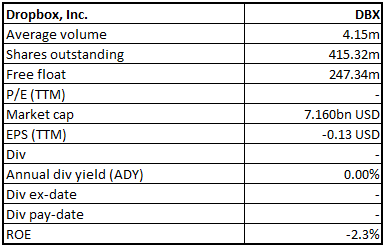

Dropbox, Inc.

DBX Details

New Product Launch to Aid Customer Additions:Dropbox, Inc. (NASDAQ: DBX) provides a cloud-based smart workspace that helps users to access their folders and files. The company has more than 600 million registered users across 180 countries.

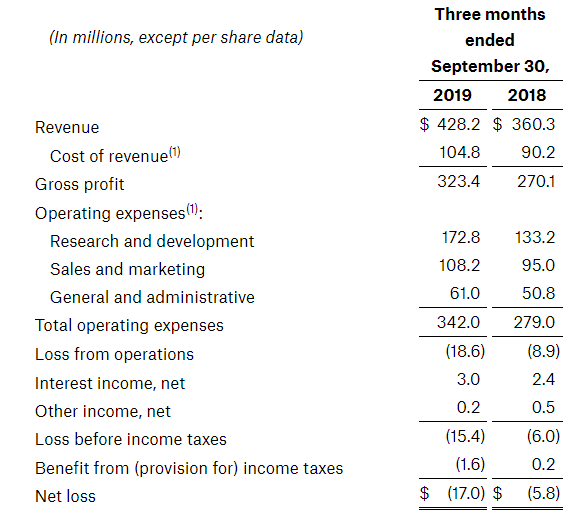

Q3FY19 Financial Highlights for the period ending 30 September 2019: DBX declared its quarterly results wherein, the company reported total revenue at $428.2 million, up 19% on y-o-y basis. The company reported a net loss of $17 million as compared to a loss of $5.8 million in the previous corresponding period. Paying users totaled 14.0 million, as compared to 12.3 million for the same period last year.Average revenue per paying user stood at $123.15, as compared to $118.60 for the previous corresponding period. Gross margin stood at 75.5%, improving marginally from 75% in Q3FY18. Research and development expenses came in at $172.8 million, representing 40.4% of the total revenue. During the quarter, DBX launched Dropbox Spaces used for building the world’s first smart workspace.

Q3 FY19 Income Statement Highlights (Source: Company Reports)

Guidance:As per the Q4FY19 guidance, the company expects revenue within the range of $442 million to $444 million with an operating margin (Non-GAAP) of 14% to 15%. As per the FY19 guidance, the company expects revenue at $1,657 million to $1,659 million along with a Non-GAAP operating margin at ~12%. The company expects free cash flow within the range of $375 million - $385 million followed and capital expenditure in the range of $65 million - $75 million.

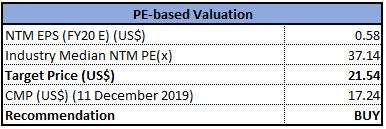

Valuation Methodology: Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of DBX closed at $17.24 with a market capitalization of $7.160 billion. The stock has generated positive returns of 15.16% and 25.14% in the last three-months and six months, respectively. The popularity of the platform led to significant growth, which has allowed the company to scale rapidly and efficiently. Currently, DBX is building a thriving global business with 14 million paying users. The stock is quoting at the lower band of its 52-week trading range of $17.20 to $26.49. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., PE Multiple and arrived at a target price of double-digit upside (in % terms). Hence, we give a ‘Buy’ rating on the stock at the closing price of $17.24, down 3.2% as on 11 December 2019.

DBX Daily Technical Chart (Source: Thomson Reuters)

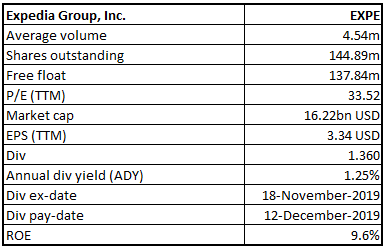

Expedia Group, Inc.

EXPE Details

Delivered Better than Industry Growth: Expedia Group, Inc. (NASDAQ: EXPE) is a leading travel service provider. Recently, the company announced the resignation of Mark Okerstrom as CEO and a member of the Board of Directors and CFO Alan Pickerill joined the above post. The company also announced a new share repurchase authorization for up to an additional 20 million shares of the Company’s common stock.

