.png)

Stocks’ Details

Suncorp Group Limited

Special Dividend to be Paid on May 03, 2019: Suncorp Group Limited (ASX: SUN) recently announced a special dividend of 8.0 cents per share which will be paid on Friday, May 3, 2019to shareholders who registered on or before 2 April 2019. The Ex-date for the same is April 01, 2019. The Board announced this after the successful completion of the sale of its Australian Life Business to TAL Dai-ichi Life Australia Pty Ltd.

.png)

Consolidated Income Statement (Source: Company Reports)

The Group has delivered a net profit after tax attributable to owners of the company of $250 million for the half-year ended 31 December 2018 as compared to $452 million in the prior corresponding period.

During the half year, the Group issued $600 million of subordinated debt through the Company as part of its capital management strategy, which was fully deployed to the Bank as Basel III compliant Tier 2 capital.The issuance facilitated the redemption of the Company’s existing $770 million of subordinated debt, of which $670 million and $100 million had been deployed as qualifying Tier 2 capital to the Bank and Life businesses respectively. Following the $600 million Tier 2 issuance and $770 million Tier 2 redemption, the Group now has a more optimal level of Tier 2 capital.

Key Priorities: The company is primarily concerned to achieve its vision of three strategic priorities i.e. to elevate the customer, to inspire the people and drive momentum and growth.

The stock, on the other hand, has generated a YTD return of 8.56%, with a P/B multiple of 1.3x compared to an insurance industry median of 2.4x, hinting a potential for the stock for an up-move. Therefore, considering the above factors, we recommend a “Hold” rating on the stock at CMP of $13.440 per share (up 1.895% on 22 March 2019).

Magellan Financial Group Limited

Trading closer to 52-week high: Magellan Financial Group Limited (ASX: MFG) recently announced that Ms. Marcia Venegas had been appointed to the role of Company Secretary of the company effective from 20 March 2019. Ms. Venegas has also been nominated to communicate with the ASX relating to Listing Rule matters. Mr. Geoffrey Stirton has resigned as Company Secretary with immediate effect as well.

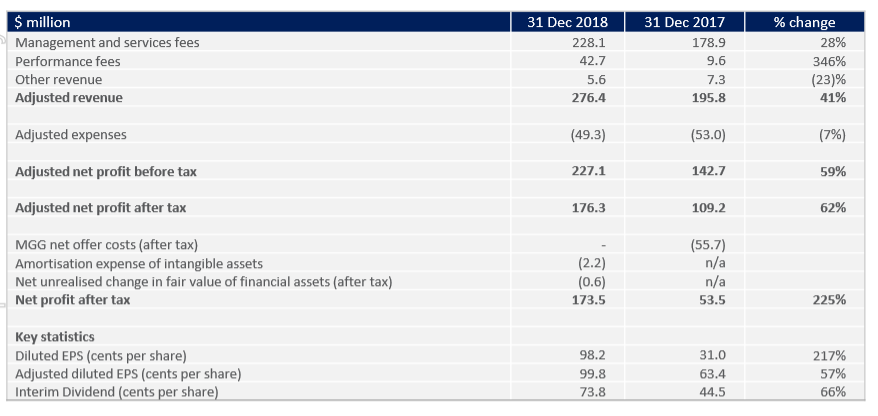

1HFY19 Financial Results (Source: Company Reports)

The revenues for the six months ended 31 December 2018 increased by 45% to $273.2 million. This was driven by a 28% increase in total management fees revenue as a result of a 35% increase in average FUM attributable to strong investment performance, net inflows and the acquisition of Airlie in March 2018. The Group reported a net profit after tax of $173.5 million in 1HFY19 which represents an increase of 225% over the previous corresponding period.

Among the key ratios, the pre-tax ROA and ROE stood at 32.8% and 27.1% in 1HFY19, a increase of 19.8% and 15.0% respectively as compared to the prior corresponding period.

