DXC Technology Company

.png)

DXC Details

Global Infrastructure Services Grew 8.8% on pcp:DXC Technology Company (NASDAQ: DXC) is a cloud-based service provider of innovative Information Technology, optimizing data and provides security and scalability across to its users.

Q3FY20 Operating Highlights for the Period ended 31st December 2019: DXC came up with its quarterly results, wherein the company reported revenue of $5,021 million, down 3% on pcp. Global Business Services delivered a revenue growth of 8.8% while Global Infrastructure Services reported a decline in revenue of 11.5% on pcp. The company reported adjusted EBIT of $528 million, down 37.1% from Q3FY19. Adjusted EBIT margin stood at 10.5%, decline from 16.2% in prior corresponding period. The decline in the margin was associated unfavorable foreign currency exchange rate within the Global Infrastructure Services followed by decreases in the infrastructure businesses due to run -off from a few accounts. Profit margin from GBS, during the quarter stood at 15%, as compared to 18.2% in the prior year, due to investments across digital hiring followed by a slower pace of cost takeout.

.png)

Q3FY19 Income Statement Highlights (Source: Company Reports)

Valuation Methodology: EV/Sales Based Relative Valuation

.png)

EV/Salesbased relative valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of DXC closed at $23.73 with a market capitalization of $6.02 billion. The stock made a 52-week low and high of $22.89 and $67.62 and is currently trading at the lower band of its 52-week trading range. The stock corrected by 34.57% and 64.72% in the last three months and one year, respectively. The company has made several initiatives on running the business and unlocking value. DXC is executing on the focused strategy centered on the enterprise technology stack. Performance in the third quarter was a step to positioning DXC for long-term success. Considering the aforesaid facts, current trading levels, recent price movements and the company’s long-term vision, we have valued the stock using one relative valuation, i.e., Enterprise Value (EV) to Sales, and arrived at a target price of double-digit (in% terms). Hence, we recommend a ‘Buy’ rating on the stock at the closing price of $23.73, down 1.58% as on 02nd March 2020.

Lyft, Inc.

.png)

LYFT Details

Significant FY19 Revenue Growth Driven by Focused Execution: Lyft, Inc. (NASDAQ: LYFT) is one of the largest and fastest-growing transportation networks in the United States and Canada. The company recently released its fourth quarter results for FY19, which proved to be a record quarter with revenue of $1,017.1 million against $669.5 million in Q4FY18, representing a yoy growth of 52%. Adjusted net loss stood lower at $121.4 million as compared to a net loss of $238.5 million in Q4FY18. The quarter saw an 80% yoy growth in Contribution to $549.5 million with Contribution Margin at 54%. FY19 for the company was marked as an exception period as LYFT significantly improved its path to profitability and achieving critical milestones set towards long-term strategy. With this, FY19 revenue at $3.6 billion witnessed a robust yoy growth of 68% and lowered adjusted net loss of $651.8 million versus an adjusted net loss of $888.7 million in FY18.

.png)

Outlook: For FY 2020, the company estimates revenue to be in the range of $4,575 million - $4,650 million. Annual revenue growth rate is expected to come in the range of 27% - 29% with adjusted EBITDA loss to be between $450 million - $490 million.

Valuation Methodology: EV/Sales Based Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock witnessed a sharp correction amid the ongoing panic related to coronavirus and fell 13.19% and 22.26% in the last one week and one month, respectively. During FY19, top-line witnessed a healthy revenue growth, declined adjusted losses, and decent contribution margin. Considering the operational excellence, focused execution, robust transportation platform and outlook, we have valued the company using EV/Sales based relative valuation method and arrived at a target price with an upside of double-digit (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $36.91, down, 3.17% as on 02 March 2020.

Aramark

.png)

ARMK Details

Organic Revenue Grew by 1.6% on pcp terms: Aramark (NYSE: ARMK) is a food delivery company which serves premier educational institutions, Fortune 500 companies, world champion sports teams, prominent healthcare providers, iconic destinations and cultural attractions, and numerous municipalities in 19 countries around the world.

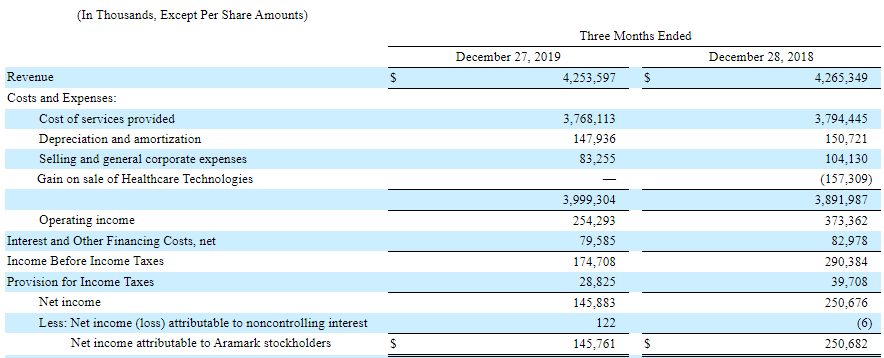

Q1FY20 Operational Highlights for the Period ended 27 December 2019: ARMK declared its quarterly results, wherein the company reported revenue of $4.3 billion, down 0.3% on pcp, mainly due to approximately six weeks of operations from the Healthcare Technologies business in Q1FY19 before its divestiture in November 2019. The company reported 1.6% growth in its organic revenue aided by positive performance across all the segment. FSS International reported a growth of 3.2%, aided by robust performance in South America, despite the impact of social unrest in Chile and the strategic exit of non-core custodial accounts in Europe in previous year. Operating income stood at $254.3 million, down 32% on pcp, primarily due to the divestiture of the Healthcare Technologies segment. The company reported net income of $145.461 million, as compared to $250.682 million in Q1FY19.

Key Income Statement Highlights (Source: Company Reports)

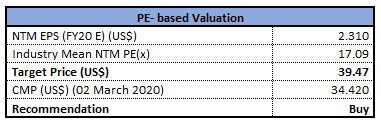

Valuation Methodology: Price to Earnings Based Relative Valuation

Price to Earnings based relative valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of ARMK closed at $34.42 with a market capitalization of $8.68 billion. The stock made a 52-week low and high of $25.49 and $47.22 and is currently trading at the lower band of its 52-week trading range.The stock has corrected 22.02% and 19.27% in the last one month and three-months, respectively. The performance in the latest quarter was mostly materialized as expected and reflects the early actions of the strategies to unlock the economic potential of the business. Considering the aforesaid facts, current trading levels, recent price movements and the company’s long-term vision, we have valued the stock using price to earnings based relative valuation and arrived at a target price of lower double-digit (in% terms). Hence, we recommend a ‘Buy’ rating on the stock at the closing price of $34.42, down 0.92% as on 02nd March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...