Rhipe Limited

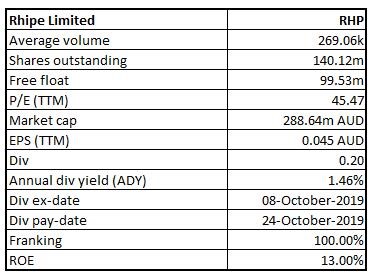

RHP Details

High Investment in Growth Strategies & Development of SmartEncrypt: A cloud-based company, Rhipe Limited (ASX: RHP), is engaged in offering the licensing facility, business development and knowledge services, thus, supporting its partners and software vendors with an end to end cloud solutions.

Shareholding Update: On 16th December 2019, the company updated that National Nominees Ltd ACF Australian Ethical Investment Limited, has become a substantial holder of the company, holding 7,109,460ordinary shares with a voting power of 5.07%.

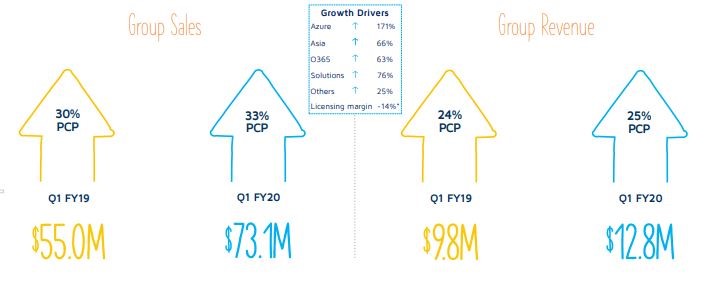

Trading Updates for 1QFY20: The company reported gross sales of $73.1 million, up 33% year over year. Group revenues for the period stood at $12.8 million, an increase of25% year over year.The company reported operating expenditure of $9 million, up 29% year over year. Operating profit for the period came in at $2.9 million, up 6% year over year.

1QFY20 Trading Highlights (Source: Company Reports)

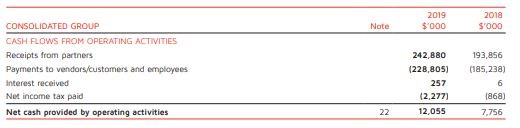

Key Highlights of FY19: The year 2019 witnessed a strong growth trajectory with delivering an operating profit of $12.8 million and EBITDA of $10 million, representing a yoy increase of 65% and 56%, respectively. Operating cash flows for FY2019 came in at $12.1 million. The company exited FY2019 with cash and cash equivalent of $25.53 million as compared to $22.69 million at the end of FY18.

Cash Details (Source: Company Reports)

Outlook: For FY20, the company expects to invest $0.6 million on the development of SmartEncrypt. The company also intends to invest infront office sales, marketing strategies and technical staff in order to support a higher number of customers across all countries. It also expects FY20 operating profit to come in at $16 million, excluding any changes in market conditions or major expansion initiatives such as geographical or vendor expansion opportunities.

Valuation Methodologies:

Method 1: Price to Book Value Multiple Approach

.png)

Price/Book Value Based Approach (Source: Thomson Reuters)

Method 2: Enterprise Value to EBITDA Multiple Approach

.png)

EV/EBITDA Based Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock is trading slightly below the average of its 52-week low and high of $1.185 and $3.120, respectively. As on 23 December 2019, the company’s market capitalisation stands at ~$288.64 million, with 140.12 million outstanding shares. The stock increased approximately 66.8% on a year-to-date basis. The company expects its public cloud business to be a growth engine for the corporates. The sales and revenue are expected to improve with more APAC business transiting their workloads to the cloud. The company also focuses on executing opportunities in Australia and invest in Microsoft Dynamics channel staff in FY2020. Considering the above factors, we have valued the stock using two relative valuation methods, i.e., Price to Book Value and EV/EBITDA multiples and arrived at a target price with lower double-digit upside (in % terms). Hence,we recommend a “Buy” rating on the stock at the closing price of $2.10 per share, up by 1.942% on December 23, 2019.

RHP Daily Technical Chart (Source: Thomson Reuters)

Splitit Payments Limited

.png)

SPT Details

Robust Black Friday Sales & Operational Efficiency: A technology-based company, Splitit Payments Limited (ASX: SPT), is engaged in providing cross-border payment-based services to businesses and retailers. It helps customers with “buy now and pay later” facility by utilising their credit card without any additional cost. On 12 December 2019, the company provided facts about its worldwide operations, including Black Friday and Cyber Monday long weekend.The company saw better-than-expected growth in its key US market, with underlying merchant sales increasing by 83%. The company also entered into partnership agreements with Magento, iPay88 (over 15,000 merchants) and BlueSnap. These partnership initiatives are likely to accelerate the company’s merchant acquisition in 2020. Splitit Payments Limitedalso entered into new merchant agreements with multiple brands, including Dick Smith, Reds Baby, ReST, Plus Shop, Slabway, Later Gator and Mobvoi.

Financial Highlights for Third Quarter FY19 for Period Ended 30 September 2019: The company reported an increase of 97% in total merchants, which came in at 624 for the quarter. Total Customers for the period increased 187% year over year and came in at 235,000. Merchant Transaction Volume stood US$30.5 million for the quarter, an increase of 100% year over year. Merchant fees came in at US$466K, up 96% from the year-ago quarter. Net cash used during the quarter stood at $6.92 million. The company exited the quarter with cash and cash equivalent of $16.15 million.

Financial Highlights (Source: Company Reports)

What to Expect: In the coming quarter, the company is expecting net cash outflow amounting to ~$3.61 million.

Stock Recommendation: The stock is trading below the average of its 52-week low and high of $0.305 and $2.000, respectively. As on 23 December 2019, the company’s market capitalisation stands at ~$211.84 million, with 311.53 million outstanding shares. The stock gained 38.78% in the last three months. The need for instalment payment solutions is growing every day on a global scale, and the company is well-positioned to take advantage of the growing demand. The company is likely to benefit from increasing customer base, partnership initiatives and accelerating merchant acquisition. Considering the above factors, we recommend a “Buy” rating on the stock at the closing price of $0.670 per share, down by 1.471% on December 23, 2019.

SPT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...