.png)

Stocks’ Details

IDP Education Limited

Announcement of Share Purchase Plan: IDP Education Limited (ASX: IEL) is an education service provider which places international students into education institutions in Australia, UK, USA, Canada, New Zealand and Ireland. As on 14 April 2020, the market capitalization of the company stood at $4 billion. The company has recently invited eligible shareholders to apply for up to $30,000 of new fully paid ordinary shares under its Share Purchase Plan without incurring brokerage or other transaction costs.

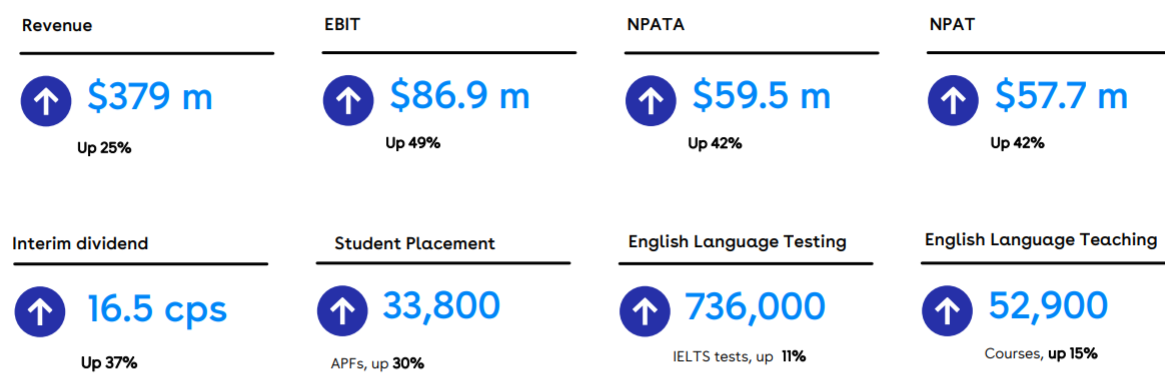

During 1H20, the company witnessed an increase of 25% in revenue to $379 million and a growth of 42% in NPAT to $57.7 million. This growth was mainly due to growth in student placement and increasing trend of English Language Testing volume. The improvement in financial performance resulted in strong margins through operational efficiencies and a slower investment in overheads.

1H20 Financial Highlights (Source: Company Reports)

Future Expectations: The breakout of COVID-19 has taken a toll on the global economy. The company is likely to have a material impact on its performance as many of its IELTS testing locations are suspended. However, it is taking pre-emptive measures to benefit from opportunities after this period. The company is sufficiently liquid and is focusing on preserving global talent.

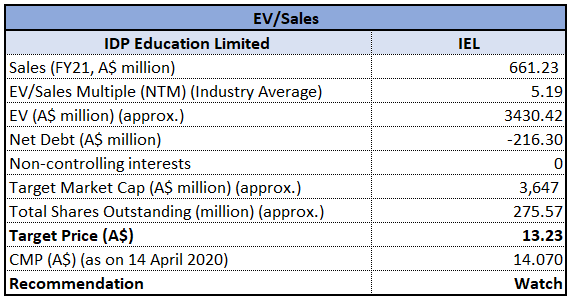

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Method

EV/Sales Multiple Based Relative Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of IEL gave a negative return of 7.46% in the past 6 months and a negative return of 12.58% in the past one month. The stock is also trading close to its 52-weeks’ low level of $9.9. Travel restrictions and school closures in all destination markets is likely to materially affect the performance of the company. During 1H20, gross margin of the company stood at 66.9% as compared to the industry median of 67.5% and net margin of the company was 15.2% relative to the industry median of 17.2%. Considering the current trading levels, negative returns and uncertainty due to COVID-19, we have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at an indicative downside of single-digit (in percentage terms). Hence, we have a watch stance on the stock at the current market price of $14.070, down by 3.099% on 14 April 2020.