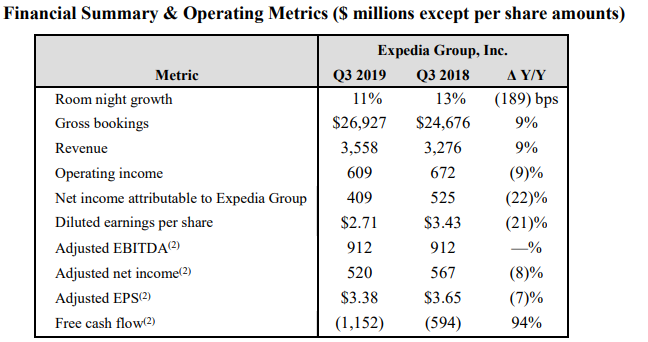

Q3FY19 Highlights for the period ended 30 September 2019: EXPE announced its quarterly results wherein, the company reported revenue of $3,368 million, up 9% on y-o-y basis. EXPE’s net income declined 22% on y-o-y basis to $409 million during Q3FY19. The company reported gross bookings at $26.9 billion, up 9% on y-o-y basis, driven by growth in Expedia Partner Solutions, which includes the benefit from enterprise deals launched in late 2018, and Hotels.com. On YTD, EXPE repurchased 3.2 million shares for $418 million. Expedia Group exceeded 1.4 million properties available on its core lodging platform as of September 30, 2019, including over 650,000 integrated Vrbo listings.

Q3FY19 Key Metrics (Source: Company Reports)

Valuation Methodology:Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

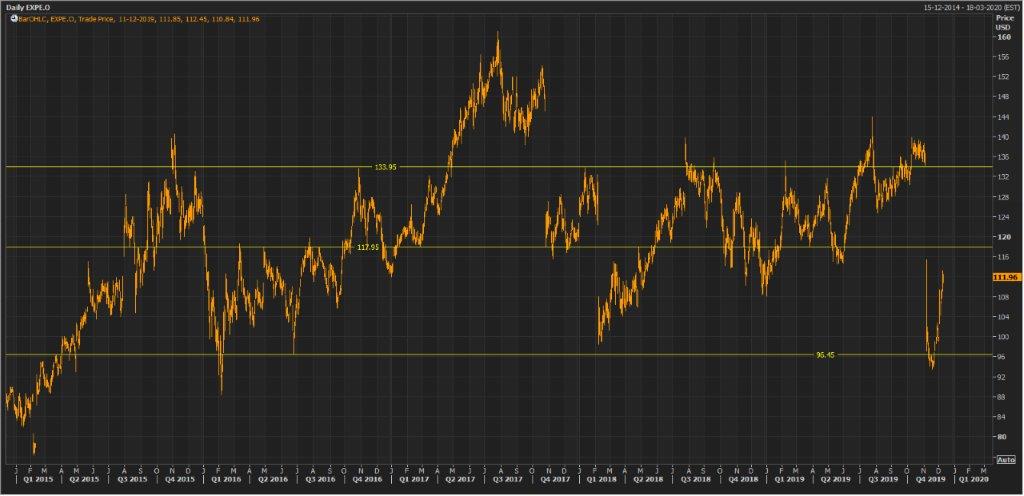

Stock Recommendation: The stock of EXPE closed at $111.96 with a market capitalization of $16.221 billion. The stock has corrected 7.071% and 5.399% in the last nine months and one year, respectively. In the last one month, the stock has generated positive return of 13.01%. The travel industry, including offline agencies, online agencies and other suppliers of travel products and services, has historically been characterized by intense competition, as well as a rapid and significant change. Despite the sectoral challenges, the business witnessed continuous growth in FY19. The company has delivered gross margin and net margin of 84% and 11.4% in Q3FY19, higher than the industry median of 52.4% and 0.4%, respectively. Considering the aforesaid facts, we have valued the stock with one relative valuation, i.e., price to earnings multiple and arrived at a target price of lower double-digit (in% terms). Looking at the price movement, valuation, better than industry growth and business prospects, we recommend a ‘Buy’ rating on the stock at the closing price of $111.96, up 0.1% as on 11 December 2019.

EXPE Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...