G8 Education Limited

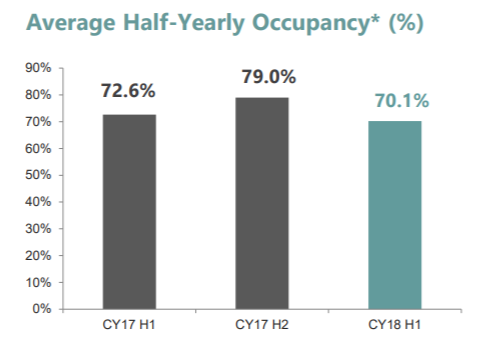

Operational Challenges will Continue in Near Term:G8 Education Limited (ASX: GEM) was formed after the merger of Early Learning Services and Payce Childcare in March 2010. As of now, the group operates around 518 long day childcare centers across Australia and Singapore and is the largest for-profit operator in Australia. Besides this, the group reported a 1HFY18 result that was broadly in line with the management expectations along with encouraging occupancy trend level of transitions in July and August month. However, the management doesn’t expect improved conditions until mid-late CY19 because of certain challenges in the education sector such as stiff competition, salary hike, etc. On the financial front, the underlying EBIT decreased by 21.2% to $48.1 million in 1HFY18 due to higher Q1FY18 wage costs from regulatory changes to required staff ratios, though this is in line with market consensus. Wage ratios have returned to prior year levels by May, reflecting an improved wage outcome to be expected in the second half. The average like-for-like 1H FY18 occupancy was down by 250 bps to 70.1% in 1HFY18 over the prior corresponding period, however, the recent data reflects encouraging early signs of improvement, as July 2018 occupancy rose to 74.5%, representing 2.2% rise over June 2018. August occupancy growth is ahead of last year’s levels. Additionally, GEM expects the H1/H2 Earnings Before Interest and Tax (EBIT) split to be similar to prior years, being approximately 34: 66. In our view, there are certain challenges that persist in near term while in long run, the childcare operating conditions will improve at the back of new childcare subsidy, center closures, restricted developer financing.

Average Half-Yearly Occupancy Trend (Source: Company Reports)

Currently, the group focuses on its network growth strategy which is based on detailed network modelling supported by forecast supply/demand across the region, competitive environment and demographic profiling. Meanwhile, GEM is trading at a reasonable P/E of 12.08x. Lately, Legg Mason Asset Management Limited and related entities enhanced its interest in GEM to 6.84% from 5.59%. Based on the foregoing, we maintain our “Hold” recommendation on the stock at the current price of $ 2.00.

