.png)

Stocks’ Details

Beach Energy Limited

Decent March Quarter Results:Beach Energy Limited (ASX: BPT) is an oil and gas exploration, development and production company with a market capitalisation of around $3.11 billion as on 27 April 2019. For the period ended 31st March 2020, BPT reported production of 6.9 MMboe, up 8% on pcp, demonstrating the strength and resilience of Beach’s workforce and asset portfolio. Over the quarter, the company saw continued growth in Western Flank oil production which increased by 15% to 2.1 MMbbl. Due to the declining oil price, Q3FY20 sales revenue decreased by 7% relative to the prior quarter. At the end of March quarter, BPT had a net cash position of $80 million and access to $530 million in liquidity.

.png)

Navigating Lower Oil Prices and Covid-19 Impacts: With a prudent financial management system, a diversified natural gas business and strict operating discipline, BPT is currently well placed to manage an extended period of low oil prices, as well as the impact of COVID-19.Following the recent oil price downturn, the company has decided to review its 5 Year Outlook, which is currently planned to be released after the FY20 full year results.

What to expect:The company has lowered its FY20 underlying EBITDA guidance to $1.175 – 1.250 billion, reflecting the lower oil price environment. The company expects 97% of its forecast East Coast gas sales in FY20/21 to be sold under term contract, with less than 25% of these volumes oil-linked. BPT’s FY20 production, capital expenditure and DD&A guidance is currently unchanged, however, the company is now guiding towards the lower end of the range for each metric.

.png)

FY20 Guidance (Source: Company Reports)

Valuation Methodology: EV/Sales Multiple Based Approach (Illustrative)

.png)

EV/Sales Multiple Based Approach (Source Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of BPT is currently trading near its 52-week low of $0.920, offering a decent opportunity for accumulation. For H1FY20, the company reported a net margin of 29.4%, higher than the industry median of 8%. The company has a current ratio of 1.06x, higher than the industry median of 1x. We have valued the stock using EV/Sales multiple based illustrative relative valuation approach and have arrived at a target upside of lower double-digit (in percentage terms). Considering the aforesaid facts, decent performance in March quarter, FY20 outlook, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $1.325, down by 2.93% on 27 April 2020.

Viva Energy Group

Shutting Down of the Geelong Refinery’s Residual Catalytic Cracking Unit:Viva Energy Group Limited (ASX: VEA) is primarily involved in the manufacturing, distribution and supply of petroleum products to retail and commercial customers. On 27 April 2020, VEA announced that it has decided to shutdown the Geelong Refinery’s Residual Catalytic Cracking Unit (RCCU) and associated processing units together with the smaller of the Crude Distillation Units, with effect from early May 2020, in order to further reduce surplus production and continue operations during a period where fuel demand is lower than normal. The company believes that the incremental financial impact of this action will be immaterial in the current refining margin environment and expects no disruption to fuel supply.

March Quarter update: During the three months ended 31 March 2020, the company’s retail segment continued to perform well, with the Alliance network achieving average sales volumes of 62.4 million litres per week in 1Q2020, up 5.1% on pcp. Although there were some declines in aviation sales volumes towards the end of March 2020, the commercial sales volumes for 1Q2020 were overall in-line with pcp. The actual Geelong Refining Margin (GRM) for the March quarter was US$2.7/Barrel (BBL), with refining intake of 10.8MBBLs, impacted by higher crude premiums from purchases made at the end of 2019, and continued lower regional refining margins.

.png)

Refining Figures (Source: Company Reports)

Undertaking Cost Saving Initiatives:In order to preserve cash and minimise the risk associated with commencing projects in the current challenging environment, the company has lowered its FY20 capital expenditure guidance to approximately $60 – 80 million. In addition, the company is undertaking a range of fixed and variable cost saving initiatives across all parts of the business in response to weaker fuel demand.

