Stocks’ Details

Commonwealth Bank of Australia

Announcement About Completion of Count Financial Divestment: Commonwealth Bank of Australia (ASX: CBA) has recently made an announcement that sale of Count Financial Limited to the ASX-listed CountPlus Limited has been wrapped up. The transaction happens to be a significant milestone in CBA’s decision to exit the aligned advice businesses. CBA is committed to continuing to support and manage the customer remediation matters arising from the past issues at Count Financial. Commonwealth Bank of Australia would be providing an indemnity to CountPlus of $200 million and all the claims under indemnity needs to be notified to CBA within the span of 4 years.

Issue Of Subordinated Notes: Commonwealth Bank of Australia (ASX: CBA) has recently announced that it will issue AUD 100 million worth of subordinated notes. Further, it stated that the AUD 100 million 3.66% subordinated notes which are due 2034 has been issued pursuant to CBA’s U.S. $70,000,000,000 Euro Medium Term Note Programme. The issue of the subordinated notes by CBA would not be having a material impact on the financial position of CBA. CBA has earlier confirmed that it has issued U.S.$2.5 billion worth of the subordinated notes. The US $1.25 billion 3.610% subordinated notes which are due 2034 and U.S.$1.25 billion 3.743% subordinated notes which are due 2039 were issued pursuant to the CBA’s U.S. $50,000,000,000 Senior and Subordinated Medium Term Notes Program.

Announcement of Update on Australian life insurance business’ Divestment: CBA has recently made an announcement that it has entered into further agreements to progress planned divestment of the Australian life insurance business (CommInsure Life) to AIA (or AIA Group Limited). Further, it stated that the revised transaction path comprises the joint co-operation agreement, reinsurance arrangements, partnership milestone payments and statutory asset transfer. The aggregate proceeds for CBA have been anticipated to be $2,375 million, which reflects the reduction of $150 million from the original sale price. Upon the completion, which is anticipated to occur by FY 2020 end, revised transaction path is expected to have released around $1.6 billion – $1.8 billion of the CET1 capital, resulting in the pro forma increase to CBA’s CET1 ratio of around 35 – 40 bps on APRA basis as at June 30, 2019.

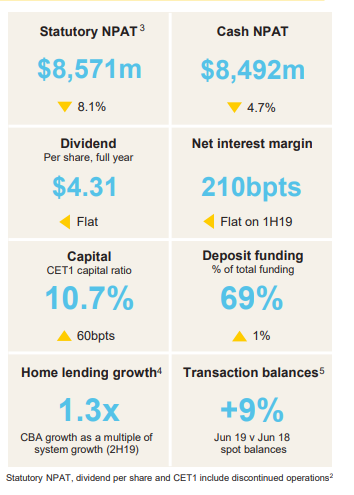

Maintenance of Dividend: In FY19 (year ended June 30, 2019) results announcement, the bank stated that its balance sheet has remained the key strength. The deposits have provided 69% of CBA’s total funding, its Common Equity Tier 1 capital ratio is above the APRA’s ‘unquestionably strong’ benchmark, as well as they have maintained the dividend. The following picture provides the key metrics:

Key Metrics (Source: Company Reports)

Stock Recommendation: As per the ASX, the bank’s annual dividend yield stands at 5.3%, and the stock price is trading towards the 52-week higher levels of $83.99. In the span of previous 3 months, the stock has fallen by 1.26% while, in the time span of one month, it rose by 2.96%. Since the price of the stock is trading towards the higher end, we advise the investors to closely watch the stock at the current market price of A$79.600 per share (down 2.067% on 2 October 2019) and wait for better entry levels.

Westpac Banking Corporation

A Look at Key Updates: The Chief Executive Officer (CEO) of Westpac Banking Corporation (ASX: WBC) named Mr Brian Hartzer recently made an announcement that Peter King, Chief Financial Officer, has decided to retire in 2020 after 25-year career with Westpac. Mr Hartzer stated that Westpac had benefited from Peter’s deep financial services knowledge and understanding of all the aspects of the business.

Westpac Banking Corporation has recently acknowledged that ASIC has filed an appeal with Full Federal Court with respect to the proceedings against WBC regarding the responsible lending obligations. The appeal which was filed by ASIC was related to a decision handed down by Federal Court in the month of August this year, in which Honourable Justice Nye Perram found in favour of WBC and dismissed proceedings of the ASIC with costs.

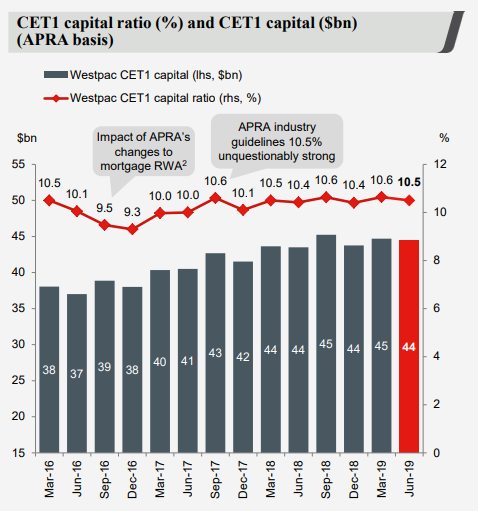

Overview of Q3 FY 2019 Capital, Funding And Credit Quality: The bank’s common equity tier 1 (or CET1) capital ratio stood at 10.5% as at June 30, 2019 a fall from 10.6% as at March 31, 2019 because of payment of 2019 interim dividend partially offset by organic capital generation and DRP participation. The bank stated that there has been a small increase in impaired assets over the quarter (i.e., a rise of $0.1 billion to $1.9 billion). The bank’s Q3 FY 2019 average liquidity coverage ratio (or LCR) stood at 137%, and net stable funding ratio (or NSFR) was 111% and both of these are well above the regulatory minimums.