Think Childcare Limited

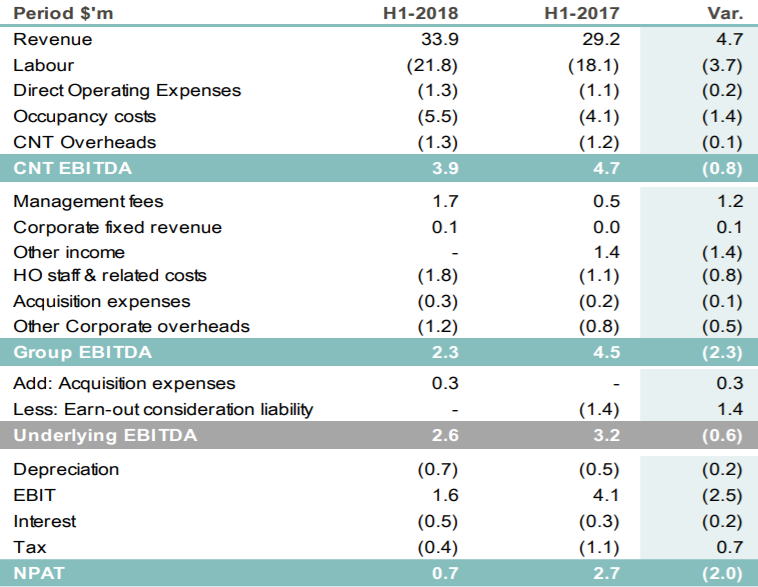

Decent Growth in Topline but Bottom line Disappointed: Think Childcare Limited (ASX: TNK) has recently released it 1HCY18 earnings report for the period ended 30 June 2018 wherein revenue grew by 4.7 per cent and amounted to $33.9 Mn against the prior year. It was mainly driven by full year impact of CY17 acquisitions; CY18 acquisitions and 1.2 Mn higher management fees during the same period. However, underlying EBITDA decreased by 0.6% to $2.6 Mn in 1HCY18 on Y-o-Y basis. It was mainly impacted by lower centre contribution of 0.8 million and higher overhead costs. NPAT was down 2.0% and recorded at $0.724 Mn as compared to the prior year. Basic EPS stood at 1.57 cent in 1H FY18. Moreover, cash and cash equivalent at the end of the first half was $ 3.89 Mn against $ 0.45 Mn of the previous corresponding period. Although, the management fees stood at 1.7 Mn in 1HCY18 from 0.5 Mn in 1HCY17, representing the strength of the forward pipeline of 26 centres under management, including 4 new centres opened and 9 DA secured in 1H18. Based on sectorial headwinds, the group has reaffirmed the full year 2018 guidance and expects Group EBITDA to be between $10 Mn and $11 Mn. The management informed the market that NPAT and EPS will be around in the range of $4.75 Mn- $5.25 Mn and 10 cps – 11cps, respectively for CY18 and the group maintains focus to improve balance sheet flexibility.

1HCY18 P&L Highlights (Source: Company Reports)

Meanwhile, the stock has generated negative YTD return of 41.18% and is hovering around its 52-week low. We believe that there is a lack of any positive catalyst at the current juncture which can boost the stock higher. By looking at its performance in 1HFY18 and current trading level, the stock can be avoided at the current market price of $1.30.

Mayfield Childcare Limited

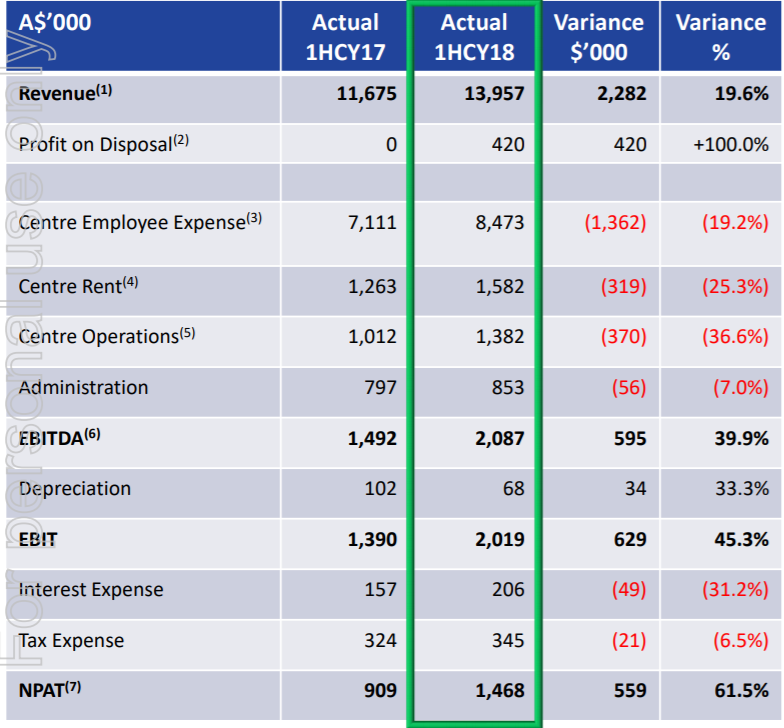

Decent Performance in 1H CY18: Mayfield Childcare Limited (ASX: MFD) has recently posted a decent set of 1HCY18 results in which revenue grew by 19.6 percent to $13.95 million as against $11.67 million in the last corresponding period. This strong growth has been achieved through the rise in childcare fees, stable occupancy, increased portfolio size, and kindergarten funding during the period. EBIT increased 45.3% to $2.01 million in 1HCY 18 as compared to the prior corresponding period (PCP). Resultantly, NPAT grew by 61.5 percent and amounted to $ 1.468 Mn in 1HFCY18 against PCP. EPS stood at 4.81 cents per share during the first half of the year. However, ROE and ROIC decreased by 490 bps and 380 bps to 6.1 percent and 4.4 percent, respectively in 1HCY18 from the previous six months. As expected, the first half of 2018 continued to experience the dual challenges of the diminishing value of the historical Child Care Rebate (CCR) which placed pressure on the affordability of childcare for families, along with market oversupply. Although, the government regulations and funding activities could play a key role in the growth perspective.

1HCY18 P&L Highlights (Source: Company Reports)

Meanwhile, the share price has fallen 14.01 percent in the past six months as at October 08, 2018 and traded close to 52-week low level. The Group is already trading at lower PE level of 6.75x among the peer group. The stock can be avoided as of now at the current market price of $0.890 and one can wait for the further developments and a suitable buying opportunity ahead. On October 9, 2018, the company had a market capitalization of $27.56 million.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...