.png)

Stocks’ Details

Myer Holdings Limited

Reopening of Stores:Myer Holdings Limited (ASX: MYR) is Australia’s leading departmental store group with a market capitalisation of around $217.64 million. In a recent business update, the company came up with positive news of the reopening of its 24 stores on a staged and trial basis. The company also informed about the reopening of all its stores from 27 May 2020 onwards. It is worth noting that the company’s online business has continued to perform strongly amid Covid-19 period.

Substantial Holders Update:On 29 May 2020, the company notified that Investors Mutual Limited is ceased to be a substantial holder in the company.

H1FY20 Performance Highlights: For H1FY20, the company had reported total sales of $1,607.9 million, down by 3% on pcp, impacted by the exit of Apple and the Country Road Group brands, and a disappointing performance in Womenswear. However, the company’s online sales grew by 25.2% to $168.2 million in H1FY20, representing 10.5% of total sales. Over the half-year period, the company made solid progress in implementing Customer First Plan initiatives despite macro headwinds. For H1FY20, the company recorded a statutory NPAT of $24.4 million.

.png)

H1FY20 Results (Source: Company Reports)

Current Strategy:The company continues to take all necessary measures to minimise costs, including engaging in ongoing discussions with suppliers and landlords. At this point, the company is focused on opening its stores while maintaining all safety and cleaning measures.

Valuation Methodology:P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the last six months, the stock of MYR has corrected 47.52% on ASX and is inclined towards its 52-week low, offering an opportunity for accumulation. We have valued the stock using a price to earnings multiple based illustrative relative valuation method and have arrived at a target price with low double-digit upside (in % terms). For the purpose, we have taken peers like Baby Bunting Group Ltd (ASX: BBN), Adairs Ltd (ASX: ADH) and Ardent Leisure Group Ltd (ASX: ALG). Considering the company’s recent steps to reopen its stores, growth in online sales, and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.250, down by 5.66% on 12 June 2020.

Kathmandu Holdings Limited

Higher online sales in April 2020:Kathmandu Holding Limited (ASX: KMD) is a global outdoor and actions sports company with a market capitalisation of ~$772.81 million. S&P Dow Jones Indices recently added KMD in its S&P/ASX 300 Index, effective from 22 June 2020. In a recent business update, the company informed that its online sales in April 2020 were 2.5 - 3 times higher than the previous year. The company is now focused on staged reopening of physical stores with an absolute focus on employee and customer safety.

$207 million Equity Raising: On 1 April 2020, the company announced a fully underwritten $207 million equity which comprises a $177 million 1.2 for 1 pro-rata accelerated entitlement offer and $30 million placement to certain institutional investors. On 22 April 2020, the company announced the successful completion of the retail entitlement offer component. This capital raising is expected to strengthen the company’s balance sheet and it will provide enough capital to the company to go through the current market uncertainties caused by COVID-19.

H1FY20 Highlights:For H1FY20, the company reported total sales of NZ$363.7 million, up 58.8% on pcp. Further, the company reported an underlying EBIT of NZ$29.0 million, up 46.5% on pcp. One of the major achievements during the period was the acquisition of Rip Curl which substantially diversified the company’s revenue and earnings streams.

.png)

H1FY20 Financial Performance (Source: Company Reports)

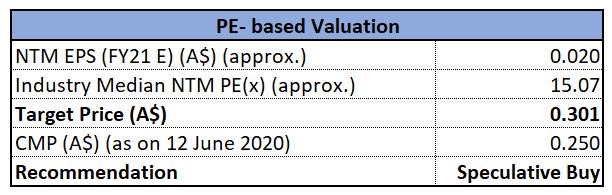

Valuation Methodology:P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the last six months, the stock of KMD declined by 48.32% on ASX and is inclined towards its 52-week low, offering a decent opportunity for accumulation. The stock is trading at a PE multiple of 5.140x with an annual dividend yield of 13.17%. We have valued the stock using a price to Earnings multiple based illustrative relative valuation method and have arrived at a target price with low double-digit upside (in % terms). Considering the company’s recent capital raising, decent H1FY20 performance, and surge in online sales, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.040, down by 4.587% on 12 June 2020.

Jumbo Interactive Limited

Covid-19 Update:Jumbo Interactive Limited (ASX: JIN) a leading digital retailer of both national jackpot lotteries and charity lotteries. JIN was recently removed from the S&P/ASX 200 Index, effective from June 22, 2020. In response to Covid-19, the company has implemented work from home initiatives with minimal impact on operations. Due to the COVID-19 crisis, the company expects some minor delays in the progress of the Lottery SaaS (Software as a Service) business. The Pacific Islands ticket selling business is affected by the closure of public places in those countries, however, the TTV (Total transaction value) is around 1.6% of total TTV so no material impact is expected.

FY20 Expectations: For FY20, the company expects its TTV to be between $335 to $341 million and revenue to be in the range of $68.5 to $69.9 million. Both TTV and revenue are expected to be underpinned by improved customer engagement. The company expects its FY20 NPAT to be in the range of $24.4 to $25.3 million. The company anticipates increased expenditure in FY20, the benefits of which are expected in FY21.

.png)

FY20 Guidance (Source: Company Reports)

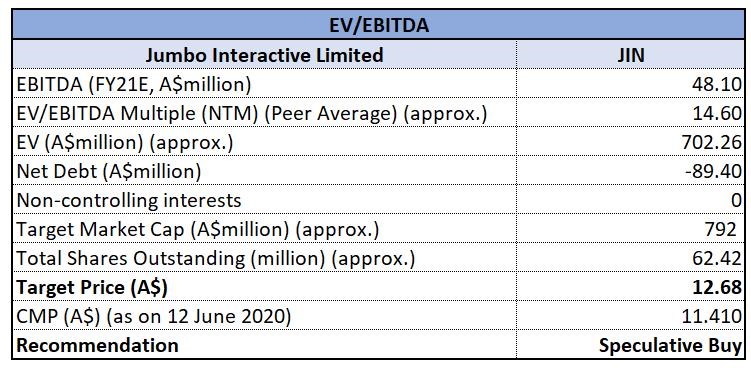

Valuation Methodology:EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:As at 20 February 2020, the company was in a healthy financial position with no debt and surplus cash of $65.5 million. The company has a current ratio of 3.42x, higher than the industry median of 1.17x, demonstrating that the company is well equipped to pay its short-term obligations. Over the last three months, the stock of JIN has increased by 34.75%, but it is still trading close to its 52-week low price, offering a decent opportunity for accumulation. We have valued the stock using an EV/EBITDA multiple based illustrative relative valuation method and have arrived at a target price with low double-digit upside (in % terms). Considering the company’s FY20 expectations, its healthy financial position and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $11.410, down by 0.262% on 12 June 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...