Westpac Banking Corporation

WBC Reports Board Changes: Westpac Banking Corporation (ASX: WBC) provides a broad range of banking and financial services in Australia. It is also one of the largest banks in New Zealand. Recently, the bank declared a dividend of $0.3400 per security, in respect of underlying securities of Aristocrat Leisure Limited. The bank also announced that Brian Hartzer has to step down from the CEO’s post on December 2, 2019 after exit from the current fiscal year. Notably, Peter King, will take over the position and will also join its board members.

FY19 Results for the Year Ended 30 September 2019:The bank declared its results for FY19, wherein net interest income came in at $7,942 million as compared to $7,850 million in FY18. Net profit came in at $6,784 Mn, down 16% y-o-y. The result was impacted by a challenging regulatory environment, customer remediation costs and decline in wealth management business. Earnings per share came in at 198.2 cents, down 16% y-o-y. The company reduced the fully franked final dividend for FY19 to 80 cents per share, down 15% from 94 cents in FY18. In percentage terms, net interest margin in FY19 stood at 2.12% as compared to 2.13% in the previous year. The company’s operating expenses increased 6% y-o-y to $10,106 Mn in FY19.

.png)

Interest Spread and Margin (Source: Company Reports)

Guidance for FY20: Operating expenses in FY20 are expected to rise by ~$245 Mn, which will include costs related to risk management, compliance, financial crime and complaints management. Productivity for the year is expected to be ~$500 million, up 23% in comparison to FY19. Moreover, exit of financial planning business along with Wealth reset is expected to reduce FY20 expenses by ~$200 million.

Stock Recommendation: As per the ASX, the stock is trading on the lower band of its 52-week trading range of $23.300 - $30.050, with PE multiple of 12.44x and an annual dividend yield of 7.12%. It has a market cap of $87.22 Bn. The stock witnessed a fall of 11.51% in the past 3 months. It has a net interest margin of 2.16%, higher than the industry average of 1.94%. Taking into consideration the growth in net interest income and FY20 productivity targets, we recommend a “Buy” rating on the stock at the current market price of $24.860, up 1.718% on November 26, 2019.

Bank of Queensland Limited

Bank of Queensland completes $250 Mn Institutional Placement: Bank of Queensland (ASX: BOQ) provides financial services including lending, deposit taking, investment platforms and other financial services in Australia. The bank will issue approximately 32.1 million fully paid ordinary shares at a price of $7.78 per share, under a fully underwritten $250 Mn institutional share placement. The bank also notified regarding a fully franked dividend of $0.3100 per security, which is to be paid on or around November 27, 2019.

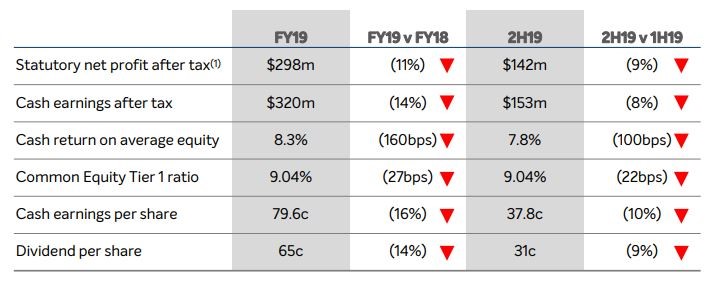

Financial Highlights: During the year ended 31 August 2019, the bank reported a final dividend of 65 cents per share, representing a payout ratio of 82%. Both reported net profit and cash EPS of the company went down by 11% and 16%, to $298 Mn and 79.6 cents, respectively, reflecting the challenging economic environment.

FY19 Performance Highlights (Source: Company Reports)

Guidance for FY20:The bank expects lower cash earnings on y-o-y basis for FY20. The company also anticipates an increase in costs, mainly due to regulatory compliance and higher technology investment.

Stock Recommendation:The stock witnessed a fall of 4.42% in the past 3 months. Currently, the stock is trading close to its 52-week low level of $7.850. The bank has increased Australian customer base and has an efficiency ratio of 55.8%, higher than the industry average of 52.3%. Going forward, the bank will focus on delivering sustainable shareholder returns on the back of strong capital position and sound underlying asset quality. Taking into consideration the above factors, we recommend a “Buy” rating on the stock at the current market price of $8.140, down 5.787% on November 26, 2019.

National Australia Bank Limited

CET1 Ratio up by 18 BPS:National Australia Bank Limited(ASX: NAB) operates in the banking sector and has a market capitalisation of $75.19 billion as at 26 November 2019. The bank recently updated that David Hugh ARMSTRONG, Director on the Board, disposed 900 convertible preference shares for a total consideration of $91,638.

Financial Performance:During the year ended 30 September 2019, cash earnings per share came in at 177 cents, down 12.5% y-o-y. Cash RoE for FY19 came in at 9.9%, down 180 bps y-o-y. FY19 full year dividend stood at 166 cents per share, down 16.2% from FY18. On 12 December 2019, the bank will pay a fully franked final dividend of 83 cents per share. Net interest margin in FY19 stood at 1.78%, down 7 bps from the previous year. The company’s operating expenses increased by 0.4% y-o-y to $8,155 Mn in FY19. Statutory net profit for the year stood at $4,798 million, down 13.6% on pcp.

.png)

FY19 Financial Highlights (Source: Company Reports)

Stock Recommendation:Over a span of 1 month and 3 months, the stock generated negative returns of 10.62% and 3.62%, respectively. In FY19, CET1 (Common Equity Tier 1) ratio of the bank went up by 18 bps. CET1 capital ratio was impacted by dividend reinvestment plan and impact from regulatory changes. The bank has an efficiency ratio of 57.2%, higher than the industry median of 52.3%. Considering the backdrop of the above factors, we recommend a “Hold” rating on the stock at the current market price of $26.150, up 0.268% on November 26, 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...