Stocks’ Details

Insurance Australia Group Limited

Update on Catastrophic Reinsurance Plan for CY20 & Peril Claim Costs: Insurance Australia Group Limited (ASX: IAG) is engaged in providing general insurance services, which includes a wide range of personal and commercial insurance products. On 21st January 2020, the company announced that Ben Bessell, Group Executive of the company has planned to step down from the post, effective from March end 2020.

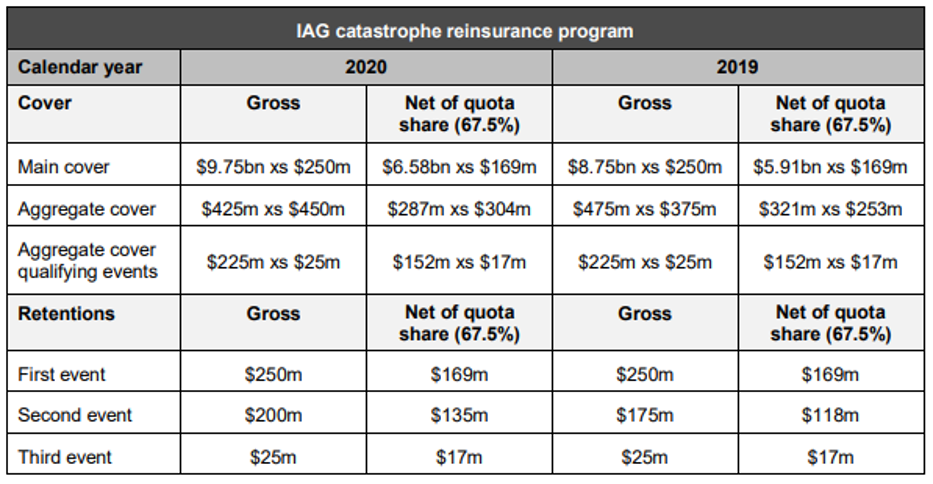

Highlights ofCatastrophic Reinsurance Program: On 3rd January 2020, the company has increased its group reinsurance cover to up to $10 billion, up from $9 billion in the previous calendar year. The company also stated an update on claim costs associated with net natural perils for FY20 to date. IAG had obtained more than 2,800 bushfire related claims since September 2019. Most of these claims were linked to residential properties. The group is anticipating natural peril claim costs of approximately $400 for the six months ended December 31, 2019. It was mentioned that bushfires would result in net claims costs of about $160 million during the half.

IAG Catastrophe Reinsurance Protection (Source: Company Reports)

Other Recent Updates: Recently, the company announced that Peter Horton has been appointed as the Company Secretary, effective December 19, 2019. The company also notified that H1 FY20 results will be announced on 12th February 2020.

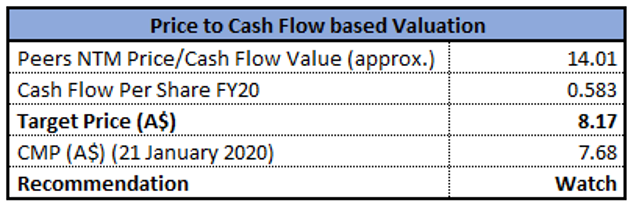

Valuation Methodology: Price to Cash Flow Multiple Approach

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to the average of its 52-week low and high of $7.040 and $8.740, respectively. The stock gave a return of 6.19% in the past one year. As per ASX, the stock has a market cap of $17.84 billion with a PE multiple of 16.69x and an annual dividend yield of 4.15%, suggesting a decent opportunity for accumulation. The company’s asset to equity stood at 4.57x, lower than the industry median of 5.89x, reflecting a better financial position. We have valued the stock using P/CF based relative valuation method, and for the said purpose, we have considered peers like NIB Holdings Ltd (ASX: NHF), QBE Insurance Group Ltd (ASX: QBE) and Suncorp Group Ltd (ASX: SUN), to name few. Therefore, we have arrived at a target price with an upside of single-digit (in percentage terms). Considering the above factors, we have a watch view on the stock at the current market price of $7.680 per share,down 0.518% on 21st January 2020.

AMCIL Limited

Profit up by ~4.4% in 1HFY20: AMCIL Limited (ASX: AMH) is engaged in managing a strong investment portfolio consisting of 30 to 40 stocks. The portfolio comprises both small and large companies in the Australian equity market. The market capitalisation of the company stood at $277.13 million as on 21st January 2020.

