Stocks’ Details

Ainsworth Game Technology Limited

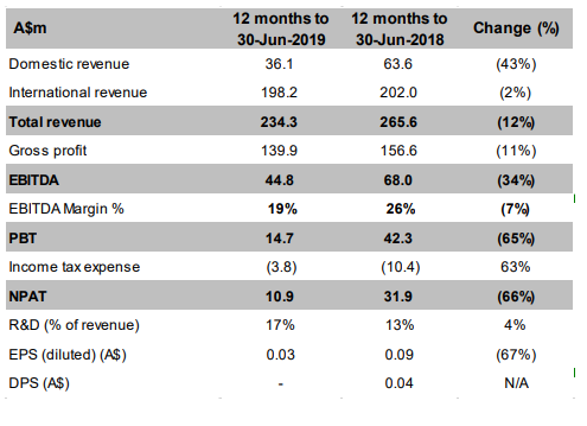

Strategy to Expand Internationally: Ainsworth Game Technology Limited (ASX: AGI) is involved in the design, development and manufacture of gaming machines. The market capitalisation of the company stood at $245.86 million as on 30th January 2020. The company recently announced that Spheria Asset Management Pty Ltd has made a change to its substantial holding in the company on 3rd December 2019 and the current voting power stands at 6.23% as compared to the previous voting power of 5.16%. During FY19, the company reported revenue amounting to $234 million and profit after tax stood at $11 million. The company added that international sales currently account for 85% of the group total, which is consistent with its strategy to expand the company’s global footprint.

Profit & Loss Summary (Source: Company Reports)

What to Expect: The company’s strategy revolves around leveraging its excellent industry reputation, international footprint, scale, as well as R&D for generating long term growth and improved returns. For FY20, the company is aiming for selective acquisitions to drive financial performance.

Stock Recommendation: Current ratio of the company stood at 5.79x in FY19 as compared to the industry median of 1.08x. This reflects that the company is in a decent position to address its short-term obligations as compared to the broader industry. Debt to equity multiple of the company stood at 0.14x in FY19 against the industry median of 0.49x. On TTM basis, the stock is trading at an EV/Sales multiple of 1.0x, lower than the industry median (Consumer Cyclicals) of 1.3x. It is trading at an EV/EBITDA multiple of 6.6x, lower than the industry median (Consumer Cyclicals) of 8.1x. Therefore, considering a decent liquidity position and improved balance sheet, we give a “Buy” recommendation on the stock at the current market price of A$0.740 per share, up by 1.37% on 30th January 2020.

Crown Resorts Limited

Decent Returns Paid to Shareholders: Crown Resorts Limited (ASX: CWN) is an international casino and gaming company. The market capitalisation of the company stood at A$7.82 Bn as on 30th January 2020. The company recently announced that Perpetual Limited and its related bodies corporate, made a change to their substantial holdings on 23rd January 2020 and the current voting power stands at 7.09% as compared to the previous voting power of 6.08%. In another update, the company announced that it has wrapped up the purchase of the One Queensbridge development site.

During FY19, the company continued to pay cash returns to shareholders and declared a final dividend amounting to 30 cps, which brought the total dividend for FY19 to 60 cps. The following picture provides an idea of financial performance for FY19:

.png)

Financial Performance for FY19 (Source: Company Reports)

Focus on Maximising Shareholder Returns: The company is well-positioned in order to finance its Australian development project pipeline with the help of available liquidity amounting to $1,192.5 million. The company is also focused on maximising shareholder returns by recognising opportunities for delivering improved operating performance at Crown Melbourne, Crown Perth as well as Crown Aspinalls.

Stock Recommendation: Net margin of the company stood at 13.8% in FY19 as compared to the industry median of 9.2%. This reflects that the company possesses decent capabilities to convert its top-line into bottom-line, as compared to the broader industry. Gross margin and EBITDA margin of the company stood at 22.2% and 29.9% in FY19, reflecting YoY growth of 2.8% and 3.3%, respectively. On TTM Basis, the stock is trading at an EV/Sales multiple of 2.5x, lower than the industry average of 3.7x.Hence, in the light of decent capabilities to convert the topline into bottom-line and improvement in key margins, we give a “Buy” recommendation on the stock at the current market price of $11.600 per share, up 0.433% on 30th January 2020.

G8 Education Limited

Completion of Divestment in Western Australia: G8 Education Limited (ASX: GEM) is engaged in the operation of early education centres and ownership of early education centre franchises. As on 30th January 2020, market capitalization of the company stood at $869.73 million. The company has recently announced that it has completed the sale of 25 centres in Western Australia for a consideration of ~$6.4 million. These proceeds will be used to repay debt.

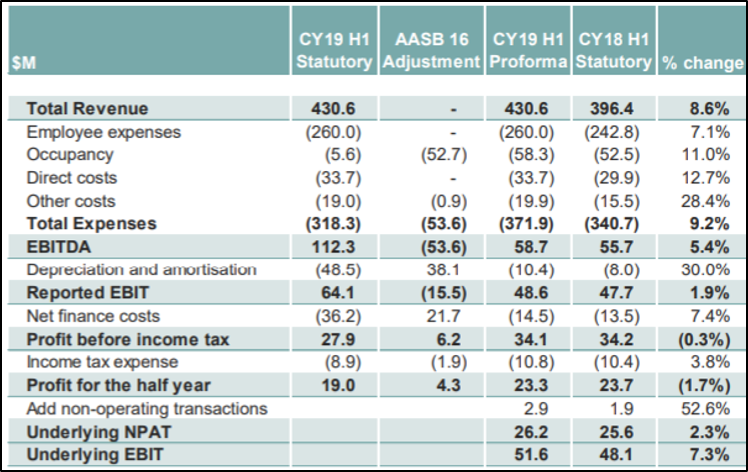

During 1H19, total revenue of the company went up by 8.6% and stood at $430.9 million. This was driven by increased occupancy, fee growth and acquisitions. In the same time span, Underlying EBIT was in-line with half-year consensus and stood at $51.6 million, up by 7.3% on prior corresponding period.

Financial Performance (Source: Company Reports)

What to Expect: The company expects CY19 occupancy growth to be around 1% on prior year. This translates to a revenue shortfall of $7 million and has a significant flow-on effect to EBIT due to its seasonal earnings profile. GEM expects full-year underlying EBIT to be in the range of $131 million to $134 million and the impact of AASB16 will increase this EBIT range by approximately $30 million.

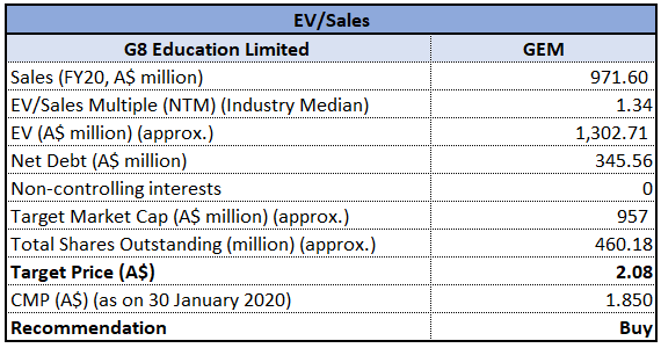

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of GEM is trading very close to its 52-weeks’ low level of $1.832, proffering a decent opportunity for accumulation. For 1H19, gross margin of the company stood at 92.2%, higher than the industry median of 67.1%. This indicates that the company is managing its costs well and is able to convert its top-line into profits. Considering the trading levels, high gross margin and decent outlook, we valued the stock using EV/Sales based relative valuation method and have arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $1.850, down by 2.116% on 30th January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...