.PNG)

Stocks’ Details

Coles Group Limited

Bright Future Prospects:Coles Group Limited (ASX: COL) is a leading supermarket retailer with 2500 retail outlets. Its core business includes- Coles Supermarkets, Coles Online, Coles Liquor, Coles Express, Flybuys, Coles Financial Services, Spirit Hotels.

Recent Developments: COL entered into partnership with Ocado Group where the later will provide access to its OSP (Ocado Smart Platform) technology to COL. For the purpose, Two CFCs (Customer Fulfilment Centres) are planned to be operational by FY2023. Capital expenditure inclusive of upfront Ocado fees is anticipated to be in the range of around $130 million to $150 million over the four year development and construction period. The development will bring in lower cost, improved network capacity, product availability etc leading to an improvement in profit margins for COL.

Recently, Coles had made an announcement that they have entered into incorporated Joint Venture with Australian Venue Co (or AVC) in relation to its hotels business, Spirit Hotels. AVC happens to be a highly experienced and responsible operator when it comes to hospitality assets

1H FY2019 Result Review: COL recorded strong numbers for first half of FY19 with YoY growth of 2.6% in sales revenue coming in at $20,867 million. The group’s EBIT saw a decline of 5.8% to $733 million mainly on the back of lower Express EBIT and additional corporate costs. The favourable seasonal working capital movements have resulted in strong cash realisation (normalised) of 141%.

.png)

Strong Cash Generation (Source: Company Reports)

What to Expect from COL:Management has narrowed the net capex for FY19 to $700-800 million. COL’s Supply Chain Modernisation project will see an initial payment to be paid in second half. The company’s management targets dividend pay-out ratio at 80-90% of earnings from 28th Nov 2018 to 30th June 2019, payable in September 2019.

Stock Recommendation: At current market price of $12.210 per share, stock is trading at P/E multiple of 21.910x. The stock has risen 6.5% in last one-month whereas, on YTD basis, stock has gone up by 3.5%.From valuations perspective, the company’s P/B ratio stood at 6.1x which is quite higher as compared to industry average of 2.6x reflecting that the stock is quite overvalued at the current trading juncture.

Hence, with the above-mentioned factors, we maintain our “watch” stance on the stock at the current market price of $ 12.210 per share (up 0.743% on April 8, 2019). Further, we advise that market players should wait for the stock to witness a correction and then make an entry at reasonable levels.

Sydney Airport

Further Improvement in Fundamentals:Sydney Airport (ASX: SYD) is owned by SAL group. The investment policy of SAL Group is to invest funds in accordance with the provisions of the governing documents of individual entities within SAL Group.

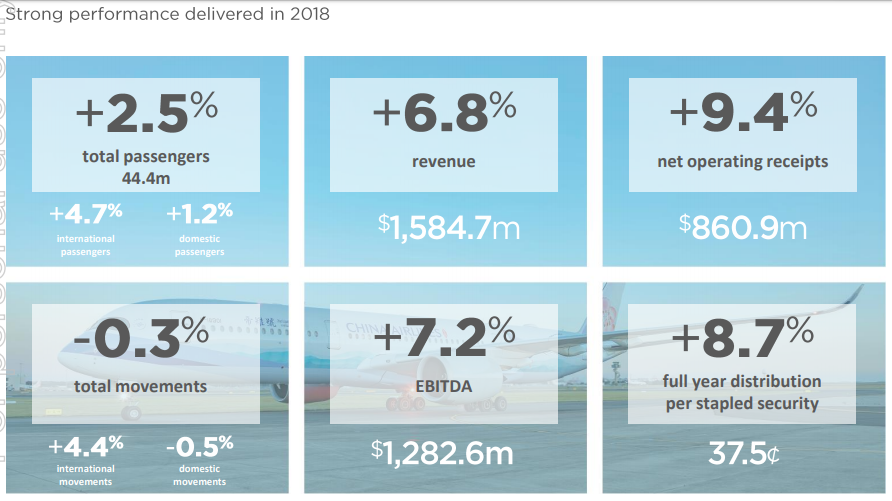

Financial Performance of FY18: Overall, the revenue for the business increased by 6.8% primarily because of international passengers coupled with strong performance from retail and property. The balance sheet strengthened further with cashflow cover ratio going up from 3.0x in FY17 to 3.2x in FY18. Net debt/EBITDA reduced to 6.6x in FY18 as compared to 6.7x in FY17.

Strong Performance in FY18 (Source: Company Reports)

What to Expect: The management provides a 3-year capex guidance of $0.9-$1.1 billion for the 2019-2021 period. The management is expectedto deploy between $390 million-$440 million in 2019.

Growth Across the Business (Source: Company Reports)

For the month of Feb 2019, The number of International passengers moving through the Sydney Airport were marginally ahead of prior corresponding period, growing by 0.4%.However, the domestic passenger numbers witnessed the fall of 2.7% on pcp.

Stock Recommendation: Looking at the price movement, stock has risen 10.53% on 1-year basis. At current market price of $7.270, stock is trading at a P/E multiple of 43.800x with a market capitalization of $16.34 billion and annual dividend yield stands at 5.18%.

The company’s stock has witnessed the rise 1.69%, 10.20% and 7.42% over the span of one-month, three months and six-months, respectively pushing the stock closer to its 52-week higher level.

As a result, we have a “watch” stance on the company’s stock at the current market of A$7.270 per share and we further advise the players to look for correction in the upcoming periods as, we presume, that the current trading juncture had discounted some key growth catalysts.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...