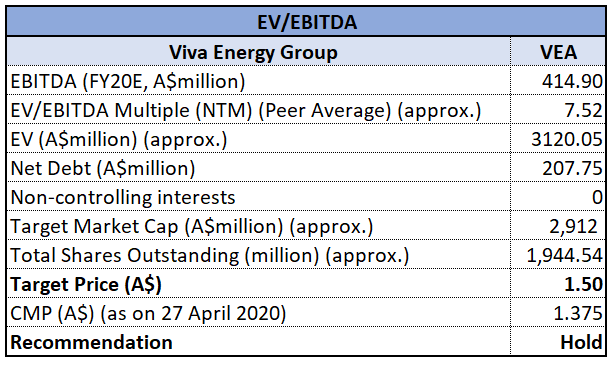

Valuation Methodology: EV/EBITDA Multiple Based Approach (Illustrative)

EV/EBITDA Multiple Based Relative Valuation Approach (Source Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: With the support of capital management and cost saving initiatives, the company is currently well placed to manage the potential impacts of COVID-19. The stock of VEA has declined by 25.48% in the last three months and is inclined towards its 52 weeks low price of $1.125. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with an upside of higher single-digit (in percentage terms). For the purpose, we have taken peers like Caltex Australia Ltd (ASX: CTX), Oil Search Ltd (ASX: OSH) and Worley Ltd (ASX: WOR). Considering the aforesaid facts, decent performance in the March quarter, recent cost saving initiatives and current trading levels, we give a “Hold” recommendation on the stock at the current price of $1.375, up by 1.103% on 27 April 2020.

Strike Energy Limited

West Erregulla Appraisal Plan Approved for Execution:Strike Energy Limited (ASX: STX) is an Australian based, independent oil and gas exploration company with a market capitalisation of around $213.28 million. The company is an operator and holder of a 50% interest in EP469 joint venture, with Warrego Energy Limited holding the remaining interest. On 27 April 2020, the company announced that the EP469 Joint Venture has approved the West Erregulla Appraisal Plan and multi-year work program and budget. The company will now proceed to finalise major procurement activities, to incorporate the addition of WE4 to the previously approved WE3 and capture campaign savings.

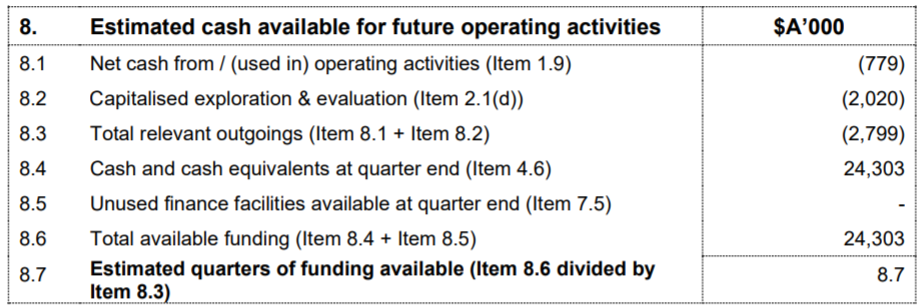

Cash Position:During the March quarter, the company continued to work to deliver the West Erregulla gas project in line with its aspired timeline. For the quarter, the company reported cash outflow from operating activities of $779k, cash outflow from investing activities of $2,143k and cash outflow from financing activities of $14k. At the end of the March quarter, the company had a cash balance of $24.303 million. In the upcoming future, the company expects to incur around $2.02 million on capitalised exploration & evaluation.

Cash Available for Future Operating Activities (Source: Company reports)

Stock Recommendation: With the requisite funding in hand, and a safe and experienced Board armed with a resilient strategy, the company has maintained the excellent momentum it commenced the year with. All appraisal wells which will be constructed at EP469, are expected to be used as future producers to support the proposed Phase 1 Development. In the last six months, the stock of STX has declined by 56.9% and is inclined towards its 52 weeks low price of $0.054, offering a decent opportunity for accumulation. Considering the company’s upcoming appraisal drilling campaign at the West Erregulla gas field, its development pipeline and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.125 as on 27 April 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...