.png)

Stocks’ Details

Xref Limited

Strategic Alliance for ANZ Region: Xref Limited (ASX: XF1) is an online, automated solution, which delivers data-driven candidate insights, customer-centric platform and team, offering the flexibility and scalability that clients need to hire the best talent. As on 27th December 2019, the market capitalization of the company stood at $68.55 million. CVCheck Limited and Xref Limited announced a strategic alliance, where the users of Xref platform will be able to add multiple products from CVCheck to their verification process, while Xref’s reference checks will be made available to all CV Check users.

Continued Growth Trajectory throughout Q1 FY20: XF1 managed to achieve record credit usage and cash receipts in Q1 FY20. As compared to Q1 FY19, the sales rose 23% to $2.46 million, while the credit usage increased 32% to $2.24 million. The record sales during Q419 resulted in strong cash receipts of $3.53 million in Q1 FY 2020, a rise of 31% from $2.7 million in the previous corresponding quarter. During Q1 FY 2020, credit usage by integrated customers was $0.5 million, representing a 67% increase on Q1 FY19. Net cash outflow for the quarter stood at $1.946 million as compared to $1.519 million in Q4 FY19. Xref Limited has recently announced that it has received commitments from institutional and professional investors to garner $3,476,000 before costs via placement of 10,533,333 fully-paid ordinary shares.

.png)

Credit Sales and Usage (Source: Company Reports)

Stock Recommendation: As per ASX, the stock gave a return of 2.67% in the last one month and is trading towards its 52-week low of $0.310, proffering a decent opportunity for accumulation.In the time span of 3 years from FY16 to FY19, the company witnessed a CAGR of 82.24% in revenue and has witnessed an improvement in EBITDA margin in the same time span. During the FY19, current ratio stood at 1.31x, up from 1.22x in FY18 and is in a decent position to leverage opportunities globally and at scale. Considering the returns, trading levels, high revenue CAGR and improvement in margins, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.360, down by 6.494% on December 27, 2019.

ELMO Software Limited

Investment in Software Development House: ELMO Software Limited (ASX: ELO) is one of Australia and New Zealand’s leading providers of software-as-a-service, cloud-based human resources and payroll solutions. As on 27th December 2019, the market capitalization of the company stood at $460.82 million. The company has recently announced an investment of $1.18 million in exchange for 50% equity ownership in Hero Brands Pty Limited, providing ELMO with increased Research and Development capability. In the recently held Annual General Meeting, the top management stated that FY19 annualised recurring revenue (ARR) went up by 47.8% on YoY basis to $46 million with a gross margin of 86.6%.

.png)

Financial Performance (Source: Company Reports)

Growth Opportunities: The company has a positive outlook for organic growth across the business. ELO has confirmed its FY20 guidance and expects its ARR to be between $61 million to $63 million. It also anticipates that its EBITDA to come in the range of -$1 million to -$3 million.The company expects larger market opportunities, primarily with more multi-module sales with broadened product set and is deploying towards sustainable growth.

Valuation Methodology: EV/Sales Based Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of ELO gave a return of 12.43% on a YTD basis. In the time span of 4 years from FY15 to FY19, the company witnessed a CAGR of 41.79% in revenue and 41.17% in gross profit. On the backdrop of decent returns, CAGR in revenue and gross profit, coupled with modest outlook, we have valued the stock using EV/Sales based relative valuation approach and arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $6.150 as on 27 December 2019.

Japara Healthcare Limited

Development Program Progressing Well: Japara Healthcare Limited (ASX: JHC) is Australia’s leading aged care provider and owns, operates and develops residential aged care homes. As on December 27, 2019, the market capitalisation of JHC stood at A$257.89 million. Through its staged development program, the company expects to deliver more than 1,100 net new places to the market by the end of FY2022.The company has been positioning its business around the continuum of care model, which is expected to result in further growth in its senior living business. In FY19, under its development program, the company has completed four new homes, including its 50th and newest home in Robina, Queensland.

Director’s Interest Notice:On 17th December 2019, the company’s director Richard England acquired 4,038 fully paid ordinary shares of the company at $4,038 via on-market trade under Japara Healthcare Limited Non-Executive Directors Share Purchase Plan.

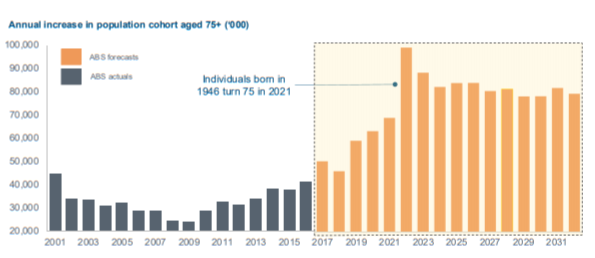

Positive Sector Outlook: It has been observed in Australia that people are living longer, and there has been a significant increase in births in the post-war era.The below-mentioned figure demonstrates the annual increase in the population of Australians aged 75 plus.

Future demand for aged care places (Source: Company Reports)

FY19 Results Highlights: For the year ended 30th June 2019 (FY19), the company reported total revenue of $399.8 million, up 7% on last year. The company reported net profit after tax of $16.4 million.The company paid a final dividend of 3.35 cents per share (franked to 50%), taking total dividends for FY2019 to 6.15 cents per share, representing the dividend payout of 100% compared with 88% last year. The payout ratio of 100% in FY19 reflected a non-cash gain on the acquisition of the Riviera Health portfolio of $9.6 million. JHC has also announced that it will release its 31st December 2019 half-year financial results on 28th February 2020.

What to Expect From JHC:The company expects its FY20 EBITDA to be 5%-10% lesser than FY19, mainly due to the removal of the Government’s temporary subsidy increase that applied from 20 March 2019 to 30 June 2019, low occupancy and challenges in the funding environment. Further, the company’s recently completed developments are expected to mitigate industry headwinds.

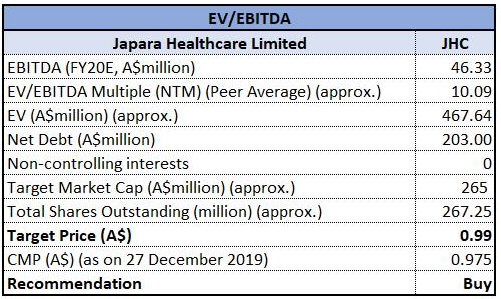

Valuation Methodology: EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock is currently trading near to its 52-week low. We have valued the stock using EV to EBITDA multiple approach and arrived at a target price with an upside of lower single-digit (in percentage terms). Considering the decent sector outlook, current trading levels, company’s progress with the development program and valuation, we give a “Buy” recommendation on the stock at the current market price of A$0.975 per share, up 1.036% on December 27, 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...