NetComm Wireless Limited

Strong balance sheet with no debts: NetComm Wireless Limited (ASX: NTC) is known for developing tailored network-grade telecommunications equipment. It operates in 4G and 5G Fixed Wireless space. It is to be noted that S&P Dow Jones removed NTC into the All ordinary indices, effective from 18 March 2019. NetComm Wireless Limited and Casa Systems have announced that they have entered into a definitive agreement under which Casa Systems would be acquiring 100% of the equity interests in NTC by way of a scheme of arrangement. As per the scheme, NTC’s shareholders would be receiving cash consideration amounting to A$1.10 per NetComm ordinary share and NetComm would be a wholly-owned subsidiary of Casa Systems.

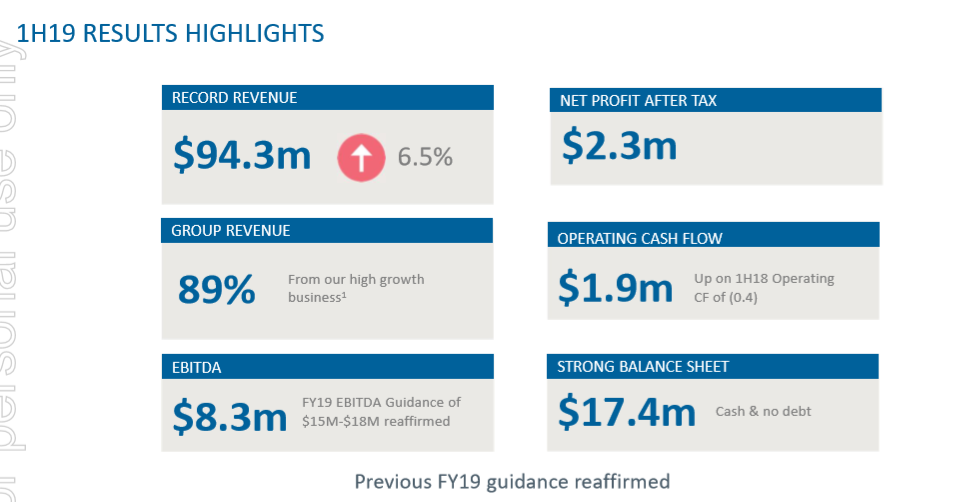

1H19 Results Highlights (Source: Company Reports)

The revenue stood at $94.3 million in 1H19 compared to $88.6 million in 1H18 reflecting growth of ~6.5% YoY primarily because of scaling of NCD contract and Fixed Wireless sales to multiple clients.The EBITDA reduced and stood at $8.3 million for 1H19, compared to $9.2 million in 1H18, primarily driven by planned 5G investments.

Company Guidance: The company’s revenues are expected to be up 15% to 20% over FY19. The company expects its reported EBITDA to be between $15 million to $18 million. The company expects earnings to be fairly evenly balanced across 1H19 and 2H19, based on current expectations around customer order patterns. The telecom sector is expected to grow by CAGR (2016-2023) of 10% with attractive market fundamentals. The stock, however, generated a significant YTD return of 41.45%.

Backed by a strong balance sheet, strong revenue growth, and decent industry outlook, we, thus, maintain our “Hold” recommendation on the stock at the current market price of $1.075 per share.

EML Payments Limited

Decent Performance in 1HFY19: EML Payments Limited (ASX: EML) is a payment solutions company that serves its businesses or consumers while making the payment experience to be an efficient and secured one.

The company in its announcements on 15 March 2019, has mentioned that Tribeca Investment Partners PTY Ltd has stopped to be a substantial holder of the company’s shares. It has also announced that one of its substantial holders, IOOF Holding Limited and its subsidiaries has cut down its stake in the company from an earlier 8.096% which comprised of 20,261,322 votes to 16,261,322 votes, which ultimately resulted into 6.498%.

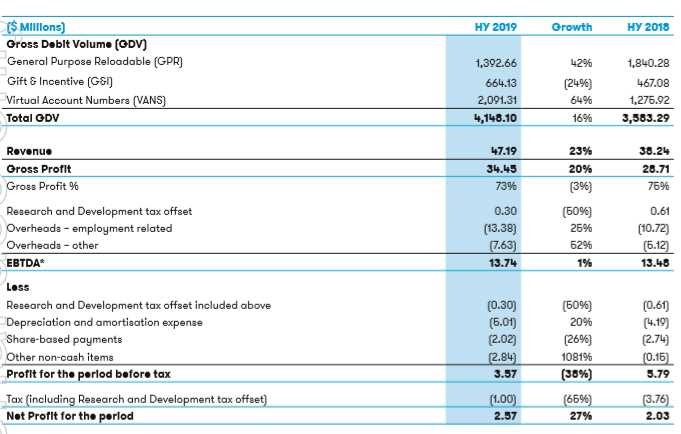

1HFY19 Performance Overview (Source: Company Reports)

EML’s revenues increased by 23% over the prior corresponding period to $47.2 million in the first half of 2019, with growth driven by all segments including G&I up 49%, GPR up 13% and VANS up 100%.The Group generated EBTDA of $13.74 million for the half year due to strong revenue growth driven by organic and acquisitive business development.

What to Expect From EML: The company has updated the revenue guidance for the 2019 financial year to be between $88-94 million as compared to the previous guidance of $82-88 million. The company has narrowed the EBTDA guidance to between $27-28 million compared to previous guidance of $26-28 million based on the results in the first half of FY19.

Meanwhile, the stock has generated a YTD return of 22.0% and 21.59% over the past three months. EML remains debt free with $50.1 million of cash at hand. The group revenue growth is a positive reflection of the inherent diversification in the business and the lack of reliance on any one customer, segment or geography. Based on the foregoing and looking at trading level, we maintain our “Hold” recommendation on the stock at a current market price of $1.830 per share (up 4.871% on March 15, 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...