Stocks’ Details

Treasury Wine Estates Limited

TWE Confident on Re-building Momentum in the US: Treasury Wine Estates Limited (ASX: TWE) is engaged in the production, marketing and distribution of wine. The company also engages in growing and sourcing grapes. The company recently updated that the voting power of The Capital Group Companies, Inc. was reduced to 6.0116%, from 7.578% earlier.

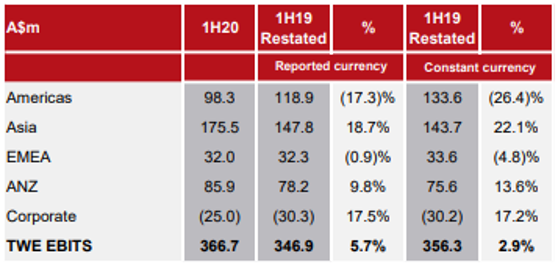

1H20 Update: During the half-year ended 31st December 2019, the company reported net profit after tax amounting to $229.2 million, up 5% on pcp. Earnings per share stood at 31.9 cents, up 5% on pcp. EBITS for the period reported a growth of 2.9% on pcp. The company performed decently across the Asian, ANZ and EMEA regions, driven by growth across the Luxury and Masstige business. However, the company underperformed in the US due to a set of reasons, including changes in TWE’s Americas leadership and US wine market dynamics that included suppliers providing surplus wine at lower prices. Therefore, the company expects FY20 and FY21 profits to grow at a slightly lower rate than previously expected and is drafting a plan to rebuild the momentum and bring the business back on track.

1HFY20 EBITDA (Source: Company Reports)

Outlook:The company is currently reviewing its internal operating model which focuses on driving returns through premiumisation and efficiently managing the Commercial wine business, which is expected to add benefits to business performance. The review is anticipated to wind up in the second half of FY20, with details to be announced no later than FY20 full-year results. In FY20, the company now expects EBITS to grow in the range of 5% - 10%, as compared to the previous guidance of 15% - 20%, due to challenging conditions in the US. As the situation stabilises, the company expects FY21 EBITS to grow by 10% - 15%.

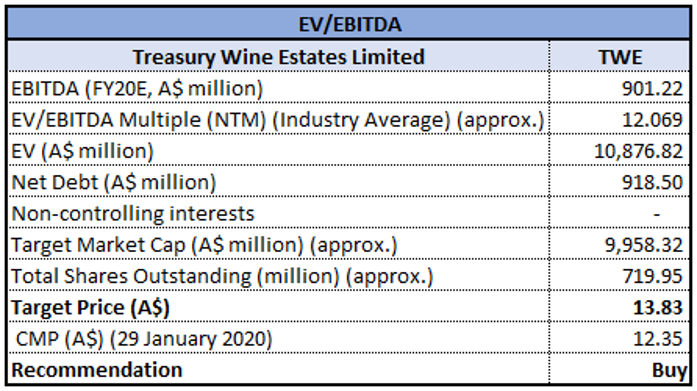

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated returns of 7.96% over a period of 1 year. The company’s performance in 1HFY20 has been supported by the continued momentum on the back of its premiumisation strategy and a diversified business model. As described above, the company has performed strongly in a few markets and expects to deliver continued benefits, going forward. Despite the challenging environment in the US, it is confident on re-gaining momentum and returns to growth. We have valued the stock using EV/EBITDA based relative valuation method and arrived at a target price offering an upside of lower double-digit (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $12.350, down 25.959% on 29th January 2020, taking cues from the revised guidance for FY20.

oOh! Media Limited

Improved Bookings from Sep’19 – Dec’19:oOh! Media Limited (ASX: OML) is a leading media company providing advertising solutions across Australia and New Zealand. The company recently announced that Brendon Cook will be stepping down from the position of Managing Director & CEO after the completion of a global executive search and ensuring a smooth transition to a new CEO.

Revised FY19 Guidance: Underlying EBITDA for the year ended 31st December 2019 is expected to be between $138 million - $143 million. The above guidance excludes integration costs and the impact of change in accounting standards. As per the previously issued guidance, underlying EBITDA was expected in the range of $125 million - $135 million. Operational expenditure for the year is expected to witness growth in the range of 5%-7%. FY19 capital expenditure is expected to be between $55 million - $70 million, precisely at the mid to lower end of the guidance. The revised guidance for FY19 came in as a result of improved advertising bookings for September and the last quarter of FY19.

