.png)

Stocks’ Details

Speedcast International Limited

Cost-Cutting Initiatives on Track: Speedcast International Limited (ASX: SDA) is a global remote communications supplier. It provides satellite services, including network service, value-added services, equipment sales and wholesale Voice over Internet Protocol (VoIP) to enterprise customers and government.

Recent Updates: On 10 December 2019, the company announced that Southeastern Asset Management, Inc has been ceased to be a substantial shareholder of the company, effective from 9th December 2019. On 9th December 2019,SDAnotified that National Australia Bank Limited and its associated entities ceased to be a substantial shareholder of the company, effective from 4th December 2019.

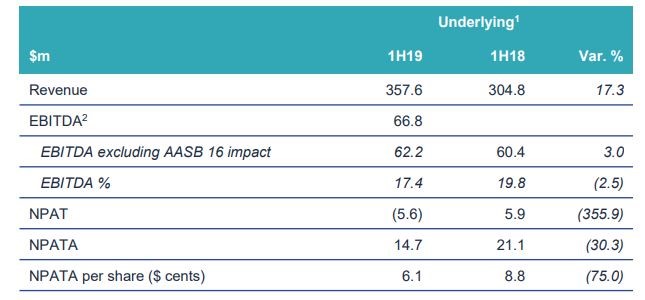

Results for Six Months Ended 30 June 2019: The company reported group revenue of $357.6 million, up 17.3% year over year. Underlying net losses during the period stood at $5.6 million. EBITDA (excluding AASB 16 impact) came in at $62.2 million, up 3% on yoy. Cash and Cash equivalents at the end of the period came in at $54.6 million.

Financial Highlights (Source: Company Reports)

Outlook: The company reiterated its guidance for EBITDA and expects the same to be in the range of $150 million to $160 million in 2019. The company expects cost savings of $10 million in the second half of 2019, along with annualised savings of $20 million.

Valuation Methodology:Price to Book Value Multiple Valuation

.png)

Price to Book Value Multiple Based Valuation (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the stock is trading below the average of its 52-week trading range. As on 12 December 2019, the company’s market capitalisation stands at ~ $173.81 million, with 239.74 million outstanding shares. The company is focused on reducing overall costs by the end of the year. Moreover, Globecomm’s integration in 2020 is expected to provide revenue synergies in the future. Cost synergies from Globecomm are expected to be in the range of $18 - $20 million in 2020. Considering the aforesaid facts, we have valued the stock using one relative valuation, i.e., price to book value and arrived at a target price of a higher single-digit upside in % terms. Hence, we give a “Speculative Buy” rating on the stock at the current market price of $0.730 per share, up 0.69% on 12 December 2019.

Superloop Limited

Higher Focus on Connectivity and Broadband Services Across Asia-Pacific: Superloop Limited (ASX: SLC) is engaged in the construction and operation of independent telecommunications infrastructure in the Asia Pacific Region. On 10th December 2019, the company announced that Jon Tidd, CFO of the company, will be shifted to take the leading position in Customer Operations and will work as the Chief Customer Officer (CCO) of the company. The current move is aimed at addressing the robust demand for Superloop’s connectivity and broadband services across the Asia Pacific region.

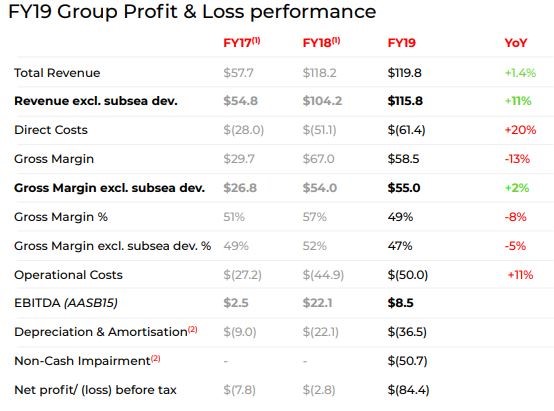

Financial Highlights for the Year Ended 30th June 2019: During the year, the company reported total revenue of $119.8 million, up 1.4% year over year. Gross margin came in at $58.5 million as compared to $67 million in FY18. EBITDA for the period stood at $8.5 million in FY19 as compared to $22.1 million in FY18, primarily due to lower-than-expected subsea development margin, fixed wireless margin and high operating expenditure.

