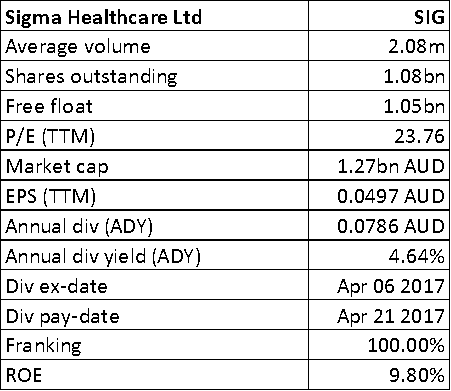

Sigma Healthcare Ltd

SIG Details

· Crash on issues relating to supply agreement with My Chemist/Chemist Warehouse Group: Sigma Healthcare Ltd (ASX: SIG) tumbled 31% on May 24, 2017, over the unfavorable discussions and outcome with regards to its current supply agreement with My Chemist/Chemist Warehouse Group. The supply agreement which was expected to run through to June 2019, was rejected by MC/CW and the latter now intends to acquire certain products from an alternate Wholesaler. As a result, Sigma now aims to defend the move and has decided to commence legal proceedings against MC/CW. Importantly, the impact on Sigma’s EBIT is expected to be ~$5m - $10m per annum, which is 5% below FY16/17 EBIT, if MC/CW acts in accordance with the specified intention. This will also be impacted by the ongoing legal costs.

· Recommendation: Given the ongoing developments and uncertainty over the supply arrangement with My Chemist/Chemist Warehouse Group coupled with subdued business scenario, we maintain an “Expensive” recommendation on the stock at the current price of $ 0.81

G8 Education Ltd

.png)

GEM Details

· Successfully completed $100m Institutional placement:G8 Education Ltd (ASX: GEM) witnessed a stock price slip of 1.5% on May 24, 2017 while the group completed the fully underwritten institutional placement to raise $100 million as announced on May 23, 2017. The Institutional Placement was priced at $3.20 per share, representing a 7.2% discount to the closing price of $3.45 per share before the trading halt and the top end of the bookbuild price range ($3.10 to $3.20). A total of 31.25 million new shares will be issued under the Institutional Placement, representing approximately 7.7% of G8’s existing share capital prior to the Institutional Placement. The purpose of the Institutional Placement is to reduce debt, strengthen the balance sheet and to ensure that G8 can execute on its $200 million acquisition pipeline as previously announced. G8’s trading performance for the 4 months to April 30, 2017 has been in line with estimated underlying EBIT for FY2017 of around mid to high $170 million. However, on a rolling 12-month basis, G8's like?for?like occupancy as at the end of April was down by 3.4% yoy to 77.7%, due to industry supply increases, weaker demand in select markets and select center?specific issues. The impact of lower occupancy has been offset by price increases as well as strong cost control which, through active management, resulted in an improvement in underlying EBIT and EBIT margin. The group is also undertaking initiatives to drive momentum going forward.

· Recommendation: We give a “Hold” recommendation on the stock at the current price of $ 3.40

.png)

Share Placement Detail (Source: Company Reports)

Surfstitch Group Ltd

.png)

SRF Details

· Confirms receival of statement of claim on behalf of plaintiffs:Surfstitch Group Ltd (ASX: SRF) has entered into a trading halt until commencement of normal trading on May 26, 2017 or release of an announcement to the market. SRF has now confirmed the receipt of a statement of claim on behalf of representative plaintiffs and members of a group, following the several press articles indicating that a class action against the company has been filed with the Supreme Court of Queensland.Currently, the company is considering the claim and a further update will be provided to the market shortly. All in all, the group seems to be witnessing strong headwinds and it will be crucial to watch out for the developments.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...