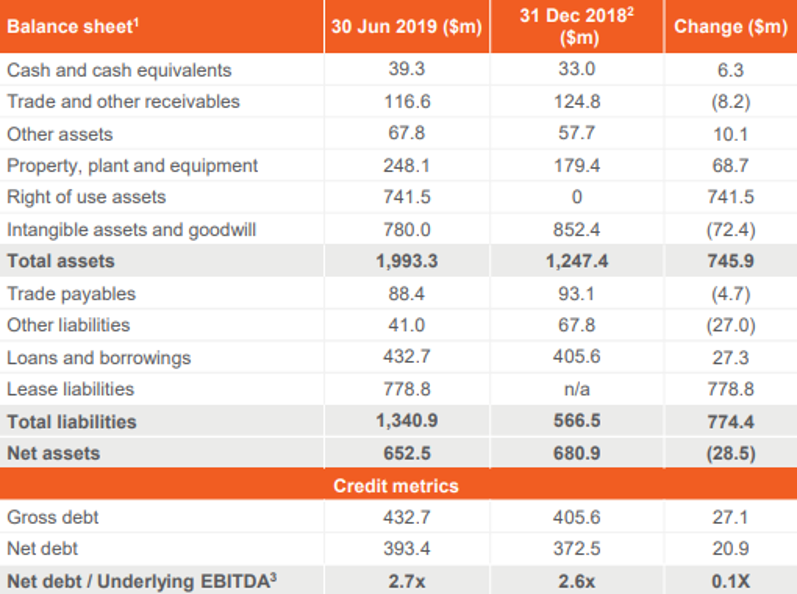

During the half year ended 30th June 2019, the company reported a sound balance sheet position and expects a reduction in debt in the second half on the back of strong positive cash flows.

1HFY19 Balance Sheet (Source: Company Reports)

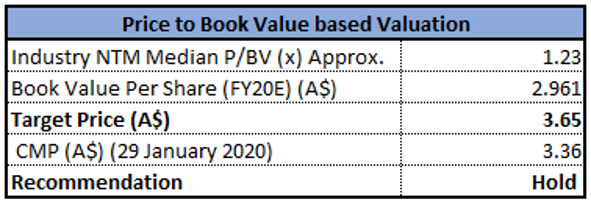

Valuation Methodology: Price to Book Multiple Approach

Price to Book Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated returns of 42.29% over a period of 3 months. The company has revised FY19 guidance as a result of improved bookings and continues to target a leverage ratio below or approaching 2 times in 2020. FY19 full-year results are expected to be released on 24th February 2020. We have valued the stock using the P/B based relative valuation method and arrived at a target price offering an upside of higher single-digit (in % terms). Considering the above factors, we give a “Hold” recommendation on the stock at the current market price of $3.360, down 6.667% on 29th January 2020, possibly due to the announcement regarding the resignation of MD & CEO.

Clearview Wealth Limited

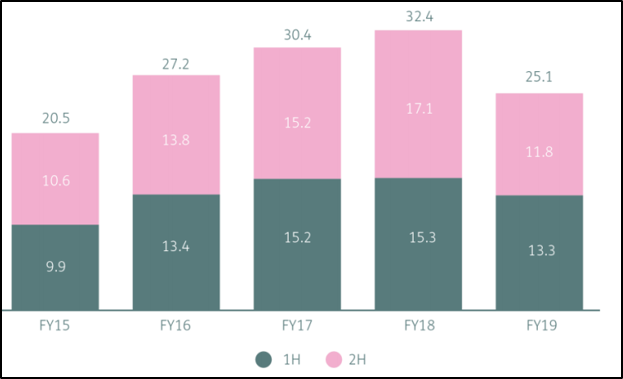

Challenging Period for the Life Insurance Segment:Clearview Wealth Limited (ASX: CVW) is engaged in providing services in the areas of Life Insurance, Wealth Management, Financial Advice, etc.

Update on 1HFY20 Results: The company recently updated the investors on the results for the half year ended 31st December 2019, which are in the process of being finalised. As per the update, underlying NPAT for the half amounted to $10.2 million as compared to $13.3 million in pcp. Reported NPAT for the period came in at $9.8 million. The Life Insurance segment was adversely impacted by deterioration in claims and higher than expected lapses. Underlying NPAT for the half came in at $8.7 million. The Wealth Management segment reported an underlying NPAT amounting to $1.7 million and witnessed strong net inflows of $66 million. Underlying NPAT for the financial advice segment came in at $0.6 million.

Underlying NPAT for FY15 – FY19 (Source: Company Reports)

Stock Recommendation: The stock of the company gave a negative YTD return of 47.19% over a period of 1 year. During 1HFY20, the company reported poor lapse and Income Protection (IP) claims due to poor wages growth, IP product design issues, rising consumer costs, etc. As a corrective measure, the company is conducting a detailed review of the claim assumptions, along with the repricing of the product to be implemented in 2HFY20. Revised claim assumptions are expected to have an adverse impact on the reported incurred claims reserves and depict a potential impact of $2 million to $3 million on 2HFY20 underlying NPAT after tax. Considering the backdrop of the above factors, we have a watch stance on the stock at the current market price of $0.450, down 4.255% on 29th January 2020.

Comparative Daily Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...