TPG Telecom Limited

.png)

TPG Details

Federal Court Approves Merger with Vodafone Hutchison Australia: TPG Telecom Limited (ASX: TPM) provides telecommunications services to the consumer, wholesale and corporates. On 13 February 2020, the company reported that it has received approval from the Federal Court of Australia regarding the proposed merger of TPG and Vodafone Hutchison Australia Pty Limited (VHA) via a Scheme of Arrangement. While, the implementation of the Scheme remains subject to several conditions, which include approvals from other regulatory bodies, the Federal Court and TPG Telecom shareholders.

Key Business Highlights for FY19: TPM announced its full-year results, wherein the company reported revenue of $2,477.4 million, down 0.7% on y-o-y basis. The business reported a profit for the year at $175 million, depicting a growth of 56% from FY18. The year was characterized by higher expenses related to impairment cost of $236.8 million followed by higher amortisation and interest expenses related to the Australian spectrum licences. Within the consumer segment, EBITDA stood at $457.3 million, as compared to $499.1 million for FY18 due toa $62.6 million reduction in gross profit, which was partially offset by a $20.8 million decrease in employment and overhead costs.

.png)

Key Income Statement Highlights FY19 (Source: Company Reports)

Guidance: By the end ofFY20, the company expects to have less than 15% of its residential broadband customer base remaining on ADSL. The business further expects operational efficiency programs to deliver savings and growth within the company’s corporate division. The business expects EBITDA to come in within the range of $735 million to $750 million.

Stock Recommendation: The stock of TPM is quoting at $8.150 with a market capitalisation of $6.78 billion. The stock is trading at the upper band of its 52-week trading range of $5.94 to $8.78.The stock has given a positive return of 10.26% and 6.10% in the last three months and six months, respectively. Going forward, the company improved financial impact from customer migration to NBN, along with the collective headwinds from residential DSL and home phone customers moving to NBN. Considering the current trading levels, acquisition with Vodafone Hutchison Australia Pty Limited and business prospects, we have we recommend a “Hold” rating on the stock at the current market price of $8.150 per share, up 11.491% on 13th February 2020, owing to the latest release related to the merger with VHA.

.jpg)

TPM Daily Technical Chart (Source: Thomson Reuters)

Telstra Corporation Limited

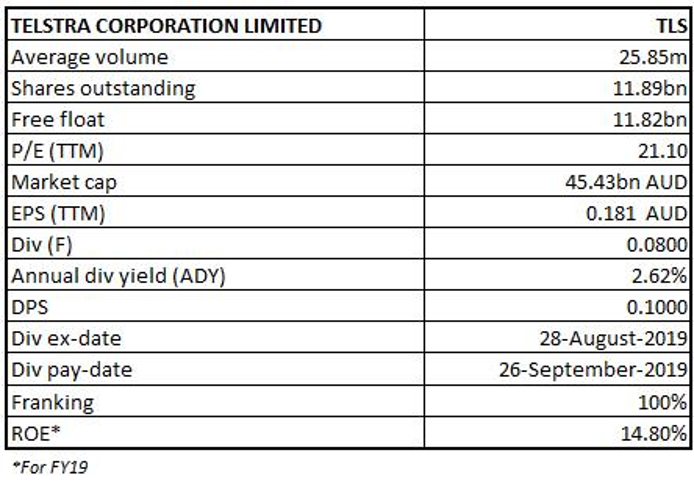

TLS Details

Added 5G Coverage Across 32 Regions: Telstra Corporation Limited (ASX: TLS) provides telecommunications carrier. The provision of telecommunications and information services includes mobiles, internet, and pay television.

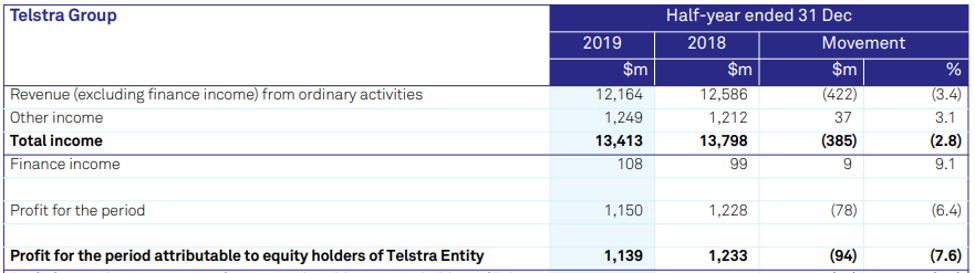

Key Operation Highlights for H1FY20 for the Period ended 31 December 2019: TLS declared its half-yearly results, wherein the company posted total income at $13.4 billion, down 2.8% from pcp. The company reported its NPAT at $1.15 billion, a decline of 6.4% from H1FY19. During the half, TLS added 137,000 retail postpaid mobile services consisting 91,000 from Belong, 135,000 retail prepaid mobile services, and 151,000 pre and postpaid Wholesale services. The company made an addition of 5G coverage across selected areas in 32 cities and regional areas and expects to execute the target of 35 regions in FY20.

Key H1FY20 Income Statement Highlights (Source: Company Reports)

Dividend Announcement: The Board of Directors has announced a fully franked dividend of $0.080 per ordinary share, payable on 27th March 2020.

Guidance: For FY20, the company expects total income to come between $25.3 billion to $27.3 billion, while underlying EBITDA is expected to come in the range of $7.4 billion to $7.9 billion. The business expects restructuring costs of ~$300 million whereas capital expenditure is likely to come between $2.9 billion to $3.3 billion. Free cash flow, after operating lease payments, is expected to come within the range of $3.3 billion to $3.8 billion.

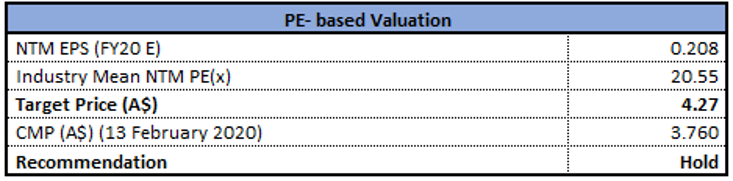

Valuation Methodology: P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Month

Stock Recommendation:The stock of TLS is trading at $3.76 with a market capitalization of $45.43 billion. The stock made a 52-week low and high of $3.022 and $3.978 and is currently trading at the upper band of its 52-week trading range. The stock has generated a mixed return of 8.22% and -2.01% in the last three-months and six-months, respectively. The company has more than 2.4 million services across the new, radically simplified plans while more than 1.2 million customers can enjoy the benefits of being a Telstra Plus member. In the recent past, more customers are choosing to interact through digital service interactions, which witnessed a growth of 57%. Considering the aforesaid facts, we have valued the stock using Price to Earnings based relative valuation method. For the purpose, we have taken the peer group – Uniti Group Ltd (ASX: UWL), SpeedCast International Ltd (ASX: SDA), Vocus Group Ltd (ASX: VOC), etc., and arrived at a target price offering lower double-digit upside (in % terms). Hence, looking at the current trading levels, business prospects and valuation, we recommend a “Hold” rating on the stock at the current market price of $3.76, down 1.571% as on 13th February 2020.

TLS Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...