Stocks’ Details

Commonwealth Bank of Australia

Trading at Higher levels: Commonwealth Bank of Australia (ASX: CBA) provides integrated financial services, life insurance, general insurance, broking services, funds management, etc. The Bank recently updated the exchange that it has been ceased to be a substantial shareholder for Otto Energy Limited.

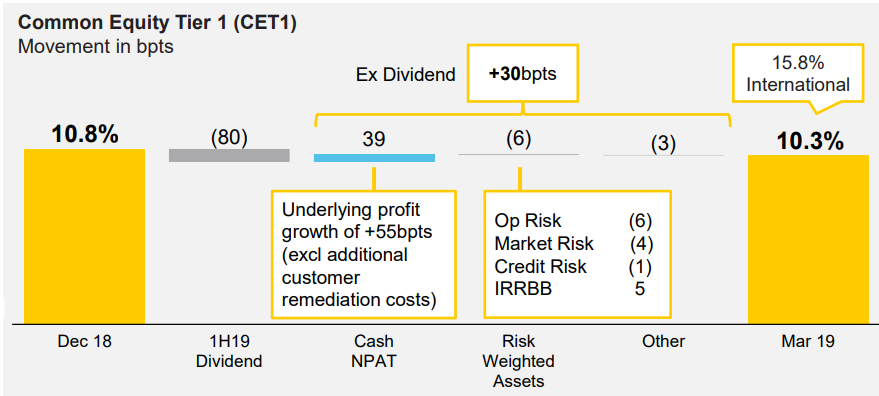

Financial Performance in 3QFY19:Net interest income (NII) witnessed a fall of 3% owing to the impact of two fewer days in the quarter. On a day-weighted basis, Net Interest Income (NII) remained flat. During the period, the unaudited statutory net profit amounted to $1.75 billion with cash net profit of approximately $1.70 billion. The profit was impacted by $714 million in pre-tax additional customer remediation provisions. Operating income during the period was down by 4% due to a combination of factors, including seasonal impacts, unfavourable derivative valuation adjustment, and weather events and rebase fee income driven by the Bank’s Better Customer Outcomes Program. Capital and balance sheet position remained strong, with the Common Equity Tier 1 (capital) ratio at 10.3%. The credit quality remained sound with loan impairment expense of $314 million in the 3QFY19. The company witnessed a sustained volume growth in core markets.

CET1 (Source: Company Reports)

The Bank’s leverage ratio on an APRA basis, stood at 5.4% as at 31 March 2019 and 6.2% on an internationally comparable basis.

Leverage Ratio (Source: Company Reports)

Stock Recommendation:Q3FY19 saw the profit being impacted by additional customer remediation provisions. The company’s net interest margin reduced from 2.16% in HY18 to 2.10% in HY19. Also, the company’s CET1 ratio was 10.3% as compared to APRA’s requirement of 10.5% for Australian banks. The performance was also characterised by few favourable factors including sustained volume growth and better credit quality. However, we believe that the effect of the above positive factors is priced in at the current level. The stock price is trading close to 52-week high value of $82.30 and generated returns of 5.23% and 13.42% over a period of 1 month and 3 months, respectively. Hence, considering the above factors and current trading level, we give a “Sell” recommendation on the stock at the current market price of $82.300 (up 1.044% on 19 June 2019) and we advise to investors that they can book the profit at the current level.

Australia and New Zealand Banking Group Limited

CET1 Ratio of 11.5%:Australia and New Zealand Banking Group Limited (ASX: ANZ) engages in the provision of banking and financial products and services to individual and business customers across 34 markets. On 18 June 2019, the company made an announcement regarding the issue of USD 1,000,000,000 6.750% Fixed Rate Resetting Perpetual Subordinated Contingent Convertible Securities. On 17 June 2019, the company made another announcement on leadership changes. Antonia Watsun was appointed as Acting CEO after the resignation of David Hisco.

The bank recently sold OnePath Life, its Australian life insurance business, to Zurich Financial Services Australia. Original announcement for the sale was made in December 2017. As a part of the agreement, Zurich Financial will provide ANZ customers with life insurance products for 20 years.

