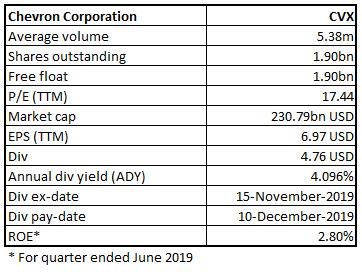

Chevron Corporation

CVX Details

Higher Net Oil-equivalent Production to Aid Business Prospect:Chevron Corporation (NASDAQ: CVX) is an integrated energy company, engaged in the production and distribution of crude oil and natural gas across the globe. The company is also engaged into refining activities and sells oil-based products such as fuels and lubricants.

Q3FY19 Operational Highlights for 30 September2019: CVX declared its Q3FY19 results, wherein the company reported total revenue and other income at $36,116 million as compared to $ 43,987 million in the previous corresponding year. Net income, during Q3FY19 came in at $2,580 million as compared to $4,056 million. During Q3FY19, average sales price per barrel of crude oil and natural gas liquids stood at $47, down from $62 in Q3FY18 while average sales price of natural gas during the same quarter came in at $0.95 per thousand cubic feet as compared to $1.80 in Q3FY18. The company reported net oil-equivalent production at 3.03 million barrels per day during Q3FY19, witnessing an increase of 3% on y-o-y basis. Refinery crude oil input during the third quarter of FY19 increased 8% on pcp to 992,000 barrels per day, aided by the acquisition of the Pasadena refinery in Texas. CVX reported revenue from its international downstream operations at $439 million during the third quarter of 2019 as compared to $625 million a year ago. As per the Management commentary, the decrease in earnings was largely due to the absence of 2018 gains from the southern Africa asset sale, partially offset by higher margins on refined product sales.

.png)

Q3FY19 Income Statement Highlights (Source: Company Reports)

During the third quarter of FY19, CVX repurchased an ordinary share worth $1.25 billion under its share repurchases program. The company also acquired deep-water exploration blocks in the Mexican Gulf of Mexico and Brazil's Campos and Santos basins, to strengthen the company’s product portfolio.

Stock Recommendation:The stock of CVX is trading at $121.57 with a market capitalization of ~$230.79 billion. The stock is available at an enterprise value (EV) to sales multiple of 1.6x on trailing twelve months (TTM) basis as compared to the industry median of 2.2x. As global demand for energy continues to grow, CVX is committed to meet this demand with less environmental impact. The company recently announced new goals to reduce net greenhouse gas emission intensity from upstream oil and natural gas production. During the first nine months of FY19, the company reported cash flow from operations at $21.7 billion, up from $21.5 billion in the corresponding 2018 period. Considering the aforesaid facts, valuation and business prospects along with improved operating cash flows, we give a ‘Buy’ recommendation on the stock at the current market price of $121.57, up 4.61% as on 04 November 2019.

CVX Daily Technical Chart (Source: Thomson Reuters)

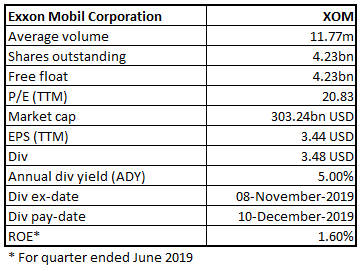

Exxon Mobil Corporation

XOM Details

Higher Production Q4 Guidance to Drive Improved Earnings: Exxon Mobil Corporation (NASDAQ: XOM) is engaged in exploration, production and distribution of crude and petroleum and related products across the world.

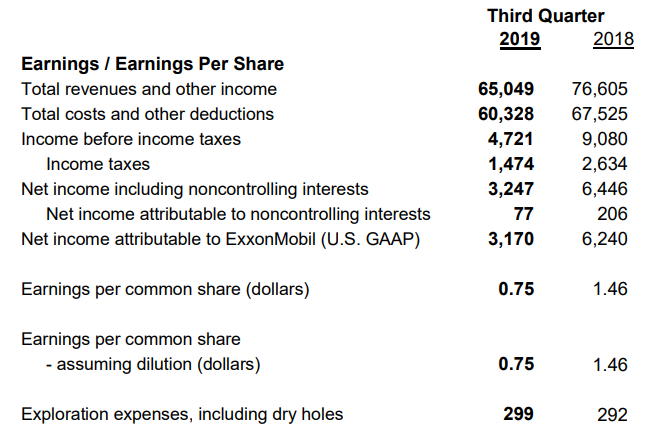

Key Highlights of Q3FY19: XOM announced its third quarter results, wherein the company reported total revenues and other income at $65.05 billion as compared to $76.61 billion in Q3FY18. Earnings during the quarter stood at $3.2 billion as compared to $3.1 billion in the previous quarter. Upstream liquids production during the quarter grew by 5% on y-o-y basis, driven by the Permian Basin. On a Q-O-Q basis, the company reported lower realizations from average crude and natural gas, which is in-line with the industry. The company reported 1% decline in Natural gas volumes. In the downstream segment, XOM posted improved industry fuel margins on Q-O-Q basis, aided by stronger distillate margins in Europe and Asia Pacific. The chemical segment witnessed weaker margins during the quarter. Results for the Chemical business were impacted by a reliability event at the Baytown, Texas olefins plant. Upstream volume during the quarter stood at 3,899 Koebd as compared to 3,786 Koebd in FY18.

Q3FY19 Financial Highlights (Source: Company Reports)

Outlook:The upstream business expects a higher production with seasonal gas demand. For downstream segment, higher fourth quarter schedule maintenance is expected. For the Chemical segment, XMO expects margin to be impacted by the supply length. Fourth quarter gas demand is expected to grow by an average of 150 Koebd on Q-O-Q basis.

Stock Recommendations:The stock of XOM is quoting at $71.67 with a market capitalization of ~$303.243 billion. XOM started production on its new high-performance polyethylene line in Beaumont, Texas, reflecting good progress on the advantaged investments in the Downstream and Chemical. The company also announced the global launch of its Mobil EV™ lubricants offering, which features a full suite of fluids and greases designed to meet the evolving drivetrain requirements of electric vehicles. In addition, the company enhanced the competitiveness of its portfolio through divestment of non-strategic assets. The stock of XOM is available at an EV to Sales multiple of 1.3x on TTM basis as compared to the industry median of 2.0x. Considering the aforesaid facts, business outlook and valuation, we recommend a “Buy” rating on the stock at current market price of $71.67, up 2.97% as on 04 November 2019.

XOM Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...