.png)

Stocks’ Details

Insurance Australia Group Limited

Covid-19 Update: Insurance Australia Group Limited (ASX: IAG) is a parent company of a general insurance group with controlled operations in Australia and New Zealand. On 4 May 2020, the company provided a market update, wherein it informed that it presently has limited scope to pay a final dividend in September 2020. The company will determine the quantum of any final dividend in August 2020, after taking into account its FY20 financial performance.The company has advised that its financial performance in the last months of FY20 is subject to ongoing uncertainty from the impact of COVID-19 related challenges and surrounding economic conditions.

FY20 Performance Update: In the first half of FY20, the company saw strong underlying performance with GWP growth of 1.4% (like-for-like ~2.5%) and an underlying margin of 16.9%.For the nine months ended 31 March 2020, IAG’s underlying business performance has remained strong. At the end of April 2020, the company’s investment income on shareholders’ funds stood at a YTD loss of around $280 million pre-tax, impacted by the severe corrections witnessed in the H1FY20 in equity and credit markets.

.png)

Half-year Results Summary (Source: Company Reports)

FY20 guidance Retained: The company has retained its existing FY20 market guidance, of ‘low single digit’ gross written premium growth and a reported insurance margin of 12.5-14.5%, subject to any COVID-19 related challenge and surrounding economic conditions.

Valuation Methodology: Price to Earnings Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The company currently has a strong capital position with a Common Equity Tier 1 (CET1) ratio at the top end of its targeted range, of 0.9 to 1.1. In the last six months, the stock of IAG has declined by 31.24% on ASX and is currently trading near to its 52 weeks low price of $5.0. We have valued the stock using Price to earnings multiple based illustrative relative valuation method and arrived at a target price with limited upside in percentage terms. Considering the aforesaid facts and the uncertainty around the impact of COVID-19, we have a watch stance on the stock at the current market price of $5.490, up by 0.182% on 5 May 2020.

Westpac Banking Corporation

H1FY20 Results Highlights:Westpac Banking Corporation (ASX: WBC) is one of the leading banks in Australia, involved in providing banking, financial and related services to its clients. For the six months ended 31 March 2020, the company reported statutory net profit of $1,190 million and cash earnings of $993 million. The half-year results were impacted by the higher impairment charges due to COVID-19, as well as notable items including the AUSTRAC provision. During the period, the customer deposits grew faster than loans, causing the bank’s funding and liquidity to strengthen.

.png)

Half-year Results Summary (Source: Company Reports)

Tackling Challenging Environment:Due to the changed economic outlook, the bank has increased its provisions for expected credit losses to $5.8 billion and has provisioned $900 million for a potential penalty relating to the AUSTRAC civil proceedings. As part of its COVID-19 response, the bank has also deferred the decision on determining an interim dividend.

What to expect:The bank remains well capitalized. Its liquidity and funding metrics are also comfortably above regulatory requirements. Although, the bank expects the remainder of the year to be challenging, it is well placed to continue to support customers through this difficult time.

Valuation Methodology: Price to Book Value Based Relative Valuation (Illustrative)

.png)

Price to Book Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the past six months, the stock of WBC has declined by 41.96% and is trading near to its 52-week low of $13.470, offering a decent opportunity to investors for accumulation. The bank is currently well provisioned and capitalized to support customers through this difficult time. We have valued the stock using Price to Book multiple based illustrative relative valuation method and arrived at a target price with lower double-digit upside (in percentage terms). Considering the bank’s current liquidity and funding metrics, its recent measures to handle Covid-19 impacts, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $16.20, up by 2.727% on 5 May 2020.

Suncorp Group Limited

Decent H1FY20 Results:Suncorp Group Limited (ASX: SUN) is a leading financial services provider in Australia and New Zealand, involved in the provision of banking, insurance, wealth and other financial solutions to the retail, corporate and commercial sectors. For the half-year ended 31 December 2019, the company reported Group net profit after tax of $642 million, up 156.8% on the pcp. For the same period, the company reported cash earnings of $365 million and an interim ordinary dividend of 26 cents per share, fully franked. The half-year results reflect the early progress the company made in implementing the refocused strategy. During the period, the company saw strong GWP growth in New Zealand driven by the direct and partner channels.

.png)

Half-Year Results Summary (Source: Company Reports)

What to expect: In the second half, the company is focusing on improving the performance of its core businesses while driving operational excellence. In FY20, the Group reserve releases is expected to be above 1.5% of NEP and NIM is expected to remain within the operating range of 1.85% - 1.95%. The company’s regulatory project costs are expected to peak in FY20, with costs expected to gradually decline but remain elevated. In FY20, the company intends to maintain an ordinary dividend payout ratio policy of 60-80% of cash earnings, subject to ongoing uncertainty from the impact of COVID-19.

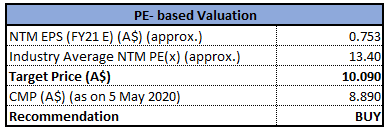

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock recommendation:The company currently has a strong balance sheet, providing capital flexibility. In the past six months, the stock has declined by 35.14% and is trading near to its 52 weeks low price of $7.3, offering a decent opportunity for accumulation. We have valued the stock using Price to earnings multiple based illustrative relative valuation method and arrived at a target price with lower double-digit upside (in % terms). Considering the aforesaid facts, the company’s decent performance in H1FY20, FY20 outlook, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $8.890, up by 2.894% on 5 May 2020.

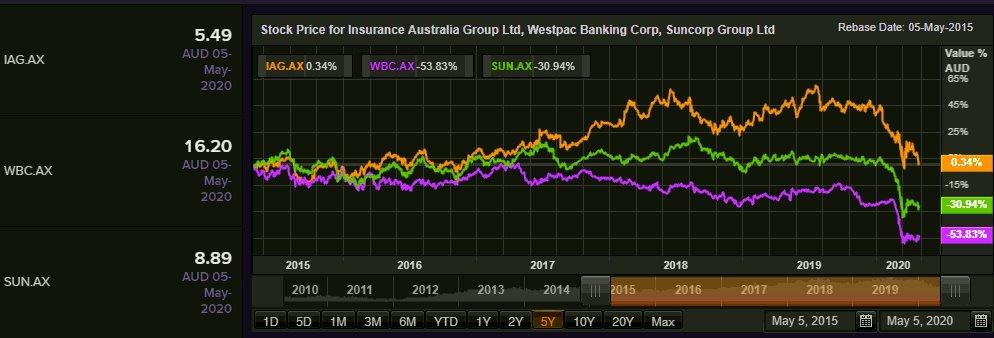

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...