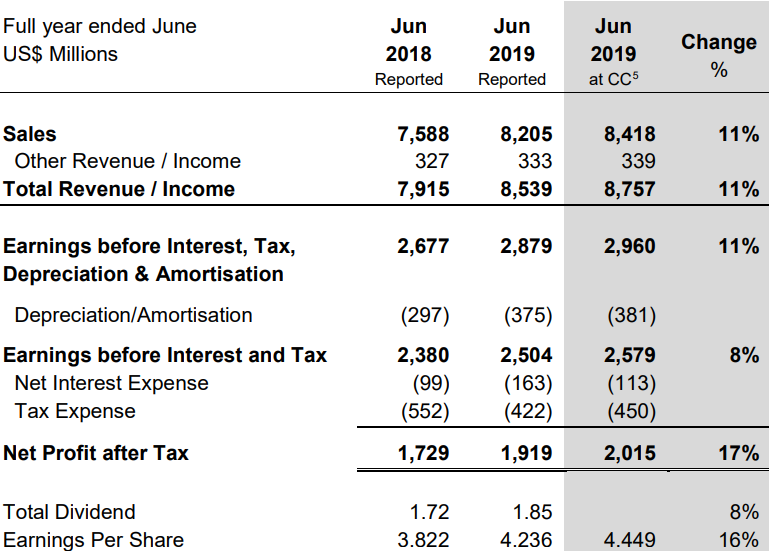

FY19 Key Highlights for the year ended June 30, 2019:Net profit after tax for the period was reported at US$1,919 Mn, which is an increase of 17% (at Constant Currency). Total revenue/income for the period was reported at US$8,539 Mn, which is an increase of 11% (at CC). This result can be attributed to high demand for specialty products such as Haegarda & Kcentra; continued strong growth in albumin and immunoglobulin therapies; strong profit growth in Seqirus; and successful evolution of the haemophilia therapies portfolio. The Board of Directors declared a final dividend of US$1 per share, with record date and payment dates on September 11, 2019 and October 11, 2019, respectively.

FY19 Income Statement (Source: Company Reports)

What to Expect:As per the release, FY20 net profit after tax has been anticipated to be in the range of around US$2,050 Mn to US$2,110 Mn (at Constant Currency), representing growth in the range of 7% - 10%, whichconsiders the one-off financial headwind of transitioning to a new model of direct distribution in China.

Stock Recommendation:CSL’s share generated positive YTD return of 31.91%. Its gross margin for FY19 stood at 56%, higher than the margin of 55.4% in FY18 but lower than the industry median of 71.4%.Net margin for FY19 stood at 22.5%, better than the FY18 result of 21.8%. ROE for FY19 stood at 41.1%, better than the industry median but lower than the FY18 result of 47.7%. Currently, the stock is trading close to its 52-week high level of $248.050.Hence, considering the aforesaid facts and current trading levels, we have a wait and watch stance on the stock at the current market price of $243.740, down 0.327% on October 14, 2019, ahead of the company’s AGM, to be held on 14 October 2019.

Fisher & Paykel Healthcare Corporation Limited

F&P ViteraTMnow now available for sale in the United States:Fisher & Paykel Healthcare Corporation Limited (ASX: FPH) is a leading designer, manufacturer and marketer of products and systems for use in respiratory case, acute care, surgery and the treatment of obstructive sleep apnea. Recently, the company announced that its F&P ViteraTMis now available for sale in the United States. F&P Viterais a new mask for obstructive sleep apnea (OSA), and is already available in markets such as Canada, Australia, Europe and New Zealandand is expected to be available in other markets as well after the relevant regulatory clearances.

FY19 Key Highlights for the year ended March 31, 2019:Operating revenue for the period increased by 9% to NZ$1.07 Bn. Hospital revenue grew by 12% to NZ$642 Mn, as there was strong demand for Optiflow and AIRVO systems, driven by a growing body of clinical research in nasal high flow therapy. Revenue in the Homecare group increased by 6% to NZ$421 Mn, driven by growth in the company’s home respiratory support business and successful rollout of new SleepStyle system for patients with OSA.

Net profit after tax increased by 10% to NZ$209 Mn. The total dividend for the financial year was reported at 22.35 cents per share (NZD), which is an increase of 9% on previous year.

