The Citadel Group

Strong Growth Outlook: The Citadel Group Limited (ASX: CGL) had an eventful FY18 as the IT security and data management company recorded healthy numbers and the upbeat forecast. The company has a strong portfolio of Government clients with the new ones in Victoria, Queensland, and New South Wales and supports more than 24,000 new Citadel-IX users. The company won 10 new long-term contracts for Citadel- IX. Higher revenue was driven by the client wins across the portfolio of solutions along with the rollout of multi-year Australian Federal Government Agency Contract. Throughout the FY2018, the company expanded its customer base with notable mentions such as RAAF in New South Wales, Melbourne City Council, Royal Adelaide Hospital, Department of Defense among others. On financial front, the company has consistently posted higher operating margins over 5 years with the latest coming in at 23.9% compared to the industry average of 19.2%. Apart from effective cost management, it has also generated higher returns for the shareholders consistently with ROE marked at 20.5% for FY18 against the industry return of 12.0%.

.png)

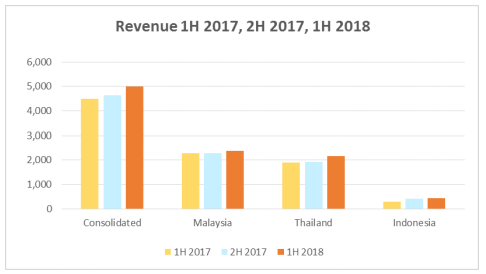

Revenue Growth (Source: Company Reports)

Meanwhile, the stock has reflected the positive developments happening around, generating a YTD return of 25.44%. CGL shares have been in a secular uptrend and current developments clubbed with the outlook of the company are expected to drive the growth further. We, therefore, recommend a ‘Buy’ in the stock at the current market price of $7.850.

iCAR Asia

Core Business remains strong: iCAR Asia Limited (ASX: ICQ) posted strong 1H FY2018 results driven by the growth in all the markets. The company posted a profit of $5,008,342, up 12% from $4,482,592 in FY17. The major revenue contributing segment i.e. User Car Sales remained strong posting a growth of 35% in FY18 compared to previous corresponding period. Besides this, the second quarter of the half year saw record quarterly cash collections at A$3.21Mn, an increase of 29% over the previous corresponding period. This is the company’s highest ever quarterly cash receipts.As at June 30, the company had cash at bank of $15.2 Mn.The company has a positive outlook for the third quarter expecting record revenue growth in the quarter and 50% more than the previous comparable period. Main drivers of the growth would be retimed new car revenues in Q3 and progress in the Used Car business.

Revenue Contribution by Geography (Source: Company Reports)

Meanwhile, the stock has generated YTD return of 12.50% and has been trading in a tight consolidation range from quite some time now. We expect that Narrowing EBITDA losses and increasing audience across the Geography would ramp up the growth further, going forward. Moreover, the efforts made by the company to cut down on operating expenses and manage cost effectively would reflect in the numbers and in stock price. We, therefore, recommend ‘Speculative Buy’ in the stock at the current market price of $0.225.

Auscann Group Holdings

Cannabinoid Meds to drive growth: Auscann Group Holdings Limited (ASX: AC8) has been trading in green since the company was listed on OTCQX market under the scrip code ACNNF. The company posted lower losses in FY18 at $7,569,001, down more than 45% compared to $14,207,117 Mn posted in FY2017. Losses were recorded primarily due to a share-based payment of $2.7 Mn for advisor share options issued during the period. Increase in the R&D expense was due to product launch due in Australia in FY19. On the other hand, the company has entered into various strategic partnerships in Australia, Canada, and Chile and is progressing towards becoming a fully-integrated Cannabinoid pharmaceutical company. The company has been progressing on all fronts including new agreements, R&D breakthroughs, and regulatory approval. The Cannabinoid medicines could be an improvement over the opioid-based medicines prescribed to the patients suffering from Chronic neuropathic pain. A key challenge for the company would be to convince the doctors and medical fraternity to switch to cannabinoid. The company has enough liquidity with current ratio at 23.17x compared to the Industry average of 2.47x.

.png)

Integrated Business Model (Source: Company Reports)

The stock has rewarded the shareholders generating year to date return of 27.95%. Going ahead, the recent capital raise of AUD$35 Mn keeps the company well-funded to take ahead its R&D program and cover operational cost. Also, listing on the OTCQX would diversify the investor platform of the company and give a stronger foothold in North America where the company has numerous strategic agreements. We, therefore, recommend ‘Hold’ on the stock at the current market price of $1.060 (up 2.9% on September 14, 2018).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...