Expenses likely to take-off: Going forward, the total Group expenses (excluding non-cash amortisation and Magellan Global Trust Unit Purchase Plan) are anticipated to around $105 million in FY19 as compared to total group expenses (excluding Magellan Global Trust net offer costs and non-cash amortisation) of $101 million in 2018.

The stock is currently trading closer to its 52-week high price and, thus, we can say that the stock’s current price has discounted all the key growth catalysts. As a result, we suggest to the investor that they can book the profit at the current level as it is trading at a higher level. Hence, we put a “Sell” recommendation on the stock at the current market price of 35.95 per share and advice market players to wait for a further correction to get better entry levels.

Perpetual Limited

Understating Key Financial Metrics: Perpetual Limited (ASX: PPT) has recently announced that Perpetual Limited and its related bodies corporate, a substantial holder of Rural Co Holdings Limited has cut down its voting power from the erstwhile 9.51% to the current 8.40%.

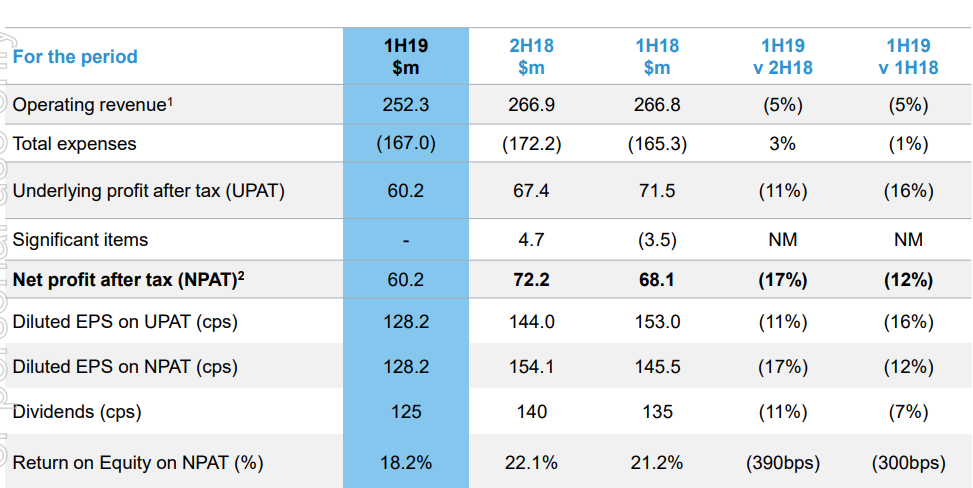

Group Financial Performance (Source: Company Reports)

The operating revenue for Perpetual took a dip of ~5.0% to $252.3 million in 1HFY19 as compared to its previous corresponding period primarily on the back of PI net outflows and lower performance fees and unrealized gains/losses on FVTPL assets now reported through the income statement.For the half-year ended 31 December 2018, the company reported a net profit after tax attributable to equity holders of Perpetual Limited of $60.2 million compared to the net profit after tax attributable to equity holders of Perpetual Limited for the half-year ended 31 December 2017 of $68.1 million.

Among the key ratios, the ROE and Asset Turnover stood at 9.1% and 0.21x in 1HFY19 a decrease of 1.5% and 10.0%, respectively over the previous corresponding period.

What to Expect from PPT: The company is seeking for diversification to accelerate growth while embracing new asset classes & investment styles. It will promote a boutique culture within each investment team and leverage its “institutional grade” infrastructure and distribution platform.

The stock generated a YTD of 28.78%, however, it is currently trading at a P/B multiple of around 2.8x compared to the industry median of ~1.3x (Investment banking & investment services). Also, the P/E multiple is currently 14.02x which is greater than an industry median of ~12.0x.

With sluggish financial performance against the prior corresponding period and the price multiples trading higher than the industry, the stock seems to be expensive at the current juncture. Hence, we reiterate our “Expensive” recommendation on the stock at the current market price of $40.27 (up 1.105% on 22 March 2019).

.PNG)

Stock Price Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...