Stocks’ Details

The Citadel Group Limited

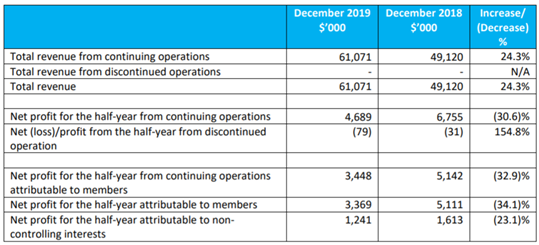

Acquisition of Wellbeing on Track: The Citadel Group Limited (ASX: CGL) is a software and technology company which specialises in managing information in complex environments cross health, national security, defense and corporate enterprises. On 24 March 2020, Citadel Group confirmed that the acquisition of Wellbeing is on track to complete by 3 April 2020. An Extraordinary General Meeting to approve the Conditional Placement is going to be held in Melbourne on 30 March 2020. This acquisition will help Citadel to transform into a global healthcare software company with multiple growth opportunities. The below image depicts the company’s performance in the first half of FY20.

Half-Year Results (Source: Company Reports)

Taking Initiatives to Tackle Covid-19 Impacts: With regards to effects on its business from Covid-19, the group has assured that no significant projects or contracts have been delayed or cancelled in the period following the release of its H1FY20 results. In order to deal with the uncertainty around the covid-19 impacts, Citadel group has placed plans to reduce operating expenses, defer any non-essential capital projects, and manage liquidity and cash flow within bank covenants. Due to restrictions on hospitality venues, Citadel has also relocated its physical EGM to the Company’s offices in Melbourne

What to expect: Following the acquisition of Wellbeing, Citadel expects to have a combined cash balance of approximately $10 million and an additional undrawn working capital facility of $10 million, with sufficient headroom within banking covenants. In FY20, the company expects to deliver revenue and EBITDA growth, supported by low double-digit organic revenue growth, with pre Noventus margins broadly consistent with FY19.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation

Price to Earnings Multiple Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Citadel’s stock is trading close to its 52-week low of $1.30, offering a decent opportunity for accumulation. For H1 FY20, the company maintained a current ratio of 1.96x which is higher than the ratio of 1.63% in pcp. This demonstrates that the company has improved its ability to pay short-term debts. We have valued the stock using the price to earnings based relative valuation method and arrived at a target upside of higher single-digit (in percentage terms). Considering the company’s expected acquisition of Wellbeing, its resilient performance in the current challenging times, and decent outlook, we are giving a “Buy” recommendation on the stock at the current market price of $1.515, up by 24.691% on 24 March 2020, owing to the updates related to acquisition of Wellbeing and Covid-19.

Technology One Limited

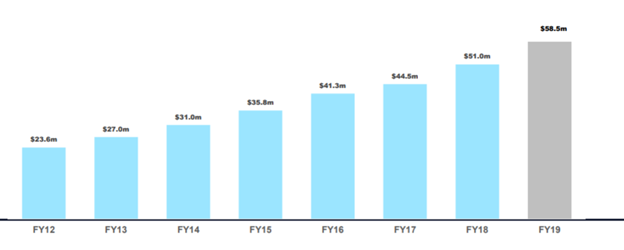

Strong Growth in SaaS Business: Technology One Limited (ASX: TNE) is a leading enterprise Software as a Service (SaaS) company in Australia which has been providing customers enterprise software that evolves and adapts to new and emerging technologies. In FY19, the company reported a Net Profit Before Tax of $76.4 million. The company’s SaaS business is growing strongly. In the last four years, SaaS ARR (Average Recurring Revenue) has grown at a rate of 44% per annum. The company’s profit margin also continues to grow and is currently at 27%, driven by the significant economies of scale from our single instance global SaaS ERP solution. On 2nd March 2020, the company announced the appointment of highly experienced Mr. Peter Ball as an independent, Non-Executive Director.

Reported Net Profit After Tax Summary (Source: Company Reports)

What to expect: The company believes that its pipeline for 2020 is strong. It expects to double in size in the next 4 to 5 year and its total ARR as a % of Revenue is expected to be 93% by FY25. The company expects strong profit growth to continue in 2020. The company expects to provide further guidance with the first half results.

Stock Recommendation: In the past three months, TNE stock has provided a negative return of 17.92% to its shareholders. In the second half of FY19, the company reported a net margin of 25.9%, which is lower than the industry median of 29.1%. Considering, the company’s expected growth in the near future, uncertainty around the covid19 impacts and its current trading levels, we suggest investors to keep an eye on the stock and have a watch stance at the current market price of $7.320, up by 1.808% on 24 March 2020.

NEXTDC Limited

No Noticeable Change to NEXTDC’s Sales Pipeline: NEXTDC Limited (ASX: NXT) is an ASX200-listed technology company, primarily involved in the establishment, development and operation of data centre facilities. On 19 March 2020, the company provided an update on COVID-19 impacts, wherein it informed that there has been no noticeable change to NEXTDC’s sales pipeline and its underlying demand for NEXTDC’s premium data centre services is expected to remain robust. The company also informed that the risk of any material supply-side impacts to the Company’s operations and ongoing developments are currently considered to be low.

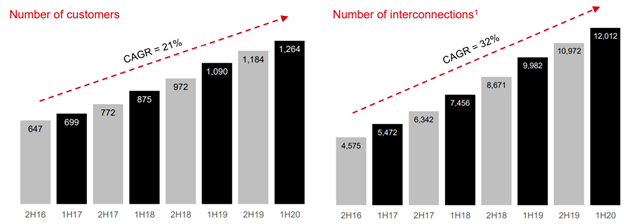

Decent Half-year Performance: In the first half of FY20, the company’s revenue from data centre services increased by 13% to $95.4 million and the number of interconnections increased by 20% to 12,012, representing 8.2% of recurring revenue. The growth in average interconnections highlights the increasing use of hybrid cloud and connectivity both inside and outside the data centre as customers expand their ecosystems. For the half-year period, the company reported Underlying EBITDA of $50.9 million, up 21% on pcp.

Strong growth in customers and interconnections (Source: Company reports)

Decent Guidance: For FY20, the company expects its revenue to be in the range of $200 million to $206 million and its Underlying EBITDA to be in between $100 million to $105 million. For the year, the company expects its capital expenditure to be in between $320 million to $340 million.

Stock Recommendation: The company has a robust balance sheet with approximately $450 million of cash and committed undrawn bank facilities available as at 29 February 2020, with no debt maturities until June 2021. Hence, considering the company’s resilient performance in the current challenging climate, its decent H1FY20 performance, and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $7.590, up by 8.895% on 24 March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...