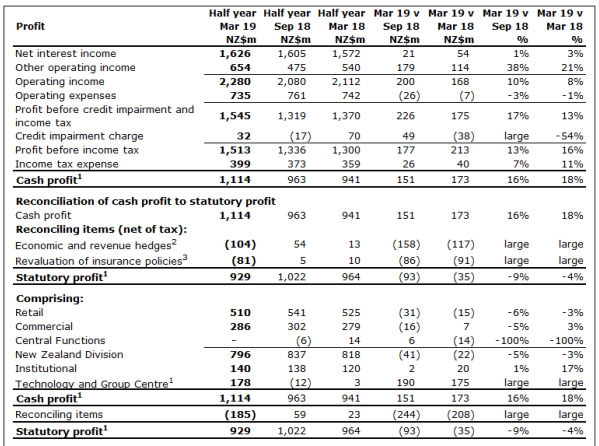

Financial Highlights:For the six months ended 31 March 2019, the bank reported a statutory net profit after taxation amounting to NZ$ 929 million, down 4% on prior corresponding period. Cash NPAT for the period stood at NZ$1,114 million, reporting an increase of 18% on prior corresponding period. Revenue for the period went up by 8% on pcp. Capital and Balance Sheet position remained strong with CET1 ratio of 11.5%. The period also saw the launch of a Healthy Home Loan Package having discounts of standard home loan rates for customers who choose to build or upgrade their homes to sustainable standards.

Key Financial Information (Source: Company Reports)

Stock Recommendation:The stock of the company yielded returns of 1.51% and 7.08% over a period of 1 month and 3 months, respectively. The overall performance during the first half of FY19 was characterised by a rise in the revenue and cash NPAT on pcp, and the CET1 ratio above APRA’s requirement of 10.5%. The period was also characterised by low levels of credit losses and improved credit quality. Hence, we give a “Hold” rating to the stock at a current market price of $28.670 (up 1.379% on 19 June 2019).

National Australia Bank Limited

Decent Outlook:National Australia Bank Limited (ASX: NAB) is engaged in providing banking services, credit and access card facilities, leasing, housing, general finance, international banking, investment banking, and wealth management services, etc. On 17 June 2019, the company announced about the distribution payment of A$0.802900 with total dividend distribution rate of 3.1853 % per annum for NABPB - CNV PREF 3-BBSW+3.25% PERP NON-CUM RED T-12-20 and it will be paid on September 17, 2019 with the record date of September 02, 2019 and ex-date of August 30, 2019.It made another announcement on the same day for distribution payment of AUD 0.9352 with total dividend distribution rate of 3.7103 % per annum for NABPF - CAP NOTE 3-BBSW+4.00% PERP NON-CUM RED T-06-26. It will be payable on September 17, 2019 with record date of September 09, 2019.

During 1HFY19 (ending March 2019), the company posted a 7.1% increase in the reported cash earnings in comparison to pcp, which totalled to $2,954 million. Net operating income increased from $9,093 million in H1FY18 to $9,218 million in H1FY19. Underlying profit during the period amounted to $5,163 million, up 1.2% on pcp profit of $5,104 million.Cash ROE during the period was 11.7% as compared to the previous cash ROE of 11.4%. Operating expenses for the company increased by 1.7% to $4,055 million in 1H19. NAB’s CET1 (APRA) ratio for 1H19 was 10.4%.

.png)

Key Financial Metrics (Source: Company Reports)

Outlook:Due to the modest GDP growth, the company foresees a challenging operating environment. Other factors include low growth in housing credit, house price decline, significant regulatory changes, higher customer and community expectations, etc. These factors may pose challenges for NAB and industry as a whole. The company plans to reorient its culture to adapt to the above conditions. Despite that, productivity benefits and greater flexibility through capital settings to accommodate potential earnings volatility will help in increasing profitability over the period.

Stock Recommendation: The stock generated positive returns of 3.53% and 6.37% over a period of 1 month and 3 months, respectively. It has a market capitalisation of ~$75.12 billion. During 1HFY19, the company witnessed positive growth in all the key fundamentals including revenue, profit, and income. Also, the company is well positioned to cope up with upcoming challenges and is likely to grow at a decent pace in the future. Hence, we recommend a “Buy” rating on the stock at the current market price of $26.830 per share (up 0.412% on 19 June 2019).

.png)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...