Scentre Group

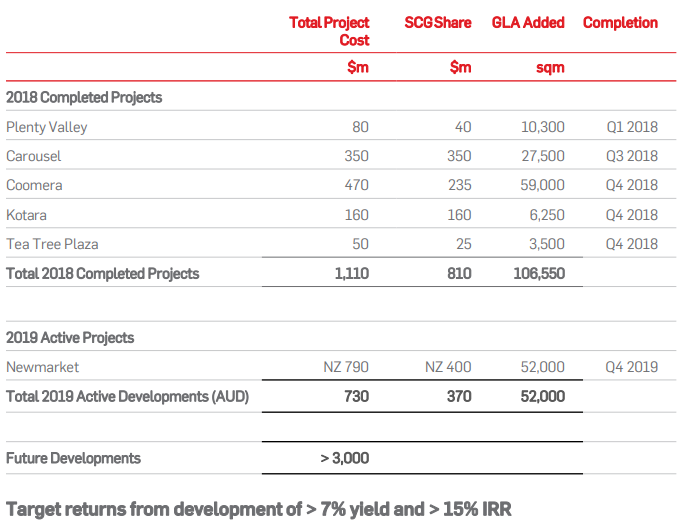

Undervalued at Current Juncture: Scentre Group (ASX: SCG) in its full-year result announcement reported an increase in its total income by 2.9% PCP to ~$2.0 Bn. It comprised net operating income of ~$1.9 Bn, management income of $46.1 Mn, and project income of $85.3 Mn. The uptick in income is due to an increase in annual customer visitation by 5 Mn to 535 Mn with an increase in annual in-store sales by $1 Bn to $24 Bn. The occupancy across its portfolio continued to be greater than 99% as it had been for 20 years. In its expansion and customer acquisition program during the year, it introduced 437 new brands and collaborated with 317 existing brands.

Its EBIT increased by 3.2% pcp to ~$1.94 Bn. Its funds from operations increased by 3.9% pcp to $1.34 Bn, representing 25.24 cents per security, and an increase in its distribution by 2% to 22.16 cents per security. Completion of developments, net income growth, and improvement in capitalization rates for high-quality assets helped the company to post a statutory profit of $2.3 Bn including revaluation uplifts of $1.1 Bn across the portfolio. Moreover, the company has around $54.2 Bn of assets under management with gearing of around 33.9% and interest cover at 3.5 times as on December 31, 2018.

Project Development Metrics (Source: Company Reports)

Further, the group expects ~3% growth in funds from operations for the full year 2019. It anticipates 2% growth in its distribution per security at 22.6 cents. It also expects growth of ~2.5% in its comparable net operating income (NOI) for the current year ending December 31, 2019. Moreover, BNP Paribas Nominees Pty Limited, a substantial holder of the group changed its holding from 6.57% of interest to 7.58% of the voting power.

Stock Recommendation: SCG’s share price generated positive YTD return of 2.86%. Its top-line and bottom-line has shown improvement over the previous year. Its operating margin for FY18 has been noted at 74.5% better than the industry median of 64.2%. The stock is currently trading at PE multiple of 9.16x as compared to the industry median of ~16.2x. These parameters reflect that SCG is undervalued, thus, providing an opportunity to invest at the current juncture. Hence, we uphold our “Buy” rating on the stock at the current market price of $3.95.

