Stocks’ Details

Treasury Wine Estates Limited

EBITS Growth Across All Regions:Treasury Wine Estates Limited (ASX: TWE) is primarily engaged in the production and sale of wine.The company recently declared a dividend amounting to AUD 0.2000 per ordinary share to be paid on 04 October 2019.

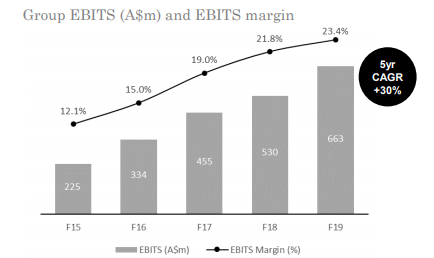

FY19 Financial Highlights: Net sales revenue for the year ended 30 June 2019 amounted to $2,831.6 million, up 17% in comparison to prior corresponding period value of $2,429 million. Earnings before interest, tax, SGARA and material items (EBITS) was reported at $662.7 million, up 25% on prior corresponding period. NPAT for the period stood at $419.5 million, up 16% on prior corresponding period. Earnings per share depicted an increase of 18% at 58.4 cents per share. FY19 cash conversion of 75.8% was ahead of the guidance range of 60% - 70%. Operating cashflow of the company went up by 36%.

Group EBITS & EBITDA Margin (Source: Company Reports)

Outlook & Guidance: The company is well-positioned to continue the successful execution of its premiumisation strategy over the future. The current investments in French production assets and Australian Luxury winemaking capacity will assist the next phase of the premiumisation journey.In FY20, the company is expecting EBITS growth in the range of 15% - 20%. Full year underlying cash conversion for FY20 is expected to be broadly in-line with FY19.

Stock Recommendation:Over a period of 6 months, the stock generated returns of 27.07%. In FY19, premiumisation was a key driver of performance, with net sales revenue growth of 27% from the Luxury and Masstige segments. Moreover, the company confirmed the acquisition of French production and vineyard assets in the Bordeaux region of France, that will support continuation of the premiumisation strategy. Return on capital employed increased by 14.9% on the back of enhanced profitability in all regions and disciplined capital allocation. Over a period of 5-year covering FY15 to FY19, the company reported EBITS CAGR growth of 30%. EBITS margin in FY19 was 23.4% as compared to 21.8% in pcp. In FY19, the company had a net margin of 14.6%, higher than the industry median of 8.2%. Considering the above factors, we give a “Hold” recommendation on the stock at the current market price of $18.240, down 4.752% on 24 September 2019.

Woolworths Group Limited

Robust Customer Scores in Q4:Woolworths Group Limited (ASX: WOW) is primarily engaged in the operation of supermarkets in Australia and New Zealand.The company recently notified that it will be paying a dividend amounting to AUD 0.5700 per ordinary share on 30 September 2019.

FY19 Results: During the 53 weeks ended 30 June 2019, the group generated sales from continuing operations amounting to $59,984 million, representing an increase of 3.4% on prior year. EBIT from continuing operations stood at $2,724 million, up 5.0% on prior corresponding period. NPAT from continuing operations was reported at $1,752 million, up 7.2% on prior year. The group reported FY19 dividend per share amounting to 102 cents, up 9.7% on the previous year.

FY19 Financial Highlights (Source: Company Reports)

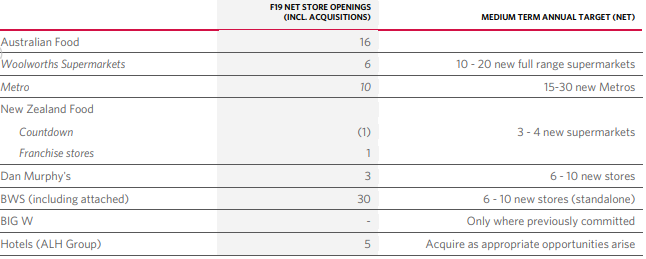

Outlook: In Australia Food, the company expects to deliver sales growth through more localised ranging and store renewals. The segment is expected to see a strong growth in online sales. As a medium-term annual target, the company is planning 3-4 new supermarkets for New Zealand Food. In addition, the company is progressing well on the merger of Endeavour Drinks and ALH Group.

New Store Rollout Plans (Source: Company Reports)

Stock Recommendation: At the current market price of $37.70, the stock is trading at a price to earnings multiple of 18.22x. Currently, the stock is trading close to its 52-week high and has gained ~35.88% over a period of 1 year. In FY19, the company reported robust customer scores, especially in Q4. Online sales of the group reported decent growth of 32%. The sales momentum of the group witnessed an improvement in the second half which will be carried forward in FY20. In addition, the company is planning to increase the roll out of metro stores along with strong online sales growth for Australian Food. BIG W saw material improvement in sales growth over the course of FY19 and will see a further reduction in losses in FY20. In FY19, the company had an EBITDA margin of 6.3%, higher than the industry median of 5.8%. Given the backdrop of the above factors, we give a “Hold” recommendation on the stock at the current market price of $37.700, up 0.346% on 24 September 2019.

Coles Group Limited

FY19 Witnessed a Strong Cash Realisation: Coles Group Limited (ASX: COL) is engaged in providing fresh food, groceries, general merchandise, liquor, fuel and financial services.The company recently notified about a Dividend Reinvestment Plan (DRP) for shareholders. If the shareholder opts to participate in the plan, they will have an option to reinvest either all or part of their dividend payments into additional fully paid Coles shares.

FY19 Results: During the year ended 30 June 2019, group sales revenue amounted to $35.0 billion, up 3.1% on prior corresponding period. Supermarkets EBITDA growth stood at 2.2%. The group generated online sales amounting to $1.1 billion, up 30% in comparison to prior corresponding period. Total fully franked dividend for the period stood at 35.5 cents per share, comprising a final dividend and a special dividend, to be paid on 26 September 2019.

FY19 Financial Results (Source: Company Reports)

Outlook: As per the trading update for Q1FY20, Little Shop 2 reported strong customer engagement. Growth in fuel volumes was encouraging in Express. However, building volumes to target levels still required more time. Smart selling initiative in FY20 are expected to deliver annualised benefits of over $150 million.

Stock Recommendation:The stock of the company generated returns of 29.30% over a period of 6 months. FY19 was a period of strong cash realisation of 110% and a robust balance sheet with an improvement in net debt position. This, in turn, provided significant flexibility for long-term growth. During the year, the company commenced a New Alliance Agreement with Viva Energy to restore fuel growth. Other strategic initiatives included an exclusive partnership with Ocado that brought in world’s leading online grocery website, two automated fulfilment facilities and home delivery solution to Australia. The company also partnered with Witron to develop two automated distribution centres.In FY19, the company had a net margin of 2.8%, which was higher than the net margin of 2.6% in pcp and the industry median of 2.0%. Today, the stock made a new 52-week high levels of $15.37. Hence, considering the above factors and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $15.370, up 2.467% on 24 September 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...