.png)

Stocks’ Details

CSL Limited

Trading at Higher Valuations: With synergies through acquisitions in FY18, CSL Limited (ASX: CSL)has been strengthening its position in the industry. For the purposes, CSL eyed to companies-

(a) Ruide Acquisition: CSL acquired 80% of the equity of Ruide.

(b) Calimmune Acquisition:CSL acquired 100% equity of Calimmune for an upfront payment of $82 million.

(c) Guangzhou Junxin Pharma Acquisition:100% equity was acquired by CSL. The acquired entity is a GSP licence holder which enables it to own and sell inventory in the domestic Chinese market.

Financial Performance in 1H FY19:CSL recorded a good set of numbers in 1H FY19 on account of standout performance from its Immunoglobulin, Specialty Products and Influenza Vaccines franchises. EBIT Margin has slightly come down to 34.5% in 1H FY19 vs 35.6%, pcp.

.png)

Group Results (Source: Company Reports)

What to Expect: The management aims to open 30-35 new collection centres in FY19. Seqirus business is likely to see losses in 2H FY19 due to seasonality effect. PAT for FY19 is likely in the range of ~ $1,880 to $1,950 million at constant currency with an upward bias.

Stock Recommendation: Looking at the valuation, the stock is trading at price to book value of 12.5x which is significantly higher than the industry median of 3.3x, showing overvalued at the current juncture. At CMP of $190.51, the stock is trading at P/E multiple of 33.30x which is higher than its peers - ResMed Inc of 30.79x and Ramsay Health Care Limited of 31.25x. At the current level, the annual dividend yield for the stock comes in at 1.30% with market capitalisation at ~$87.46 billion.In the past 1 year, the stock witnessed a rise of 18.95% and is trading slightly towards the 52-week higher level of $232.69. Considering the aforesaid facts and current trading level, we, therefore, maintain our “Expensive” recommendation on the stock at the current market price of $190.510 per share (down 1.305% on 18 April 2019).

ResMed Inc

Valuations Seem Comfortable:ResMed Inc (ASX: RMD) engaged in the business of medical devices intimated the ASX to announce its 3Q FY19 earnings on May 2, 2019.

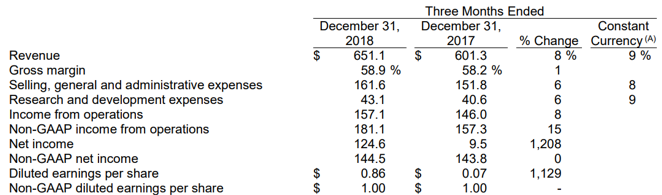

Financial Performance in 2Q FY19: Thecompany recorded a strong set of results in the second quarter of FY19. U.S., Canada and Latin America performed well with 9% revenue growth (excluding Software Services).Revenue for the period increased 8% to $651.1 million with Gross Margin expanding 70bps to 58.9%. Net operating profit came in at $157.1 million recording a growth of 8%. Non-GAAP operating profit shown a growth of 15% to $181.1 million.

Financial Results and Operating Metrics (Source: Company Reports)

At CMP of $13.600, the stock is trading at price to earnings multiple of 30.79x with the market capitalization of $20.3 billion. Annual dividend yield stands at 1.03%.The stock is trading at price to book value of 0.7x which is well-below 3.4x of Healthcare Equipment & Supplies’ Industry Median. The 52-week high and low range of the stock is at $16.570-$12.510 with the stock trading below the average of this range. Considering the above-mentioned factors, we retain our “Buy” recommendation on the stock at the current market price of $13.600 per share (down 4.023% on 18 April 2019).

Cochlear Limited

Valuations at Higher End:Cochlear Limited (ASX: COH) announced that it launched Nucleus® Profile™ Plus Series cochlear implant, designed for routine 1.5 and 3 Tesla magnetic resonance imaging scans without requiring to remove the internal magnet. Commercial availability starts in Germany with other European countries to follow over the coming months. The Nucleus Profile Plus series implant is anticipated to be launched across other developed markets over the coming months, subject to the timing of regulatory approvals.

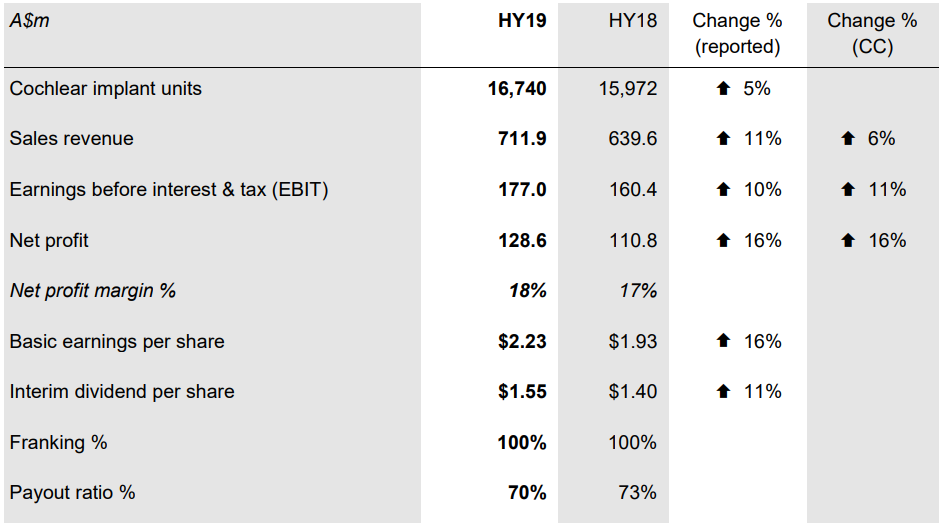

Financial Performance in 1H FY19:The services business did well, and revenues grew by 28%. The company saw a growth of 11% to $711.9 million in the sales revenue and net profit grew 16% to $128.6 million for 1H FY19.

Cochlear implant units stood at 16,740 and were up 5%. Reported PAT of $128.6 million also witnessed strong growth of 16%. Strong cash flow generation supported the growth in interim dividend at 11%.

1HFY19 Key Highlights (Source: Company Reports)

What to Expect: The management expects FY19 net profit in the range of $265-275 million, 8-12% higher as compared to FY18. Over the next few years, the company has a number of large long-term investment projects which includes the development of China manufacturing facility, with the construction phase expected to be complete by FY20 end, and investments in IT platforms to strengthen its connected health, digital and cyber security capabilities.

Stock Recommendation:At CMP of $175.750, the stock is trading at price to earnings of 38.40x which is quite higher than its peer median of 30.79x, suggesting the stock is expensive at the current level.

Looking at the price to book multiple, the stock is trading at 15.52x of its book which is significantly higher than 2.28x of industry median, signalling valuations on the higher side. However, the stock has gained 6.45% in the last 5-days trading period. Considering the above parameters, the stock seems overvalued. Hence, we retain our “Expensive” rating on the stock at the current market price of A$175.750 per share (down 2.089% on 18 April 2019).

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...