G8 Education Limited

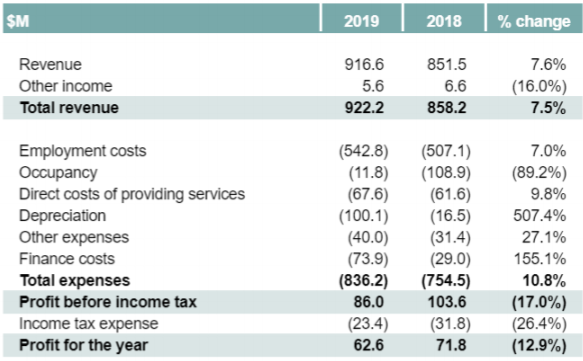

Successful Completion of Placement and Institutional Entitlement Offer: G8 Education Limited (ASX: GEM) operates early education centres. The company has recently announced the successful completion of its institutional placement wherein it has raised a total of $227 million at $0.80 per new share. The company has also announced that Mitsubishi UFJ Financial Group, Inc. has ceased to be a substantial holder. During FY19, the company reported an increase of 7.5% in revenue to $922.2 million and organic earnings growth of 3% after investment in quality. This was driven by occupancy, fee growth and acquisitions. GEM has a resilient balance sheet with lower costs and longer tenor in debt structure.

FY19 Financial Highlights (Source: Company Reports)

What to Expect: The company is prioritizing to drive growth in Turnaround and Greenfield centres with a target of around 50 centres in Q1 CY20. GEM will continue to evaluate acquisition opportunities and will focus on driving cost efficiencies to support EBIT acceleration. The company has confirmed that its 2020 AGM will be held on 17 June 2020.

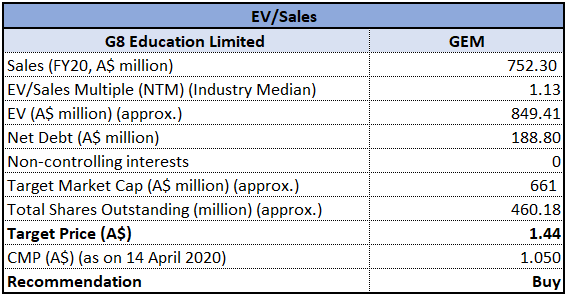

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Method

EV/Sales Multiple Based Relative Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of GEM is trading close to its 52-weeks’ low level of $0.437, proffering a decent opportunity for accumulation. During FY19, gross margin of the company stood at 92.6%, higher than the industry median of 64.7%. In the same time span, EBITDA margin of the company witnessed an improvement over the previous year and stood at 28.6%, up from 17.4% in FY18. Considering the trading levels, improvement in margins and positive outlook, we have valued the stock using EV/Sales multiple based illustrative relative valuation method and have arrived at an indicative target price with an upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $1.050, down by 2.778% on 14 April 2020.

3P Learning Limited

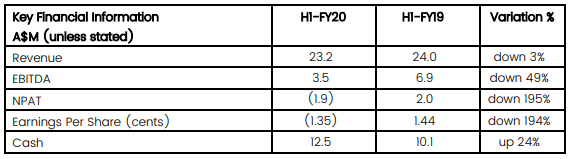

Appointment of New CFO: 3P Learning Limited (ASX: 3PL) is involved in the development, sales and marketing of online educational programs to schools and parents of school-aged students. The market capitalisation of the company stood at $122.75 Mn as on 14th April 2020. 3PL has recently appointed Dimitri Aroney as Chief Financial Officer. The sales execution issues in APAC in 2H FY19 have resulted in licence loss and have adversely impacted its H1-FY20 result. This resulted in a fall of 3%, 49% and 195% in revenue, EBITDA and NPAT during 1H FY20, respectively.

The company also witnessed a decline of 1% in global licences from 30 June 2019 due to the start of school year churn in the first half in the UK and the Americas. However, it witnessed a growth of 4% in licences in APAC. The company experienced growth in new business billings on current products and ARR in all regions.

Key Financials (Source: Company Reports)

Expected Growth in Revenue and EBITDA: 3PL anticipates growth in revenue and EBITDA for 2H FY20 as compared to 2H FY19 mainly due to new business billings on current products and growth in ARR in all regions, stronger products in the market and roll out of new products scheduled for this year.

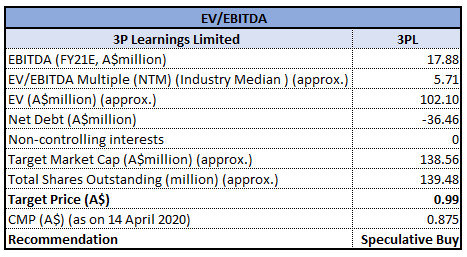

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 0.95x in 1H FY20, reflecting YoY growth of 6.5%. This reflects that the company has enhanced its position to pay its short-term obligations. During 1H FY20, the company witnessed a rise of 24% in cash position from $10.1 million to $12.5 million. We have valued the stock using EV/ EBITDA multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). Therefore, in light of the improved liquidity position and decent outlook, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.875 per share, down by 0.568% on 14 April 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...