Stocks’ Details

Westpac Banking Corporation

Q3FY19 CET1 capital ratio at 10.5%: Westpac Banking Corporation (ASX: WBC) is involved in the provision of financial services, which include lending, accepting deposit, payments services, etc. The Bank also offers services such as investment portfolio management, superannuation and funds management, insurance, leasing finance, general finance, etc. On September 3, 2019, bank decreased its stake in Pendal Group Limited from 11.93% to 10.50%, effective from August 30, 2019. Other update includes Westpac Self-Funding Instalments over securities in ASX Limited, with a final dividend of $1.1430 and special dividend of $1.2910, taking the final amount to $2.4340 per security (fully franked), with record date and payment date on 6 September 2019 and on or about 25 September 2019, respectively. Westpac Self-Funding Instalments over securities in BHP Group Limited includes estimated dividend of $1.1499 per security (fully franked), with record date and payment date on 6 September 2019 and on or about 25 September 2019, respectively.

In July 2019, Fitch affirmed banks Long-Term Issuer Default Rating at AA- but revised the outlook to “Negative” from “Stable”. The change in outlook follows APRA’s announcement on 11th July 2019 that it was applying additional operational risk capital requirements on WBC, in response to the bank's self-assessment on governance, accountability and culture. The affirmation of WBC’s rating reflects Fitch's expectation that despite these challenges, the bank will maintain its strong company profile in the short term, which in turn, supports its sound financial profile. Separately, on July 9, 2019 S&P Global Ratings (S&P) affirmed the AA- long term and A-1+ short-term issuer credit ratings and revised its outlook for Westpac and the other major Australian banks to “Stable” from “Negative”. This outlook change reflects S&P’s view that the Australian Government remains highly supportive of Australia’s systemically important banks.

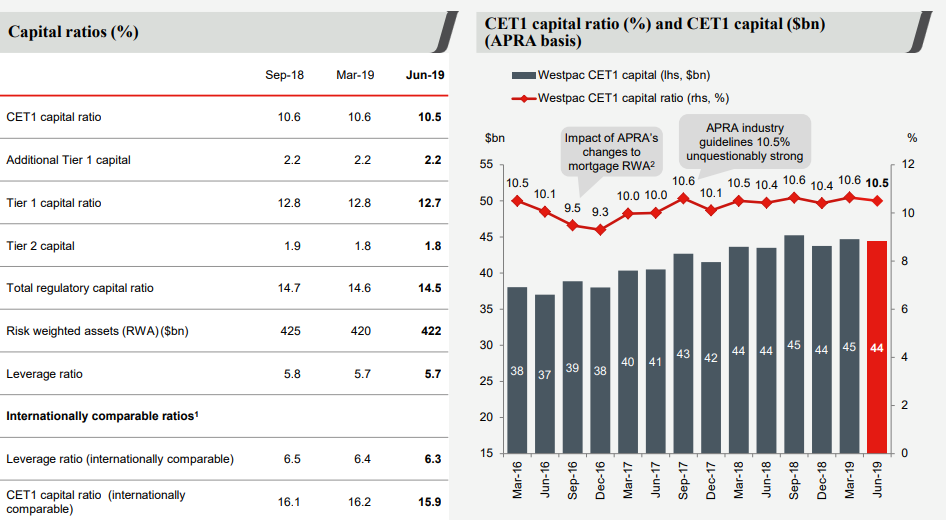

Q3FY19 Key Highlights: Common equity Tier 1 (CET1) capital ratio was reported at 10.5% on June 30, 2019.In terms of credit quality, there was a small increase in impaired assets over the quarter by $0.1bn to $1.9bn. Total provision balances increased by 1.8%, and the total provisions to gross loans were unchanged at 56 bps. Its Australian mortgage for ninety day plus delinquencies was reported at 0.9%, which was 8bps up over the quarter. Its average liquidity coverage ratio (LCR) was reported at 137%, net stable funding ratio was reported at 111%, both well above the regulatory requirements.

CET1 Capital Ratio Key Metrics (Source: Company Reports)

Stock Recommendation: WBC’s share generated a positive YTD return of 15.32%. Its efficiency ratio for H1FY19 stood at 51.9%, lower than the industry median of 60.5%. Currently, the stock is priced close to its 52-week high level of $29.110 with PE multiple of 13.70x. Hence, considering the aforesaid facts and current trading levels, we recommend a “Hold” rating on the stock at the current market price of $28.340, up 0.39% on September 03, 2019.

CSL Limited

Decent Top-line and Bottom-line growth in FY19: CSL Limited (ASX: CSL) is engaged in research, development, manufacture and distribution of biopharmaceutical and allied products. The company recently announced a change in director’s interest wherein, Robert Andrew Cuthbertson acquired 6,743 Ordinary Shares and disposed 6,743 Performance Rights (exercise) and 2,355 Performance Rights (lapse). After the change, the directors held 84,834 Ordinary Shares, 11,389 Performance Rights and 15,278 Performance Share Units, effective from August 27, 2019. Another director, Paul Perreault acquired 182,845 shares and disposed 147,911 options, 34,934 Performance Rights, 147,911 Ordinary Shares and 12,204 Performance Rights, effective from August 27, 2019.

