Coles Group Limited

Supermarket Sales supported by ‘Fresh Stikeez’ Campaign: Coles Group Limited (ASX: COL) is a leading Australian retailer, with more than 2,500 retail outlets nationally. The newly announced Supermarket and Express collectables program ‘Fresh Stikeez’ has been designed so that the kids along with their parents are encouraged to eat more fresh fruit and vegetables.

Recently the group delivered its 46th consecutive quarter of comparable sales growth.

.png)

Third Quarter Sales – 12 Weeks to 24 March 2019 (Source: Company Reports)

Supermarket sales grew 3.2% in the third quarter of the 2019 financial year, supported by a successful ‘Fresh Stikeez’ promotional campaignwhich drove high customer engagement. The online sales saw a growth of 27%, with recording sales more than $1 billion on a rolling twelve-month basis. The liquor comparable sales adjusted for New Year’s Eve timing increased 0.9%, with continued strong growth in Exclusive Liquor Brands in the wine category. Despite the impact of year-on-year fuel volume declines, there was strong growth in Coles Express food-to-go segment.

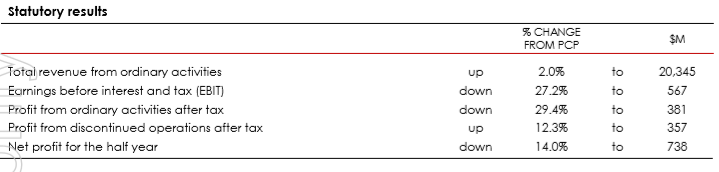

Statutory Results for 1H FY19 (Source: Company Reports)

On the financial front, the statutorysales revenue from continuing operations increased by 2.0% to $20,235 million largely due to 3.1% growth in Supermarkets’ sales revenue. The EBIT from continuing operations decreased by $212 million or 27% to $567 million mainly on the back of $146 million restructuring provision in Supermarkets, reduction in Express EBIT of $35 million and higher corporate costs associated with the demerger. The ROE for 1H FY19 stood at 13.6% which is significantly higher than the industry median of 5.6% respectively.

Company Guidance: The third quarter sales momentum of FY19 is broadly in line with the second quarter. The cost pressures from the new store enterprise bargaining agreement (EBA) along with energy & drought impacts on input costs is likely to continue going forward. The company hopes to pay the first dividend in September 2019 which seems to be the final dividend for the year ending 30 June 2019. This reflects earnings post demerger during the seven months. The target dividend pay-out ratio of 80-90% of earnings is payable in September 2019, as confirmed by the Board for the time frame of 28 November 2018 to 30 June 2019.

The company focuses on laying the foundations for long term sustainable growth. The partnership with Witron was announced by the company for an investment of ~$950 million over six years. The investment is in world class automated distribution centres, which might positively impact the sales volume going forward. Further, based on strong normalized cash realisation (141.0%) due to favourable seasonal working capital movements, robust balance sheet supporting investment grade credit rating and providing significant flexibility for long term growth, we believe the company has decent prospects going forward driven by robust fundamentals. Hence, we give a “Buy” recommendation on the stock at CMP of $12.640 (up 0.317% on 29 April 2019).

Wesfarmers Limited

Trading at Higher Level: Wesfarmers Limited (ASX: WES) announced that it had made a conditional, non-binding indicative proposal to the Board of Lynas Corporation for the acquisition of Lynas for $2.25 a share, payable in cash, as per the scheme of arrangement. The proposal is conditional on, among other things, ensuring that relevant operating licences in Malaysia are in force and will remain in force for a satisfactory period following completion of the transaction.

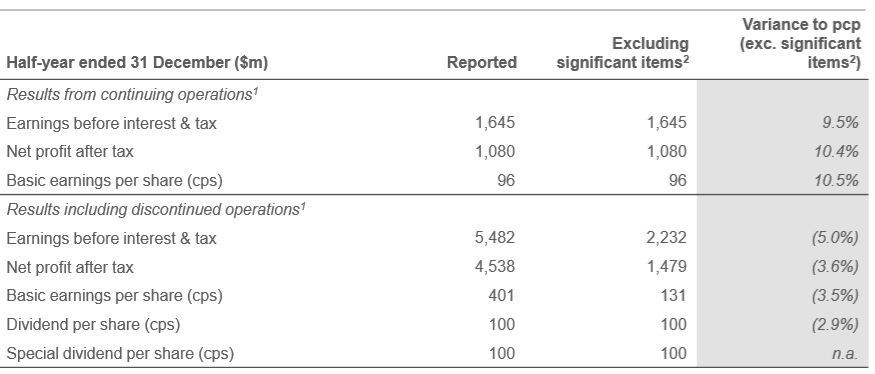

Financial Overview 1H19 (Source: Company Reports)

WesCEF revenue was 14.4% above than the prior corresponding period, driven by all businesses contributing to the revenue growth.The net profit after tax for the company stood at $4,538 million for 1H19, including post-tax significant items of $3,059 millionrelated to discontinued operations, including gains on the demerger of Coles and disposals of Bengalla, Kmart Tyre and Auto Service, and Quadrant Energy which were completed during the half-year period. The NPAT from continuing operations increased by 10.4% to $1,080 million.

The net margin and the ROE increased by 260 bps and 340 bps in 1HFY19 as compared to the prior corresponding period of 1HFY18 and stood at 7.5% and 6.3% respectively, primarily driven by higher profits.

What to Expect Going Ahead: Going forward, the balance sheet of the group is expected to remain strong and the company remains well-placed to derive the advantage of value-accretive growth opportunities and creating value for shareholders over the long term. The industrial businesses will continue to be subject to international commodity prices, exchange rates, competitive factors and seasonal outcomes. Over the medium term, the earnings of the company are expected to be adversely affected due to the oversupply of explosive grade ammonium nitrate in the Western Australian market, however the short-term outlook for the WesCEF business is generally positive.

The mean EV/EBITDA for Wesfarmers stood at 11.66x as compared to the peer median of 8.75x, indicating an overvaluation of the stock at current market prices.Looking at the historical price performance, the stock has gained 6.48% in one month and 14.11% in three months. Currently, the stock is trading near to its 52-week high of $36.623. Considering the fundamentals and valuation along with the return generated by the stock in last one-year, we assume that most of the positives are factored in at the current price. Hence, we give an “Expensive” recommendation on the stock at CMP of $35.80 per share (down 0.528% on 29 April 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...