FY19 Group Profit and Loss Performance (Source: Company Reports)

Cash Flow & Balance Sheet Update: Operating cash flows for the period came in at $5.3 million as compared to $37.9 million in FY18. Net cash flows came in at $18.9 million. Net debt at the end of the period stood at $70.3m.

Outlook: Underlying EBITDA is expected to be in the range of $14-$16 million in FY20 on the back of strong growth in core fibre connectivity business and complimentary offerings returning to growth. In FY20, the company expects to focus more on executing master service agreements, contracts and orders to offer higher connectivity and broadband services to customers and expects to drive operational productivity.

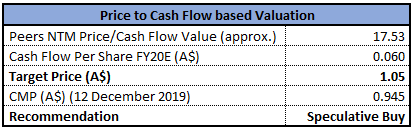

Valuation Methodology:Price to Cash Flow Multiple Valuation

Price to Cash Flow Multiple Based Valuation (Source: Thomson Reuters)

Stock Recommendation: As per the ASX, the stock is trading below the average of its 52-week high and low. As on 12 December 2019, the company’s market capitalisation stands at ~ $336.6 million. The business promises a better future with an increased focus on implementing master service agreements, contracts and orders to offer higher bandwidth services to customers. Underlying EBITDA guidance range for FY20 excluding anticipated infrastructure transaction depicts decent growth year-on-year. Considering the aforesaid facts, we have valued the stock using one relative valuation, i.e., price to cash flow and arrived at a target price depicting lower double-digit upside in % terms. Hence, we give a “Speculative Buy” rating on the stock at the current market price of $0.945 per share, up 2.717% on 12 December 2019.

Sky and Space Global Limited

Revocation of Interim Stop Order: Sky and Space Global Limited (ASX: SAS) is a satellite company and is involved in the development of a narrow-band communication network. The company provides cellular networks and voice and instant messaging services with a low cost of maintenance. The company recently notified that the Interim Stop Order made on 21 November 2019, has been revoked by the Australian Securities and Investments Commission, after lodgement of a supplementary prospectus by SAS on 10 December 2019.

Entitlement Issue:Sky and Space Global Ltd announced an Entitlement Issue of up to 2,175,014,261 fully paid ordinary shares at a price of $0.005 per new share to all the shareholders of the company.This entitlement will raise upto $10,875,071. It will also issue 1 free option for every 4 shares subscribed for by shareholders, exercisable at a price of $0.015 and expiring on or before 31 May 2021.

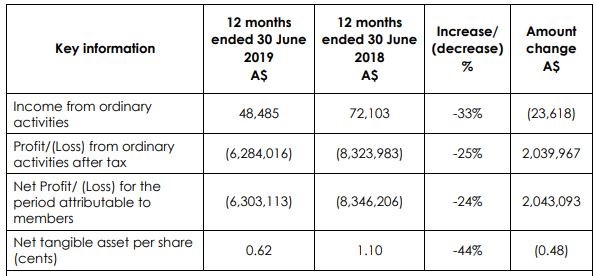

FY19 Key Financial Highlights (for the Period Ending 30th June 2019): During the year, Income from ordinary activities came in at $48,485 as compared to $72,103 reported in the year ago period. Net loss for the period came in at $6.28 million as compared to the loss of $8.32 million in the previous year. As of 30 September 2019, the company had a cash balance of $475k.

Financial Highlights (Source: Company Reports)

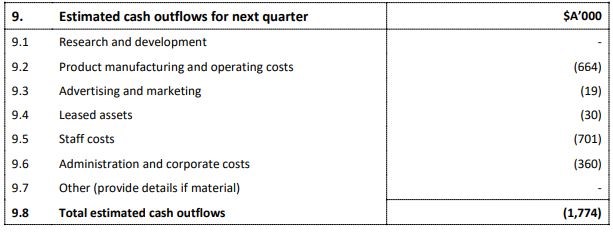

Outlook: In the coming quarter ending 31 December 2019, the company is expecting net cash outflow amounting to be $1.774 million.

Cash Flow Prediction (Source: Company Reports)

Stock Details: In the last five trading sessions, the stock gained 3.7%. The company had requested for a voluntary suspension to its securities for the purpose of completing its financial arrangements and to bring in two new non-executive directors with relevant expertise. The shares were supposed to be suspended until the release of any market update on the above matters.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...