Commonwealth Bank of Australia

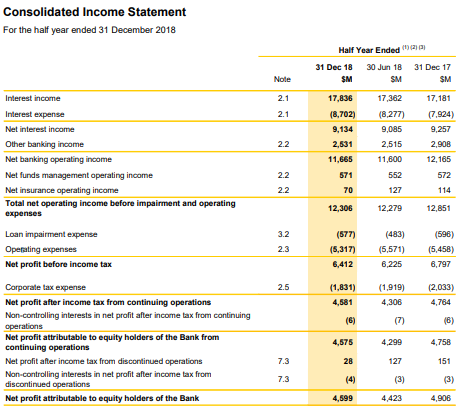

An update on CBA’s H1FY19 performance:Commonwealth Bank of Australia (ASX: CBA) has released its half-yearly report wherein it posted an increase in its interest income by ~3.81% pcp to $17.8 Bn. Its statutory net profit after tax including discontinued operations was reported at $4,599 Mn. Its cash NPAT from continuing operations increased by 1.7% to $4,676 Mn. Its operating income decreased by 1.9% to $12,408 Mn where the volume growth got offset by lower net interest margin, lower markets, fee income, and the impact of weather events. Its net interest margin was reported at 2.1% with 4 basis points (bps) lower than H2 FY18 due to higher funding costs, home loan switching, and competition. During the same period, the bank reported a decrease in its operating expenses by 3.1% to $5,289 Mn with elevated risk, compliance and remediation costs offset by prior period one-offs. Moreover, the credit quality of the bank’s lending portfolios remained sound with Loan Impairment Expense of $577 million in the first half of the year which equated 15 basis points of Gross Loans and Acceptances (GLAA) and down from 16 bps as compared to the prior corresponding period. Further, the Board of Directors declared an interim dividend of $2.00 per share with payment date on March 28, 2019 and record date on February 14, 2019. The Dividend Reinvestment Plan (DRP) is anticipated to be satisfied in full by an on-market purchase of shares.

Common Equity Tier 1 (CET1) capital ratio on an APRA basis increased to 10.8% from 10.1% as in June 2018.

Consolidate P&L Statement (Source: Company Reports)

Further, the bank expects the Australian economy to perform well with GDP growth over uptrend on population, wage growth, and employment. Since its listing on ASX, it has posted a return of 165.71%. Its top-line and bottom-line are in-line with the previous periods which indicates decent fundamentals amid sectorial challenges. Continuous improvement in the Australian economy will help the bank to post improved margin in the forthcoming year. Hence, we maintain our “Buy” recommendation on the stock at the current market price of $73.13.

Oil Search Limited

Update on Muruk 2 and Pikka B ST1 Drilling: Oil Search Limited (ASX: OSH) has recently released an update on Exploration and Appraisal Drilling report on Muruk 2 well for the February month. According to the release, 37.4 metres of core was cut in the objective Toro reservoir and the well was deepened to 3,820 metres. An extensive logging programme was conducted which has confirmed the presence of hydrocarbons. Moreover, the group has also given an update on Pikka B ST1 drilling wherein the Pikka B side track was drilled to a depth of 2,621 metres (8,599 feet), encountering the Nanushuk 3 sands. Further, 91 metres (300 feet) of cores were cut from the formation. The side-track core was oil saturated, like the initial Pikka B core, with high quality rock observed. Further, Flow-testing of the Pikka B ST1 well has begun. This will help to establish flow rates and other data, including the volume, thickness and quality of the Nanushuk reservoir at this location.

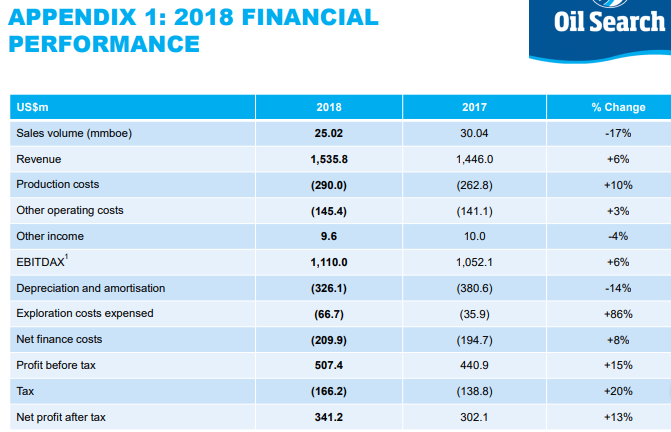

On the other hand, the company reported a healthy set of numbers despite the February earthquake. The company reported a drop in sales volume in 2018 coming in at 25.02 mmboe vs. 20.04 mmboe in 2017, a drop of 17% on a YoY basis. This was largely attributed to the drop in production due to the earthquake in February. However, the company reported a 6% growth in revenue, indicating an overall better realisation of its products. Revenue for 2018 came in at US$1,535.8 million vs. US$1,446.0 million in 2017. The net profit after tax for 2018 was US$341.2 million vs. US$302.1 million in 2017, reporting an increase of 13% on a YoY basis. The company reported a positive operating cash flow of US$1,015 million despite a plunge in sales volumes. A dividend of US$114 million was paid in 2018.

FY18 Financial Performance (Source: Company Reports)

The company has a strong production outlook for 2019, total production of 28.0-31.5 mmboe is guided for 2019. In the meantime, the share price of the company has risen 8.97% in the past three months and is trading below to the average of 52 weeks high and low level of ~$7.98. Since its listing on ASX, it has posted a return of 65.33%. The company’s gross margin is 58.7% vs. the industry mean of 53.2%. The company has guided for positive production guidance for 2019. Hence, we recommend a “Buy” rating on the stock at the current market price of $7.90.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...