CET 1 Capital Ratio (Source: Company Reports)

Priorities for 2019: The bank has earlier stated that it has been maintaining focus towards the 2019 priorities, which includes dealing with outstanding issues, momentum in the customer franchise and structural cost reduction.

Stock Recommendation: The annual dividend yield of WBC, as per ASX, stood at 6.33% and the stock price of WBC is trading closer to its 52-week higher levels of $30.05. Additionally, it stated that the bank is well provisioned, and its credit quality is in the sound position. Hence considering the above-stated factors and current trading levels, we give a “Hold” recommendation on the stock at the current price of A$29.210 per share (down 1.65% on 2 October 2019).

National Australia Bank Limited

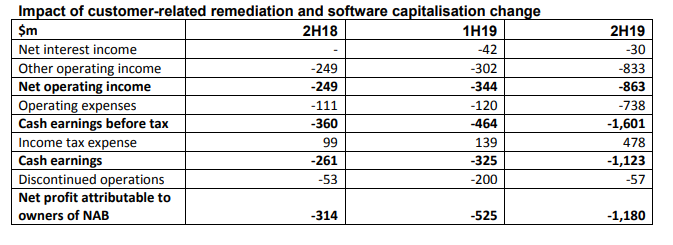

Announcement of Additional Costs for Remediation and Software: National Australia Bank Ltd (ASX: NAB) has made an announcement with regards to additional charges amounting to $1,180 million after tax ($1,683 million before tax) related to the increased provisions for customer-related remediation as well as change to the application of software capitalisation policy. This is anticipated to reduce 2H FY 2019 cash earnings by estimated $1,123 million after tax while the earnings from discontinued operations by an estimated $57 million after tax.

The 2H FY19 result would be including charges amounting to $832 million after tax ($1,189 million before tax) for the additional customer-related remediation. Following the review of NAB’s software capitalisation policies, minimum threshold at which software is to be capitalised rose from $0.5 million to $2 million, which implies NAB’s focus towards the simplification as well as increasingly shorter useful life of the smaller software items.

Impact of customer-related remediation and software capitalisation change (Source: Company Reports)

Announcement of the start date for Ross McEwan: National Australia Bank has recently stated that Ross McEwan would be starting with the bank as the group Chief Executive Officer (or CEO) and Managing Director on December 2, 2019. This follows an announcement of his appointment on July 19, 2019, at which time NAB has advised that Mr McEwan’s start date was dependent on him fulfilling the obligations as the CEO of RBS or (Royal Bank of Scotland). RBS has recently made an announcement that Mr McEwan would be stepping down as the CEO on October 31, 2019, following an appointment of Alison Rose as the new CEO of RBS.

Commencement of civil proceedings against NAB: NAB has recently released a release stating that ASIC has commenced the civil proceedings against it in relation to NAB Introducer Program. In the release, it was mentioned that the ASIC’s civil proceedings against NAB allege contraventions of section 31 of the National Consumer Credit Protection Act in relation to 297 loan applications between the span of 2013 and 2016. NAB’s chief legal and commercial counsel named Sharon Cook stated that they take this legal action seriously and would be carefully assessing the allegations.

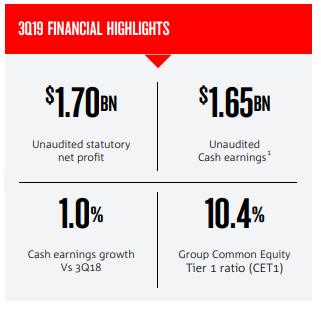

Financial Highlights of 3Q FY 2019 (June 30, 2019): In Q3FY19 trading update, the bank stated that, against the backdrop of a challenging operating environment, which includes subdued home lending growth, its Q3 FY19 performance as compared to 1H FY19 quarterly average was solid. The following image provides the financial highlights for Q3 FY19:

Financial Highlights (Source: Company Reports)

What to Expect from NAB: In the half-year results presentation, the bank stated that it is re-orienting its culture towards action. Also, the productivity benefits would remain the key driver of the underlying profit growth. The bank added that the capital settings give greater flexibility in order to accommodate the potential earnings volatility as well as regulatory change.

Stock Recommendation: The market capitalisation of NAB stood at ~A$85.63 billion as on 2 October 2019 and its annual dividend yield stands at 6.13%. As per ASX, the stock of NAB is trading closer to its 52-week higher levels of $30.0 with P/E multiple of 14.48x. Hence, considering the above-stated factors and current trading levels, we give a “Hold” recommendation on the stock at the current price of A$29.020 per share (down 2.29% on October 2, 2019).

.JPG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...