.png)

Stocks’ Details

Breville Group Limited

1HFY20 Revenues Increased by 25.4% Year over Year: Breville Group Limited (ASX: BRG) is engaged in developing and designing innovative world-class small electrical kitchen appliances. The market capitalisation of the company stood at $2.61 Bn as on 13th February 2020.

1HFY20 Key Highlights for the Period Ended 31st December 2019: Revenue for the period increased by 25.4% to $552 Mn, on the back of robust growth across all geographic segments and categories. EBIT increased by 17.1% to $73 Mn. EBITDA for the period stood at $85.2 Mn, up 20.8% year over year. NPAT for the period increased by 14.1% to $49.7 Mn. The increase was primarily on the back of adoption of AASB 16 in FY20. An interim dividend of 20.5 cents per share (60% franked) has been declared, as compared to 18.50 cents, 60% franked in the year-ago period. ROE improved as a result of robust returns on investment in organic growth. EPS for the period increased 14% to 38.1 cents. Net debt at the end of the period was reported at $52.9 Mn, as compared to net cash of $0.4 Mn in the year-ago period.

.png)

1HFY20 Key Metrics (Source: Company Reports)

What to expect: Despite the dynamic nature of the current global economic and political environment, the company remains encouraged by the continuous progress of the acceleration program. Further, the company expects EBIT for FY20 to be stable with the markets’ current consensus estimate of ~$110 Mn (pre AASB 16 basis). Moreover, the company expects to spend more on marketing and R&D as a percent of net sales. Furthermore, the group plans to penetrate more into Spain and enter France in 2HFY20, further leveraging the already established European warehousing, logistics, customer service and back office functions.

Valuation Methodology:P/BV Based Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: BRG’s share generated a positive one-year return of 70.62%. Its gross margin, EBITDA margin and net margin for FY19 stood at 35.7%, 14.9% and 8.9%, better than the industry median of 28.3%, 7.7% and 4.1%, respectively, implying decent fundamentals for the company. Its ROE for FY19 stood at 22.7%, better than the industry median of 18.4%. Its current ratio for FY19 stood at 2.57x, better than the industry median of 1.15x. The stock is currently trading close to its 52-week high of $26.180. We have valued the stock using P/BV based relative valuation method, and for the said purpose, we have considered peers like City Chic Collective Ltd (ASX: CCX), FlexiGroup Ltd (ASX: FXL) and Lovisa Holdings Ltd (ASX: LOV), to name few. Therefore, we have arrived at a target price offering limited upside (in percentage terms). Hence, considering the aforesaid facts and one-year appreciation in the stock price, we have a watch stance on the stock at the current market price of $25.50, up 27.628% on 13th February 2020, on the back of robust 1HFY20 top-line and bottom-line growth.

Skycity Entertainment Group Limited

NPAT Up a Whopping 296% Year Over Year: Skycity Entertainment Group Limited (ASX: SKC) is engaged in the gaming entertainment business. The market capitalisation of the company stood at $2.3 Bn as on 13th February 2020. Recently, the company announced that it will distribute a dividend of $0.11764706 per share on the security, SKC - ORDINARY FULLY PAID FOREIGN EXEMPT NZX,with an ex-date of February 27, 2020 and payment date of March 13, 2020.

1HFY20 Key Highlights for the Period Ended 31st December 2019: During the period, the company’s reported revenue from continuing operations amounted to NZ$721.7 million, up 75.4% on prior corresponding period. Reported net profit after tax for the period stood at NZ$328 million, up 296% on prior corresponding period. Reported EBITDA for the period stood at NZ$407.5 million, up 174.7% on prior corresponding period. Normalised revenue (including revenue including gaming GST) for the period went down by 7.7% to NZ$490.9 million. Normalised total net profit was reported at NZ$75 million, down 16.4% on prior corresponding period. The company paid a fully imputed interim dividend of 10.0 cents per share to the shareholders.

.png)

Results Summary (Source: Company Reports)

Valuation Methodology:P/E Based Valuation Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

FY20 Guidance:Corporate costs for the period are expected to be ~NZ$38 million. Due to a challenging environment, the company expects group normalised EBITDA to be slightly below NZ$300 million and group normalised NPAT to be ~NZ$130 million.

Stock Recommendation: SKC’s gross margin, EBITDA margin and net margin FY19 stood at 92.5%, 35.3% and 20%, better than the industry median of 55.8%, 25.6% and 9.4%, respectively, implying decent fundamentals for the company. The company has a well-defined growth strategy to improve its operating performance and drive further growth. It has invested in new products and is focused on reducing the cost pressure. Its strategies also revolve around optimising the current portfolio and reducing the amount of debt in the balance sheet. We have valued the stock using P/E based relative valuation method and have arrived at a target price with an upside of lower double-digit (in percentage terms). Thus, considering the performance in the first half, strategic initiatives, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $3.53 per share, up 2.319% on 13th February 2020.

Synlait Milk Limited

Long-term Initiatives & Focus on Customer satisfaction are Key Catalysts: Synlait Milk Limited (ASX: SM1) is a dairy manufacturer, which focuses on supplying higher value dairy products to leading milk-based health and nutrition companies. Recently, the company informed the market that 33,666 Performance Share Rights have lapsed as of 31st January 2020.

SM1 Updates FY20 Outlook: On 13th February 2020, the company provided an update for its FY20 guidance. The company now predicts FY20 earnings to be in the range of $70 million and $85 million net profit after tax. As per the previous guidance the company expected profits to grow in FY20, with the similar rate to FY19 over FY18. However, current outlook now suggests this rate of growth will not be achieved partly due to lower than expected infant base powder sales and lactoferrin prices being more volatile. For FY19, revenues exceeded $1 billion, representing an increase of 17% year over year.

.png)

FY19 Sales (Source: Company Reports)

HY20 Outlook for the Period Ended 31 January 2020: The company expects NPAT to be in the range of $26.5 million to $28.5 million for HY20, as compared to $37.3 million NPAT reported in HY19. SM1’s HY20 view will be impacted by higher incremental interest, increased SG&A costs associated with the Pokeno and advanced liquid dairy packaging facilities, lower sales volumes and lower sales of infant base powders due to the China infant nutrition market consolidation.

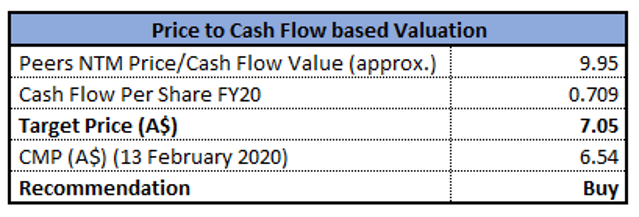

Valuation Methodology:P/CF Based Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock of SM1 is trading close to its 52-week low of $6.410, proffering a decent opportunity for accumulation. The company is focusing on commissioning the long-life dairy beverages line, with relevant export license and shelf life testing underway. Synlait continues to invest in long-term strategic opportunities and remains on track to develop and offer new opportunities to existing and prospective customers. We have valued the stock using P/CF based relative valuation method, and for the said purpose, we have considered peers like A2 Milk Company Ltd (ASX: A2M), Metcash Ltd (ASX: MTS) and Graincorp Ltd (ASX: GNC), to name few. Therefore, we have arrived at a target price with an upside of higher single-digit (in percentage terms). Thus, considering the current trading levels and long-term strategy, we give a “Buy” recommendation on the stock at the current market price of $6.54 per share, down 18.758% on 13th February 2020, on the back of recent FY20 and HY20 outlook update.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...