.png)

Stocks’ Details

Orica Limited

Lower First Half in Line with Guidance: Orica Limited’s (ASX: ORI) stock tumbled 6.358 per cent on May 07, 2018 at the back of muted performance in first half of the year wherein revenue increased by 4% YoY (largely in line) to $2,532 Mn as against $2,437 Mn in 1HFY17. The sales surged up by improved volume and value growth during the same period. However, EBIT (earnings before interest and tax) recorded de-growth of 20% to $252 Mn in 1HFY18 as compared to previous corresponding period. This was mainly impacted by operational issue incurred during first half of the year. As a result of this, PAT contracted at $124 Mn in 1HFY18, marking de-growth of 37% on YoY basis. Management stated that the company is on track to deliver full year sales volumes at the upper end of guidance and improved operational performance across all regions that will support a stronger performance in the second half of the financial year.

.png)

1H FY18 Financial Performance (Source: Company Reports)

Furthermore, second half global AN volume is expected to increase by around 10% from the first half of the year, and full year global AN volume is expected to be at the upper end of the previously stated range of 3.65 Mt. EBIT for second half is expected to be broadly in line with second half of previous year. Besides this, the group declared unfranked interim dividend of 20 cents per share and it will be paid on July 02, 2018. This represents a pay-out ratio of 61% of underlying earnings before individually significant items which is within the target pay-out ratio range of 40-70%. Harris Associates L.P. and its related bodies, a substantial holder of Orica Limited, changed its holding on March 20, 2018, from 11.56 per cent of the voting power to 12.70 per cent. As of now, we give an “Expensive” recommendation on the stock at the current market price of $ 19.00 considering present setbacks for full year and soften outlook stated by management for upcoming period.

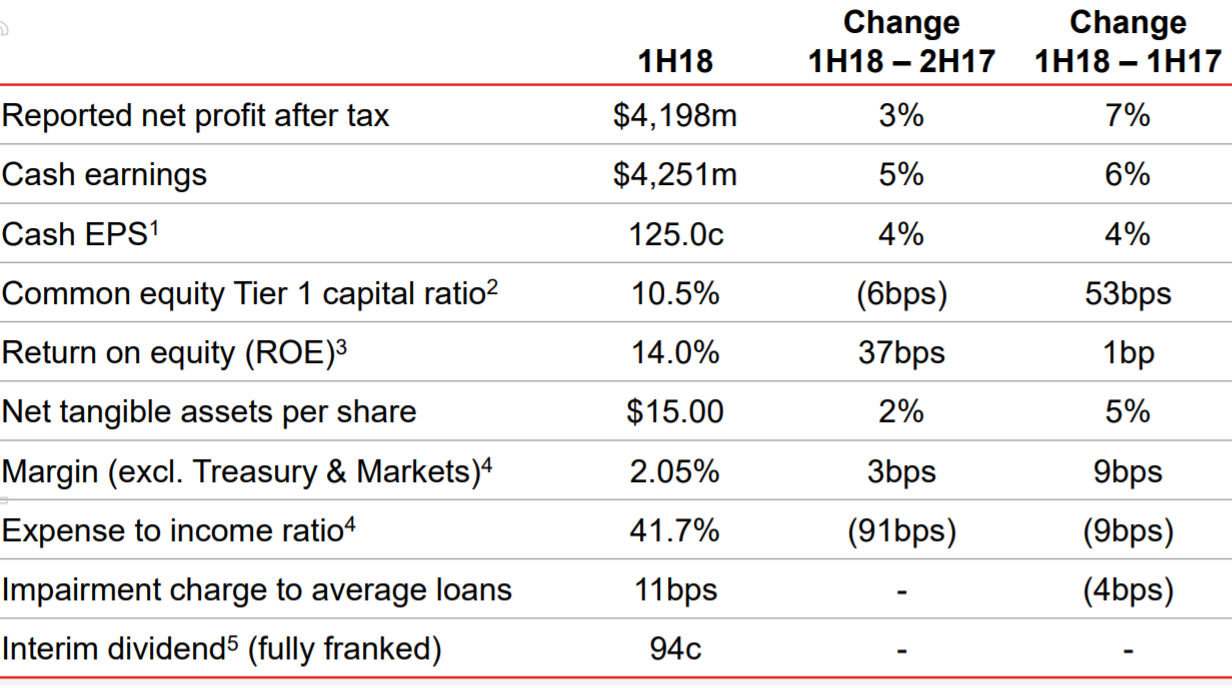

Westpac Banking Corporation

Decent 1HFY18 Performance: Westpac Banking Corporation’s (ASX: WBC) stock edged up by 0.825 per cent on May 07, 2018 at the back of decent set of result for first half year wherein Net Profit after tax rose by 7% to $4,198 Mn in 1HFY18 as compared to prior corresponding period (pcp). The result was mainly supported by disciplined loan and deposit growth, improved margins and well managed expenses during 1HFY18. Further, net interest income increased by 9% in 1H FY18 with loan growth of 5%, mostly accounted from Australian housing market. As a result, reported net interest margin (NIM) increased by 11 basis points to 2.16% which was driven by mortgage lending and deposit spreads throughout the same period. On the other hand, the Group maintained the strength of its balance sheet with CET1 capital ratio of 10.5% which is in line with the benchmark set by Australian Prudential Regulation Authority (APRA). Liquidity Coverage Ratio (LCR) came at 134% which is well above the regulatory minimum.

Decent 1HFY18 Performance (Source: Company Reports)

Further, the group’s Net Stable Funding Ratio (NSFR) stood at 112% as at 31 March 2018 which is above the APRA minimum regulatory requirement of 100%, which came into effect from 1 January 2018. Further, the interim dividend for first half of the year is 94 cents per share, consistent with the interim dividend for the second half 2017. This represents a dividend pay-out ratio of 75.3% for the first half of the year on a cash earnings basis. It will be paid on July 04, 2018 with record date of May 18, 2018. Based on market volatility, intense competition, rise in credit defaults, and changes in regulatory policy and Royal Commission, we continue to maintain our “Expensive” recommendation on the stock at the current market price of $ 29.340.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...