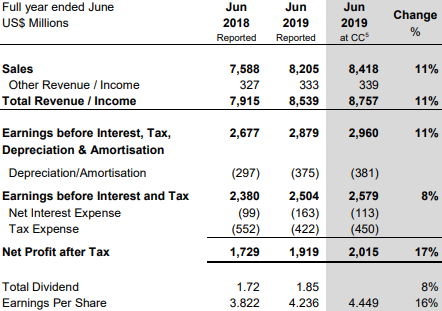

FY19 Key Highlights: Net profit after tax for the period was reported at US$1,919 million, up 17% at constant currency (CC). Total revenue for the period increased by 11% to US$8,757 million. This was due to the continued strong growth in immunoglobulin and albumin therapies, high patient demand for specialty products Haegarda & Kcentra, successful evolution of the haemophilia therapies portfolio and Seqirus delivering on strategy, with strong profit growth. The Board of Directors declared a final dividend of US$1.00 per share, taking the full year dividend to US$1.85 per share. The record date and payment date are on September 11, 2019 and October 11, 2019, respectively.

FY19 Income Statement (Source: Company Reports)

What to expect: FY20 net profit after tax is anticipated to be in the range of approximately $2,050 million to $2,110 million at CC, representing a growth of approximately 7-10% on FY19.This growth takes into account the one-off financial headwind of transitioning to a new model of direct distribution in China.

Demand for CSL’s plasma and recombinant products continue to be strong. It is expected that the company will again outpace the market in growing plasma collections and plan to open around 40 new collection centres in FY20.

Stock Recommendation: At the current market price of $240.030, the stock is trading close to its 52-week high level of $241.630. The stock has gained ~29.38% on YTD and is currently trading at a price to earnings multiple of 39.710x. Its gross margin and net margin for FY19 stood at 56.0% and 22.0%, better than the result in FY18 at 55.4% and 21.8%, respectively. Hence, considering the aforesaid facts and current trading levels, we recommend an “Expensive” rating on the stock at the current market price of $240.030, up 0.075% on September 03, 2019, and we suggest investors to wait for the better entry.

South32 Limited

FY19 net cash balance at US$504 Mn: South32 Limited (ASX: S32) is involved in the mining and metal production from a portfolio of assets including alumina, aluminium, bauxite, energy and metallurgical coal, manganese ore, manganese alloy, nickel, silver, lead and zinc. With the latest market update, the company informed that it bought back 329,564,533 shares for the total consideration of $1,032,753,527.

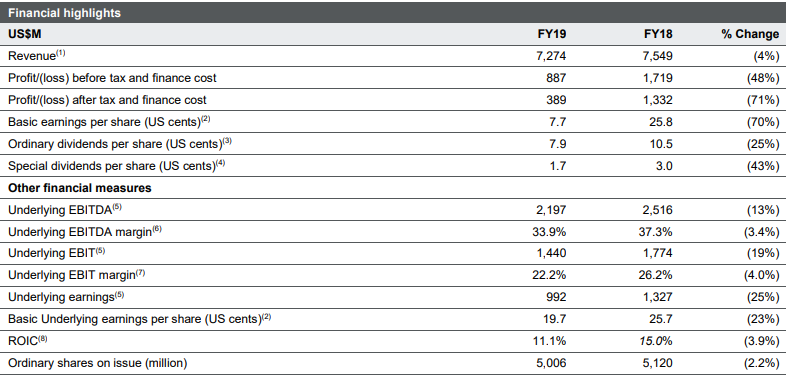

FY19 Key Highlights:The Group’s statutory profit after tax decreased by 71% to US$389 Mn in FY19 following the recognition of impairment charges totalling US$504 Mn (US$578 Mn post-tax, including de-recognition of deferred tax assets) in relation to South Africa Energy Coal operation. Underlying earnings decreased by 25% to US$992 Mn, which can be attributed to strong operating performance that delivered a 3% increase in Group production volumes, and cost reduction initiatives across labour, energy and materials usage were more than offset by lower aluminium and thermal coal prices. Basic underlying earnings per share decreased by a lesser 23% to US 19.7 cents per share as the company benefitted from the continuation of its on-market share buy-back program which has reduced its shares on issue by 6% since its commencement. The net cash balance at the end of the period was reported at US$504 Mn. The Board of Directors declared a fully franked final dividend of US 2.8 cents per share, with record date and payment date on September 13, 2019 and October 10, 2019, respectively.

FY19 Income Statement (Source: Company Reports)

What to expect: Group’s production volumes are expected to rise by a further 3% in FY20 with Illawarra Metallurgical Coal on-track to return to a three-longwall configuration during the June 2020 quarter and Worsley Alumina expected to achieve nameplate capacity following an improvement in calciner availability. Higher production volumes, weaker producer currencies and lower raw material input costs, along with the continuation of initiatives to mitigate inflation and maintain margins are expected to result in lower Operating unit costs for the majority of company’s operations in FY20.

Stock Recommendation: S32’s share generated a negative YTD return of 18.91%. It is currently trading close to its 52-week low level of $2.360. Current ratio for FY19 stood at 2.01x, better than the industry median of 1.71x, indicating company’s better position to address its short-term obligations. Its debt to equity for FY19 stood at 0.09x, lower than the industry median of 0.12x.Hence, considering the aforesaid facts and current trading levels, we recommend a “Hold” rating on the stock at the current market price of $2.700, up 2.273% on September 03, 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...