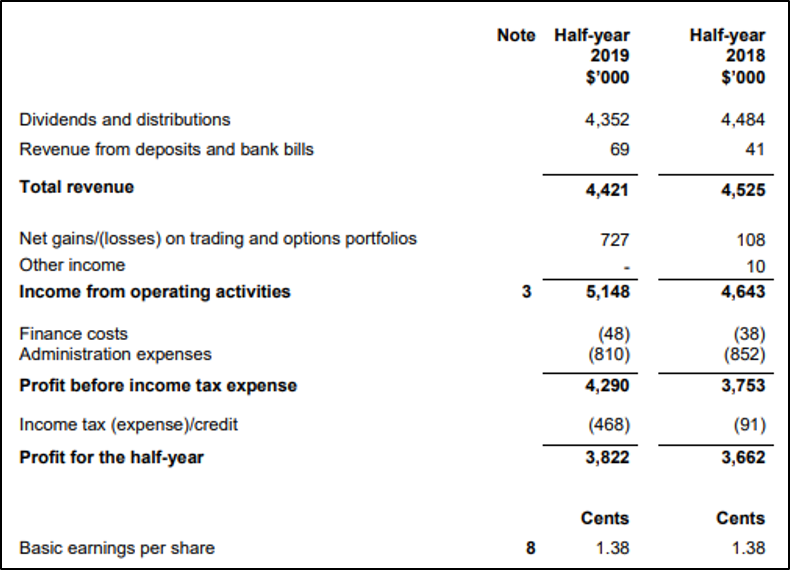

1HFY20 Financial Highlights for the Period ended 31 December 2019: The company reported first-half profit of $3.8 million, an increase of 4.4% year over year. The upside can primarily be attributed to an enhanced result from the trading portfolio. Revenue from investments (excluding capital gains on investments) stood at $4.4 million, representing a decline of 2.3% year over year. Earnings per share came in at $1.38 per share, flat on a year over year basis.

1HFY20 Financial Highlights (Source: Company Reports)

Balance Sheet & Cash Flow Position: The company exited the period with a cash balance of $10.34 million. Net cash inflows from operating activities during the six months period came in at $3.377 million.

Stock Recommendation: As per ASX, the stock is approaching its 52-week high of $1.025. The stock gave a return of 16.41% in the past one year. As per ASX, the stock has a PE multiple of 38.27x and an annual dividend yield of 5.53%. The company remains optimistic about its portfolio, despite uncertainty in economic conditions and elevated geopolitical risks. AMCIL Limited remains on track to focus on investing in better quality companies, which remains a key positive. Considering the above factors, we have a watch view on the stock at the current market price of $0.985 per share,down 1.005% on 21st January 2020.

HUB24 Limited

FUA up by 58% Year Over Year: HUB24 Limited (ASX: HUB) is engaged in providing financing and superannuation portfolio administration services, provision of licensee services to financial advisers and software license and IT consulting customer services.

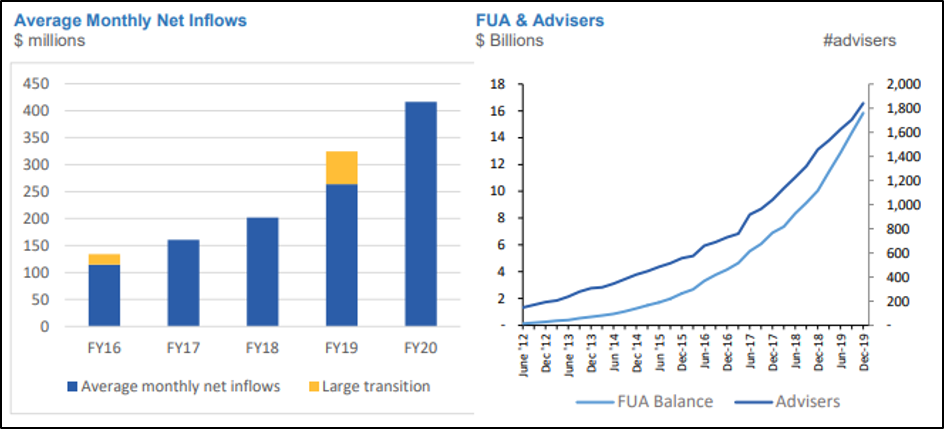

December Quarter Highlights: The company stated that it witnessed a YoY growth of 58% in funds under administration and the figure reached $15.837 billion, implying the quality of the company’s products and customer services.Net inflows for the quarter stood at $1,259 million, reflecting a growth of 67% year over year and gross inflows reached $1,668 million.

Performance Highlights (Source: Company Reports)

Outlook: The company is expected to bolster its foothold in the Australian Wealth Management industry and is well-positioned to take benefits of encouraging tailwinds and the opportunity for future growth. The company expected FUA to be in the range $22 billion to $26 billion by the end of FY21, up by $3 billion from the previously issued guidance.

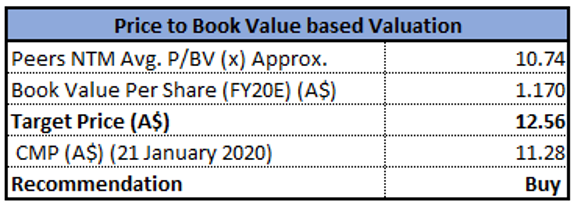

Valuation Methodology: Price to Book Multiple Approach

Price to Book Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading below the average of its 52-week low and high of $9.890 and $15.550, respectively. The stock gave a return of 7.01% in the past one month. As per ASX, the stock has a market cap of $747.9 million with a PE multiple of 103.21x and an annual dividend yield of 0.39%, suggesting a decent opportunity for accumulation. The company’s debt to equity stood at 0.01x in FY19, lower than the industry median of 0.46x, reflecting a strong financial position. In FY19, the company’s ROE came in at 11.7%, higher than the industry median of 6.2%.We have valued the stock using P/B based relative valuation method, and for the said purpose, we have considered peers like Netwealth Group Ltd (ASX: NWL), Magellan Financial Group Ltd (ASX: MFG) and OneVue Holdings Ltd (ASX: OVH), to name few. Therefore, we have arrived at a target price of lower double-digit upside (in percentage terms). Taking into consideration the company’s performance, valuation, and current trading levels, we recommend a “Buy” rating on the stock at the current price of $11.280 per share, down by 5.29% on 21st January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...