FY2019 Revenue by Product Group (Source: Company Reports)

What to expect:Following receipt of regulatory clearance to sell F&P ViteraTM mask in the United States, the company has upgraded its revenue and earnings guidance for the financial year ended March 31, 2020. Previously, after consideration of NZ:US exchange rate of 64 cents, FY20 Operating revenue was estimated to be around NZ$1.17 Bn and net profit after tax was estimated to be in the range of NZ$245 Mn - NZ$255 Mn.

Now, after consideration of NZD-USD exchange rate at 63 cents for the balance of the year, the full year operating revenue is expected to be around NZ$1.19 Bn and net profit after tax is anticipated to be in the range of around NZ$255 Mn - NZ$265 Mn.

Stock Recommendation:FPH’s share generated a positive YTD return of 31.79%. Currently, the stock is trading close to its 52-week high level of $17.120. The company has revised its operating revenue and NPAT for FY20. Its gross margin for FY19 stood at 66.9%, lower than the industry median of 70.8%. However, its EBITDA margin and net margin for FY19 stood at 33.4% and 19.5%, better than the industry median of 27.2% and 16.7%, respectively.Its ROE for FY19 stood at 25.0%, better than the industry median of 10.6%. Its current ratio for FY19 stood in-line to the industry median of 2.47x. Debt to equity multiple for FY19 stood at 0.09x, lower than the industry median of 0.32x.Hence, considering the aforesaid facts and current trading levels, we have a wait and watch stance on the stock at the current market price of $17.080, up 7.018% on October 14, 2019, on account of upgradation in operating revenue and profit guidance.

Alcidion Group Limited

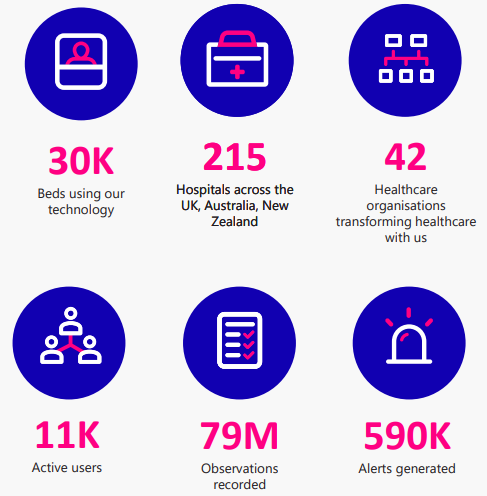

Q1FY20 Revenue Increased By 16% on PCP:Alcidion Group Limited (ASX: ALC) is primarily engaged in the development and licensing of its own healthcare software products (Miya, Patientrack and Smartpage).

On October 14, 2019, the company published its Q1FY20 report, where it highlighted that its revenue for the period was reported at $12.9 Mn, representing a 16% increase on previous corresponding period.Non-recurring revenue booked for FY20 stands at $5.6 Mn and recurring revenue to be recognised in FY20 currently stands at $7.3 Mn.

The period was marked by strategically important three-year contract signed with Healthscope to provide a solution supporting its data and analytics strategy across 43 hospitals, representing the first implementation of company’s data analytics capabilities into a major private healthcare group. The company signed several new and recurring contracts, with a total contract value of $2.54 Mn, expecting to generate a total of $1.24 Mn of this solid revenue in FY20. Cash surplus from operations for the period stood at $136 K, representing the third consecutive quarter of positive net cashflow; and improved cash reserves of $4.4 Mn.

ALC’s Important Key Metrics (Source: Company Reports)

What to Expect:As per the release, the company continues to expand its sold revenue pipeline for FY20 and the next five years. Total sold revenue out to FY25 is expected to be $34.0 Mn.

Stock Recommendation:ALC’s share generated a whopping YTD return of 485.11%. FY19 was a year of decent performance with cash surplus from operations, stronger sold revenue pipeline, and its first entry into private healthcare for data and analytics. Its gross margin in FY19 stood at 35.1%, higher than the FY18 result of 33.6%. Considering the series of events in FY19, including the launch of new brands and signing of new contracts & agreements, we would like to see the progress and impact of the above developments in future performance.Currently, the stock is trading close to its 52-week high level of $0.305.Considering the above stated factors, we have a wait and watch stance on the stock at the current market price of $0.245, down 10.909% on October 14, 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...