Stocks’ Details

Bellamy's Australia Limited

Clarification on SAMR Approvals: Bellamy's Australia Limited (ASX: BAL) is engaged in the distribution and production of branded food products. The market capitalisation of the company stood at A$996.51Mn as on 15th July 2019. As per the release dated 24th April 2019, the company stated that the State Administration for Market Regulation (or SAMR) released a series of approvals, three of which are related to approval of a new Bellamy’s branded formulation-series, which is to be produced at the ViPlus Dairy facility. In the release dated May 1, 2019, it was mentioned that ViPlus Dairy’s formula-series registration amendment has been approved by State Administration for Market Regulation but Bellamy’s organic formula-series application is pending.

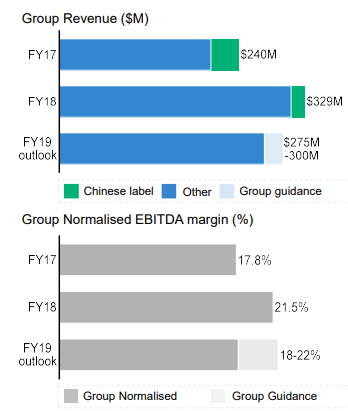

What to Expect: The company is expecting group revenue to be in the range of $275Mn- $300Mn and normalised EBITDA margin is expected to be between 18-22%. In 1H FY 2019 results presentation, the company also stated that the medium-term outlook happens to be compelling, which is supported by the category fundamentals, differentiated position and an aggressive 3-year growth strategy.

Group Revenue and EBITDA Margin (Source: Company Reports)

Stock Recommendation: Bellamy's Australia Limited’s current ratio was 4.84x in 1H FY19 as compared to the industry median of 1.42x. This implies that BAL is in a good position to meet its short-term obligations against the broader industry. On the stock’s past performance front, it yielded returns of 9.46% and 21.41% in the time span of one month and six months, respectively. However, in the time period of three months, it produced negative returns of 10.94%. Hence, considering the aforesaid facts and current trading level, we give a “Speculative Buy” rating on the stock at the current market price of A$9.050 per share (up 2.958% on 15th July 2019).

Bega Cheese Limited

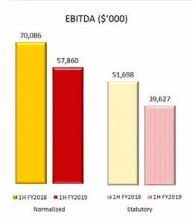

Appointment of Alternate Director: Bega Cheese Limited (ASX: BGA) is into the manufacturing, processing, packaging and cutting of traditional cheese products. The market capitalisation of the company stood at A$968.21Mn as on 15th July 2019. Recently, the company, via a release, stated that it had extended the leave of Mr Barry Irvin for around six months. Mr Irvin has appointed long time director Max Roberts as his alternate director for the duration of his leave. Adding to that, it was mentioned that Mr Roberts will also be acting as Chairman of the Board of Directors during this period. The company reported $0.65 billion of revenues, reflecting a rise of 5.8% on pcp and normalised EBITDA stood at $57.9 million in 1H FY 2019.

EBITDA (Source: Company Reports)

Future Aspects: The company’s business priorities mainly revolve around focusing towards the manufacturing footprint and cost structure as well as towards milk volume and product mix. The inventory management is also a key priority for the company. The company is expecting that global dairy supply and demand would be more balanced moving forward. It is also expecting normalised EBITDA for FY 2019 at the bottom end of range after recent farm gate milk price increases.

Stock Recommendation: The current ratio stood at 2.06x in 1H FY19 against the industry median of 1.42x, which represents that, it is well positioned to address its short-term obligations. It reported a higher EV/EBITDA and Price/Cashflow multiples of 11.8x and 52.1x respectively against the industry median of 8.5x and 3.9x respectively indicating the stock to be overvalued.

With respect to the stock’s past performance, it provided returns of -9.76% and -7.93% in the time span of one month and three months, respectively. As per ASX, the stock is trading closer towards its 52-week lower levels with high PE multiple of 65.65x which is higher than the industry average of 9.3x. By looking at the higher than industry EV/EBITDA, Price/Cashflow, and P/E multiples, we have a wait and watch stance on the stock at the current market price of $4.480 per share (down 1.104% on 15th July 2019).

Select Harvests Limited

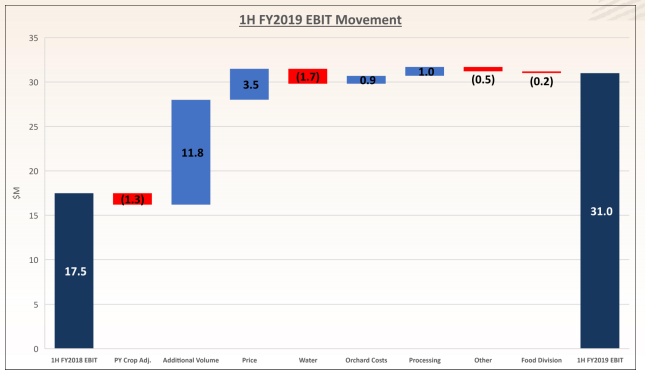

Changed Financial Year End: Select Harvests Limited (ASX: SHV) is involved in the growing, processing, packaging and marketing of almonds from company and investor owned orchards. The market capitalisation of the company stood at $681.64 Mn as on 15th July 2019. Recently, the company has changed its financial year-end from 30th June to 30th September. The 50% of fair value of 2019 crop has been recognised in line with completed harvest activity. SHV reported EBIT of $31.0Mn in 1H FY19 as compared to $17.5 Mn in 1H FY18, which reflects a massive rise of 77.1% on pcp. Adding to that, it posted EBITDA amounting to $38.5Mn in 1H FY19 in comparison to $25.9Mn in 1H FY18, which was driven by larger crop and firm A$ pricing.

EBIT Movement (Source: Company Reports)

Future Prospects: The company’s priorities include ensuring optimal tree health for 2020 Crop Horticultural Program. It is planning to continue to decrease cost per kg throughout all the production stages. The company will be focused on food export growth. As the company is having decent liquidity levels (as evident from the current ratio), it can make deployments towards key strategic business activities which might help it in achieving respectable growth rates.

Stock Recommendation:The gross margin of the company stood at 21.2% in 1H FY19 as compared to the industry median of 40.7%. Current ratio stood at 3.30x in 1HFY19, which is higher than the industry median of 1.42x. When it comes to the stock’s past performance, it produced returns of 1.86% and 3.79% in the time span of one month and three months, respectively.

As per ASX, the stock is trading closer towards 52-week higher levels of $7.660 with PE multiple of 19.720x. Hence, in the view of aforesaid facts and current trading level, we have a watch stance on the stock at the current market price of $7.100, down 0.281% on 15 July 2019 and suggesting that investor should wait for a better entry level.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...