Ramsay Health Care Limited

RHC Proposes Dividend/Distribution To Its Shareholders: Ramsay Health Care Limited (ASX: RHC) operates ~235 hospitals, day surgery centres, treatment facilities, rehabilitation & psychiatric units & a nursing college across seven countries. The company recently announced fully franked dividend/distribution of AUD 2.2931 per share on the security type ‘RHCPA - TRANS PREF 6-BBSW+ 4.85% PERP SUB RED T-10-10’ for the period of six months, with payment date on October 21, 2019, record date on October 3, 2019, and ex-date on October 2, 2019.

In another update, it announced that its French subsidiary, Ramsay Générale de Santé (RGdS), had launched a EUR 625 Mn renounceable rights issue as part of its previously disclosed intention to refinance its purchase of Capio AB. The subscription period for RGdS rights issue completed on 5 April 2019 and the total subscription orders made under RGdS rights issue stood at EUR 566,760,513.70 which represents total subscription rate of 90.66% corresponding to the issue of 34,432,595 new shares.

Financials: Group’s revenue increased by 14.9% pcp to $5.1 Bn in H1FY19. Its EBITDA increased by 9.8% pcp to $728.6 Mn in H1FY19. Its core NPAT increased by 1% pcp to $290.8 Mn.

.png)

Projects forecast for completion in FY19 in Australia (Source: Company Reports)

What To Expect: The company aims to focus on achieving synergies related to the Capio transaction, integrating the business with RGdS, and divesting non-strategic assets.There are positive signs in the UK market in terms of both price and volume growth. The core EPS growth for FY19 has been reaffirmed up to 2% including Capio.

Stock Recommendation: Ramsay’s share generated positive YTD return of 10.98%. It is currently trading close to its 52 weeks high price. Its gross margin for H1FY19 stood at 73.9% better than the industry median of 48.9%, implying that the company is well positioned to address its operating expenses than its peer group. Its net margin for H1FY19 stood in-line with the industry median at 5.3%, implying a decent bottom-line performance as per industry standards.

Its ROE for the same period stood at 11.2% better than the industry median of 8.2%, which implies that the company generated better value to its equity-holders than its peer group.Hence, considering the aforesaid facts and current trading level, we maintain our “Hold” rating on the stock at the current market price of $65.320 (up 1.903% on April 30, 2019).

Cochlear Limited

COH Launched Nucleus® ProfileTM Plus Series Implant: Cochlear Limited (ASX: COH) has major operations in Cochlear implants, Services (sound processor upgrades and other), and Acoustics (bone conduction and acoustic implants). The company recently announced the launch of the Nucleus® ProfileTM Plus Series implant designed for routine 1.5 and 3 Tesla magnetic resonance imaging scans without the need to remove the internal magnet. It is expected to be launched across other developed markets over the coming months, subject to the timing of regulatory approvals.

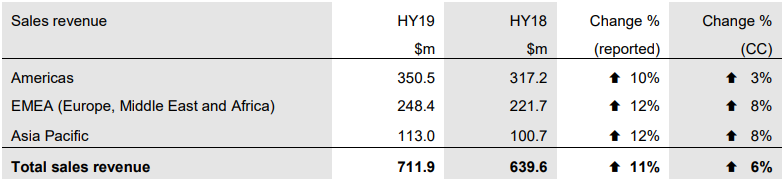

Financials: The sales revenue increased by 11% pcp to $711.9 Mn in H1FY19. It was driven by an increase in revenue by 28% pcp in Services, 7% pcp increase in Acoustics, and 5% pcp increase in Cochlear implants.

Regional Revenue Data (Source: Company Reports)

What To Expect: Revenue growth is expected to be driven by the Services business, with strong uptake of the Nucleus 7 Sound Processor, particularly in the first half. Lower rate of cochlear implant growth is expected across the developed markets for FY19. Emerging market growth rates over time continue to be strong, however, annual growth rates can be variable, driven by the timing of tender based activity and macro-economic conditions. Continued investment to retain market leadership and drive long-term market growth with the target of maintaining the net profit margin.

Stock Recommendation: Cochlear’s share generated positive YTD return of 4.63%. Its EBITDA margin for H1FY19 stood at 27.6% which is marginally lower than the industry median of 27.9%.

Hence, considering the aforesaid facts and current trading level, we suggest investors to have a close watch on the stock at the current market price of $187.33 (up 2.366% on April 30, 2019).

CSL Limited

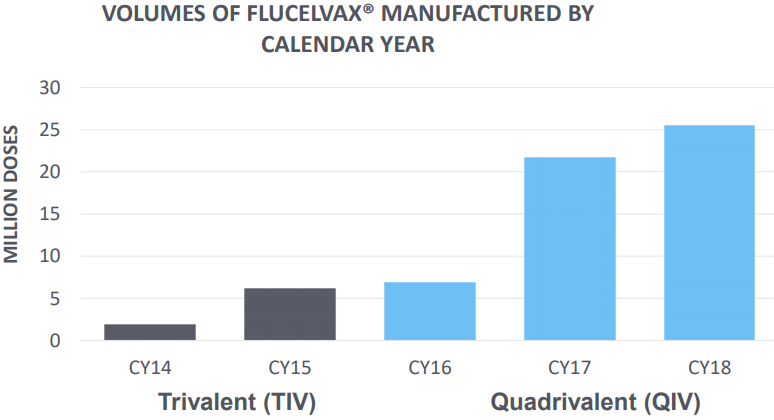

R&D Investments To Counter Influenza Threats: CSL Limited (ASX: CSL) has an engagement in the research, development, manufacture, marketing, and distribution of biopharmaceutical and allied products. The company recently published Seqirus presentation at 2019 Macquarie Equities Conference, where it highlighted that influenza poses a constant pandemic threat. Additionally, the company has been manufacturing and heavily investing in R&D capabilities across three continents. Its differentiated influenza vaccines are based on egg and cell based manufacturing and novel adjuvant technology. Coming to the revenues of Seqirus business, the contribution in H1FY19 as per regions were as follows:

-

North America contributed 71%,

-

-

Europe made up 14%,

-

-

Asia PAC made up 10%,

-

-

ROW contributed 5%.

-

Financials: The group’s Revenue from continuing operations increased by 8.6% pcp to US$4.5 Bn in 1HFY19. Its net profit after tax attributable to members increased by 6.8% to US$1.2 Bn.

Cell Based Manufacturing Data (Source: Company Reports)

What To Expect: The company anticipates strong demand for CSL’s plasma and recombinant products. It expects to outpace the market in growing plasma collections.It plans to open between 30 and 35 new collection centres this financial year. Seqirus business is expected to post a loss in the second half of the fiscal year. Its net profit after tax for FY19 is expected to be in the range between $1,880 to $1,950 Mn at constant currency.

Stock Recommendation: CSL Limited’s share generated positive YTD return of 6.88%. Its EBITDA margin and net margin for H1FY19 stood at 39.5% and 25.7% lower than the previous corresponding period (H1FY19) at 41.7% and 26.2%, respectively. Currently, the stock is trading at a high trailing 12-months P/E of 34.63x as compared to the Pharmaceutical industry trailing 12-months P/E of 6.5x showing that the stock is extremely overvalued.

Hence, considering the aforesaid facts and current trading level, we have a ‘wait and watch’ stance on the stock at the current market price of $198.57 per share (up 0.217% on April 30, 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...